The rising frequency and impact of global risks—such as COVID-19, geopolitical crises, and cybercrime—are placing increasing pressure on the insurance industry. To stay ahead and effectively address these challenges, insurers must adopt new technologies and implement digital insurance strategies.

With extensive experience in insurance technology consulting, Intellias can guide you through this transformation. In this article, we’ll explain what digital insurance is, outline the steps to becoming a digital insurer, and highlight the benefits you can expect.

What is digital insurance?

Digital insurance refers to a digital-first approach to running an insurance business, where technology becomes a core element of operations and customer service.

You might wonder: since most insurance businesses use some technology, doesn’t that make them digital insurance providers? Not exactly. Being a digital insurer involves more than just using software; it requires transforming the entire insurance experience for both the company and its customers.

A key aspect of digital insurance is the digitalization of the entire value chain, from customer acquisition and underwriting to policy management and claims processing. Traditional insurance providers may use software for specific functions, such as managing customer records or processing claims, but they often still rely on manual processes.

Another significant difference is in customer interaction. Digital insurers emphasize online channels like websites, mobile apps, and chatbots. In contrast, traditional insurers often rely on in-person meetings and phone calls, offering only limited online services and lacking the comprehensive digital integration seen in digital insurance.

Benefits of digital insurance

By positioning technology at the heart of the business rather than viewing it as merely a support tool, the digital insurance approach delivers substantial benefits for both insurers and customers. Let’s explore some of the key advantages.

It makes insurance convenient and accessible

With a digital-first model, customers can purchase, manage, and renew their policies online through web platforms or mobile apps. They can check insurance details, make changes, and file claims anytime, anywhere — without the need for in-person visits or phone calls. Additionally, customers are not restricted by office hours; they can obtain instant quotes, update policies, and track claims around the clock.

It reduces costs for insurers

The digital insurance model enables insurers to do more with less, making operations leaner and more cost-effective. By automating routine tasks such as data entry, claims processing, and customer service, insurance companies can free up staff for more strategic roles and reduce labor costs.

Digital automation also accelerates processes, resulting in faster turnaround times and lower overall expenses. Additionally, transitioning to digital reduces the need for physical office space, leading to further cost savings.

It gives digital insurers a competitive edge

Digital insurance providers gain a significant competitive edge by offering flexible and customer-focused products. For example, advanced tools enable digital insurance providers to create policies based on real-time data, such as mileage for auto insurance or health metrics for life insurance. This means customers pay only for what they actually use or need. These personalized and adaptable coverage options distinguish digital insurers from traditional providers, who often offer more static and less dynamic services.

It prevents fraud

Advanced technologies used by digital insurers can analyze large volumes of data to detect patterns that may indicate fraudulent activity. This makes it more challenging for fraud to go undetected and allows for the early identification of suspicious claims and behaviors. Additionally, predictive models that assess risk factors and historical data can identify potential fraud before it occurs, enabling digital insurance providers to take proactive measures to safeguard their businesses and data.

Digital insurance: Market overview

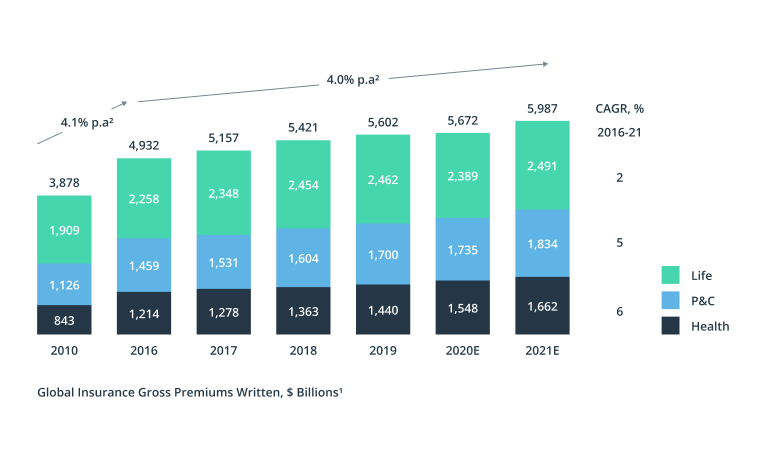

Out of every crisis, the insurance sector has only emerged stronger. The current crisis is no exception. After a slump, global insurance markets are bouncing back. McKinsey confirms a gradual rebound in 2021.

Source: McKinsey — Global Insurance Report 2022

As the impact of the health crisis waned, cross-sector recovery and market normalizations (to an extent) have been driving organic growth for insurance players. According to Statista, the global insurance market was valued at $6 trillion in 2022 — the first year after the pandemic — and is expected to keep growing in the coming years.

However, the pandemic prompted not only the growth of the market but also the digital transformations in the insurance sector. Most insurers are now recognizing that simply reacting to risks isn’t enough: they need to transform their approach to prevent losses. Along with the growing demand for customer-focused services, it creates a pressing need to adopt new technologies and innovate.

Moreover, the digital insurance market is rapidly expanding, with an estimated value of $132.86 billion in 2024 and projected to reach $229.07 billion over the next five years. This growth is led by the emergence of new, digital-first players who are raising the industry’s standards and driving further innovation.

So today, insurers are once again back to the drawing board. This time around, many have bigger technology budgets — but also a larger spectrum of needs to address.

![[whitepaperbox link="https://intellias.com/ebooks/ai-insurtech-embrace-the-tech-revolutionizing-insurance/" imageid="74480" title="AI Insurtech - Embrace the Tech Revolutionizing Insurance" ]Everything You Need to Know about the Insurance Industry and Artificial Intelligence[/whitepaperbox]](https://d3twecw9qvot3u.cloudfront.net/wp-content/uploads/2024/05/AI-Insurtech-cover-1.png)

If I were to drop by your board meetings today, I’d probably hear things like:

- We need to improve our digital customer acquisition process. Do we have a UX designer, or who’s in charge of this?

- Why is our claims management process so slow? Should we invest in robotic process automation? I’ve heard good things about that.

- Let’s use AI to better predict new risks and adjust premiums. Who knows an AI guy?

- Why aren’t new customers buying from us? What’s wrong with them picking up the phone to call?

- Blockchain! I heard someone saying we should do “blockchain,” no?

Indeed, technology for insurance is easy to find these days. You have plenty of options pitched by tech vendors, startups, consultancy firms — practically every thought leader in the space.

But how do you move away from decades of separation of business and technology toward an interconnected digital insurance stack?

We discuss three essential tips in the next section:

- Define your business objectives

- Critically assess hyped technologies

- Build your digital insurance strategy from the bottom up

Digital insurance: Why not all technologies were born equal

Similar to financial services at large, the insurance industry is:

- Data-dependent

- Susceptible to risks

- Interwoven with other industries

Insurers need to do three major tasks in parallel: improve customer offerings and the customer experience, minimize the risk radar, and grow operational effectiveness. Many must do so across service lines designed for different industries — automotive, healthcare, logistics, construction, etc.

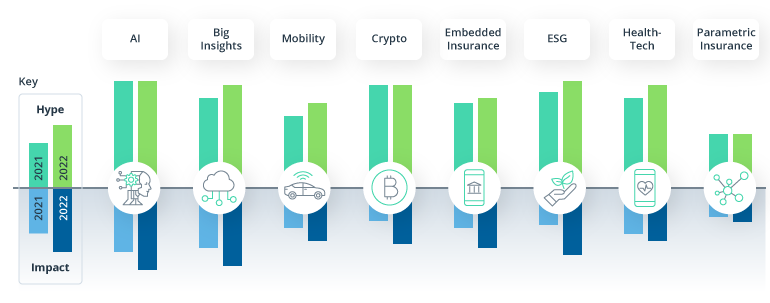

Because there are so many jobs to be done, there’s no shortage of technology for insurance being branded as “promising,” “innovative,” or “disruptive” for one use case or another.

Source: InsurTech Insights – Insurtech 2022: Hype vs. Impact

Artificial intelligence (AI) and machine learning (ML) are promoted as solutions for improving back-office processes: claims management, underwriting, risk analysis, etc. At the same time, they are touted as the tech pillar for innovative insurance products — context-aware, usage-based, and hyper-personalized.

Likewise, drones in insurance can massively increase the speed and quality of inspections while supplying field data during claims investigations.

What is often left unsaid in conversations surrounding new insurance technology are prerequisites for adoption.

Can most insurers benefit from AI? In the long-term perspective, sure. Will every insurer get immediate ROI from AI? Not without mature digital infrastructure in place.

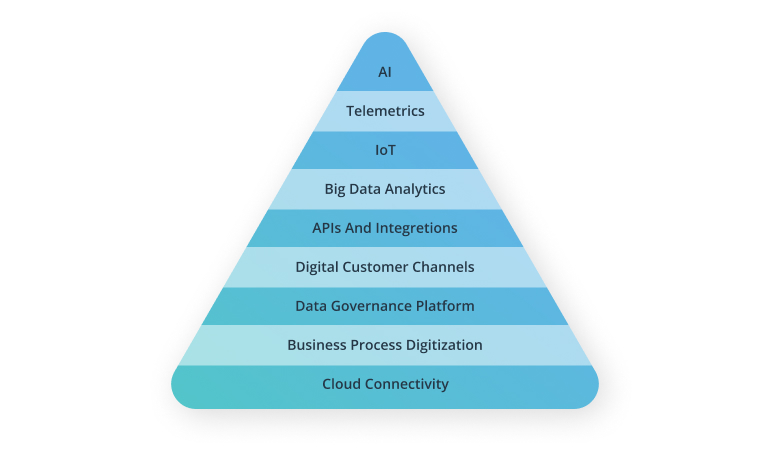

Much-hyped emerging technologies for insurance require an existing technical foothold — cloud connectivity, APIs, robust and secure data governance frameworks, and a high degree of business process automation.

When an insurance business is mostly backed by a paper trail rather than connectivity, no novel technology can fix that. You need to put down your digital roots first.

And we propose a bottom-up approach for that:

Baseline: Digitize standard business processes

Branches, brokers, paper-based back-office — the triumvirate worked well, with small improvements being enough to spur growth.

But year after year, the baggage of legacy insurance systems has gotten heavier. Though some players have managed to successfully digitize some processes and update the system’s legacy rules, productivity improvements have often proved marginal.

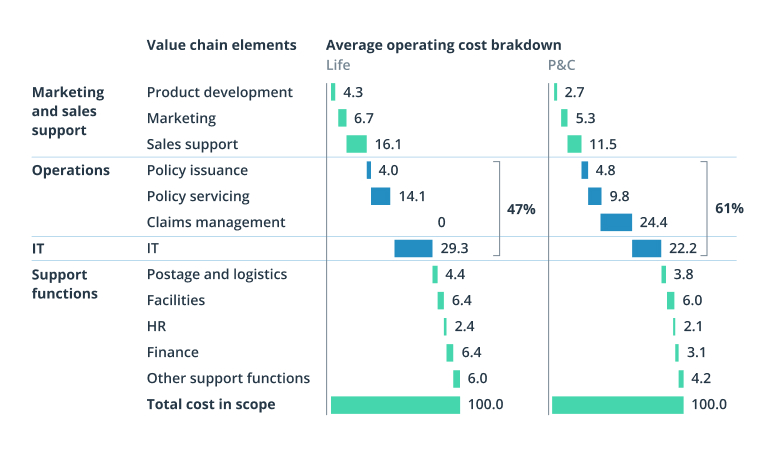

McKinsey found that among global P&C carriers, expense ratios reduced only by 45% between 2014 and 2019. IT and operations accounted for 50% of a typical insurer’s cost base in the same period.

Source: McKinsey — Successfully reducing insurance operating costs

For most insurers, the idea of modernizing legacy core systems sounds almost heretical. Why flip on its head what is fully functional? you might be wondering.

And you’re right. Legacy insurance systems don’t have to be ripped apart or fully replaced with new custom solutions. In most cases, you’ll end up with another obsolete system in several years’ time.

But you can’t keep the status quo either. Inaction can lead to loss of market share and revenue to faster-moving digital insurance players that offer a better customer experience (CX), release innovative products faster, and operate at lower costs.

What’s the fix, then? Progressively adding new blocks atop your core systems and digitizing back-office and front-office processes.

To achieve extra operational resilience and contain costs, insurers must map:

Let’s take claims management as an example. Six in ten insurers admit that emerging technologies have made a significant impact on their claims processes. Why? Because most of the steps have been manual and/or dependent on human labor.

Steps from paper-based claims submission to subsequent data entry, verification, and claims settlement are done semi-automatically (using rules) with few integrations available for faster data reconciliation.

When essential steps like intake information collection, data dissemination, and reconciliation are automated with RPA, astounding results follow. A multilinear insurer automated their disability claims management process (one of many) and saw a 25% increase in staff productivity, a 40% reduction in handoffs, and an estimated $37.4 million project cost reduction over four years. They didn’t even have to retire any legacy software, by the way.

Action steps:

- Digitize standard business processes

- Implement RPA and intelligent automation

- Move extra systems to the cloud

- Break down data silos for operational reporting

- Establish a data governance framework

Mid-term: Leverage digital insurance technologies for added value

You’ve done the groundwork. Your back-office runs like clockwork — business systems are better integrated, third-party data comes via integrations, and standard workflows are automated. Agents are happier and more productive, plus expense ratios are down.

It’s time to push the envelope further and face the customers.

The new generation of connected consumers don’t want to visit the branch or talk to an experienced agent on the phone.

Insurance customers are more thrilled by the prospects of

- 54% getting good value for their money

- 48% convenience of obtaining services

- 24% fairness of the policies offered

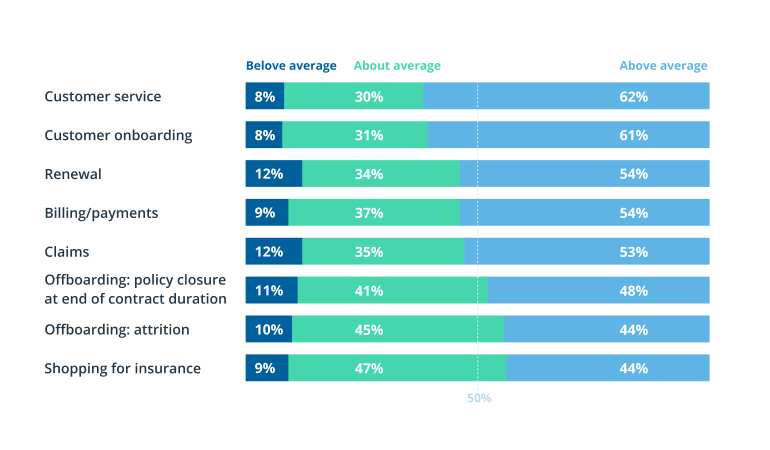

All the above are pillars of a stellar customer experience (CX) in insurance — but providers don’t hold up to their end of the bargain. Most overestimate their CX compared to the competition:

Source: IBM — Elevating the insurance customer experience

The majority of insurers also harbor outdated beliefs about customers. In 2020, only 5% of insurers actively used websites for engaging with prospects, whereas 49% of consumers marked this channel as “important.”

It appears that cost containment and operational effectiveness improvements pushed customer-focused initiatives to the backburner over the past two years. If that describes you, it’s time to get back on the customer track. ,

Where traditional insurance companies have stalled, InsurTech players have rapidly moved in. Around 40% of digital insurance companies have cut into profits at the marketing and distribution segments of the insurance value chain.

Similar to digital banks, InsurTech providers have won over customers with convenience and fast access to competitively priced products. Using a combination of intelligent process automation and big data analytics, they can issue flexible policies in minutes. A seamless digital account opening experience and fast onboarding have helped them rapidly grow their user bases.

The Global Insurtech Market was estimated at $16.6 billion in 2023 and is projected to increase to $36.5 billion by 2032.

As it’s easy to guess, a lot of these funds will go into further CX improvements and diversifying digital insurance service portfolios.

Traditional players must move fast too and transition to omnichannel sales, plus deploy more tailored customer products.

Place customer pain points at the center of your insurance product development. Then ask how good your company is at recognizing these issues during the sales process. What steps are you taking to increase the speed, accuracy, and fairness of claims resolution?

When mulling these questions, many insurers realize they lack sufficient data. In particular, many lack intelligence across two axes — customer knowledge and field data.

| Customer knowledge | Claims-related data |

|---|---|

| Standard customer journeys | Unstructured customer-reported data |

| Purchase decision factors | Pre-existing health conditions |

| Changing life circumstances | Historical data from past inspections |

| Price sensitivity | POS consumer data |

| Psychographic information | Geospatial intelligence |

| Habits and behavioral data | Mobile interactions data |

All of the above comprise big data in insurance — raw intel you can transform into insights for instantaneous decision-making, powered by advanced analytics solutions.

These insights are also essential to the development of parametric insurance products, where historical claims data is used to determine a set of conditions that trigger an instant settlement for a client. At the same time, big data analytics solutions can improve your agents’ productivity and diminish risk exposure for your business (without raising premiums for customers).

Take it from one of our clients, a global life insurer. In two years, we helped them set up an advanced risk assessment portal for streamlined customer assessments. The system connected to multiple data sources and took into account a wide number of parameters, including a customer’s medical history, sports activities, occupation, travel, and residence.

Powered by a dynamic neural network, the portal enabled insurance agents to complete health and lifestyle evaluations using scientific guidelines and proven methods for risk assessment in healthcare.

Action steps:

- Implement digital customer channels

- Start accumulating customer intelligence

- Implement big data analytics for selected use cases

- Look for extra data integrations via APIs

- Embed data analytics into new customer products

- Decide which hardware can help you gain missing insights

Long-term: Technologies for transforming insurance business models

Customer-focused, digital-driven operations today, adoption of emerging technologies tomorrow — that’s the principle insurers should operate by.

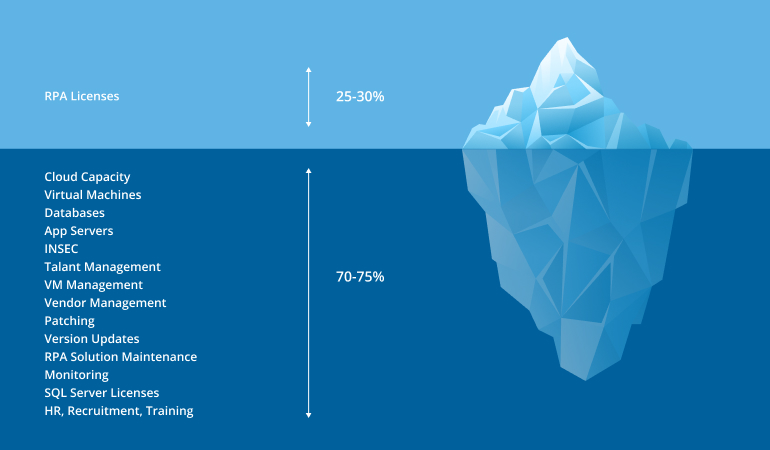

All of the technology trends in the insurance industry require a spectrum of IT architecture transformations to deliver the promised results:

But the good thing is that once you deal with the bottom of the iceberg and prepare the base, there are few to no blockers on your way to pursuing innovation — and getting tangible returns on tech investments.

Here are four technologies that can unlock new profit pools in digital insurance.

IoT devices

IoT devices are compact, low-energy sensors that can be attached or embedded into different gears for data collection. With the help of IoT and edge devices (sensors with computing capabilities), insurers can collect:

- Environmental data: Temperature, pollution levels, moisture level

- Movement data: Latitude and longitude, cardinal direction of movement

- Health data: Daily activity levels, heartbeat, blood pressure

- Property data: Movement detection, energy use, thermal efficiency

All of this data can then be incorporated into parametric and/or personalized insurance products — and used for faster claims management. Also, extra data enables insurers to predict and mitigate risk by proactively notifying policyholders about possible mishaps. For example, based on thermal efficiency data, you can notify commercial building owners about possible system malfunction before it manifests in an accident.

Similarly, IoT data can be extremely valuable for cargo insurance, as it lets you track the exact transport conditions of goods and notify shippers of mishandling. This use case is particularly promising for cold chain logistics, where precise transportation conditions are crucial.

Telematics

Telematics data, collected by many automotive companies, can supply insurers with knowledge about customers’ driving behavior (which is the top cause of accidents). With this knowledge, insurers can offer lower premiums to careful drivers and establish claims liability.

For instance, connected insurance startup Flock offers on-demand car insurance products, where coverage kicks in once the vehicle starts moving. The team relies on telematics and geolocation data to track vehicle use and driving behavior in real time. Then it bills the customer once the ride is over. This degree of flexibility is attractive for occasional drivers who don’t want to pay for a monthly/annual policy, as well as for the growing ecosystem of shared MaaS asset providers.

On-board vehicle diagnostics and performance metrics can also help insurers design more attractive products for commercial fleet managers and logistics companies. Apart from personalizing policies to drivers’ behaviors, companies can leverage telematics data to suggest maintenance — and thus reduce the volume of preventable insurance cases.

GIS data

A geographic information system (GIS) helps to collect, analyze, and visualize geospatial data. For P&C insurers, GIS is a more comprehensive alternative to human-led inspections. Geospatial data also comes in handy for predicting natural risks and conducting large-scale assessments of affected areas.

In the first quarter of 2024, insured losses from severe convective storm activity, winter weather, and flooding across the US were estimated at $13 billion. This is significantly higher than the 21st-century average of around $7 billion. GIS enables insurers to predict and plan ahead for such risks (and adjust premiums accordingly).

GIS data can also help prevent crop insurance fraud. Using infrared imagery, insurers can verify and measure vegetation growth without in-person visits — and offer better premiums to farmers.

AI and ML

AI is one of the major insurance technology trends. All of the above emerging technologies supply better data to insurance providers. Meanwhile, AI and ML algorithms help translate it into targeted actions.

The most high-value use cases of AI in insurance include:

- Risk prediction. ML and DL-based systems can perform complex multivariate analysis of various risk factors to provide agents with high-level and granular insights for decision-making. You can perform both historical analysis and future outcome-based modeling to decipher how various factors will affect tracked risks. Then you can adjust your premiums and customer offerings accordingly.

- Underwriting. This is another popular application of AI in InsurTech. By developing individual buyer profiles based on collected internal and external data, insurers can make instant underwriting decisions and adjust pricing. Automated underwriting can also help build personalized quotes and policy coverage for buyers to improve conversion rates.

- Claims management. Intelligent automation can streamline claims routing and validation by automatically filling in data and verifying its accuracy. Natural language processing (NLP) and optical character recognition (OCR) can also help process unstructured data inputs from clients to increase review speed and accuracy. At the same time, algorithms can provide more accurate loss estimates (using device-supplied data) to ensure fair claims settlement.

AI technologies, including generative AI, have a strong potential to transform the insurance sector. So it’s hardly surprising that 74% of insurance leaders plan to increase spending on AI projects this year according to Deloitte. But almost an equal amount (72%) also plan to invest more in cloud computing and storage, while 69% are ramping up their data acquisition and processing capability. Let’s talk about these technologies next.

Big data

Big data is crucial for any digital insurance strategy, serving as the foundation for AI-driven analytics. Without collecting and leveraging available data, achieving true digital insurance capabilities is impossible.

The process starts with gathering core digital data from various sources, both internal and external. Internal sources include customer details, policy information, claims history, and transaction records. External sources encompass data from third parties such as credit bureaus, public records, social media, and IoT devices like vehicle telematics and smart home sensors.

Once collected, the data is processed by storing it in data lakes or warehouses, cleaning it to remove errors and duplications, and transforming it into a usable format. This prepares the data for analysis.

The analytics phase relies heavily on AI, including descriptive analytics to understand past trends, predictive analytics to forecast future events, and prescriptive analytics to receive recommendations on the best courses of action.

Cloud capabilities

Cloud technologies are pivotal to the digitalization process in the insurance industry. They provide the infrastructure and tools necessary to leverage big data and adopt new technologies.

According to McKinsey, cloud computing benefits insurers in two major ways. First, it facilitates rejuvenation by reducing costs and mitigating risks. Cloud resources allow insurers to easily scale their digital ecosystem to meet high demand and expand operations without physical constraints. There’s no need to invest in and maintain hardware like servers and storage; the cloud provider manages these aspects.

Second, cloud technology drives innovation. Unlike traditional on-premise systems, which can limit the adoption of new technologies and scaling options, cloud computing enables seamless integration of advanced tools such as AI, big data analytics, and IoT. This flexibility supports the development of new business models and services, helping digital insurers maintain a competitive edge.

How to become a digital insurer?

Becoming a digital insurer isn’t just about implementing new technology—it requires a strategic shift in how your business operates and interacts with customers. Here are key steps to guide your transformation:

- Secure stakeholder buy-in: Ensure strong support from top management. Their active leadership and decision-making are crucial for driving the digitalization process forward.

- Redefine your business model: Transition from a product-centric to a customer-centric approach and move from manual processes to digital-first operations.

- Create a digital insurance strategy: Set clear, measurable goals and develop a detailed roadmap for implementing digital initiatives. This roadmap should outline the steps and timeline needed to achieve full digital transformation.

- Foster a digital-first culture: Cultivate a culture that embraces digital innovation and continuous learning. Provide training to equip employees with the skills necessary to work within the digital ecosystem.

- Develop strategic partnerships: Partner with experienced technology providers, like Intellias, to gain the support and expertise needed for successful digital transformation.

It’s also important to be prepared for the challenges that come with this transformation.

Transforming into a digital insurer: Key challenges

Data privacy and security

Digital insurance providers manage large amounts of sensitive personal information. If this data isn’t properly protected, it can lead to financial penalties, reputational damage, and a loss of customer trust. To avoid these issues, digital insurers must be proactive and invest in robust cybersecurity measures, including encryption, secure access controls, and regular security audits. Additionally, they must ensure that all data handling practices are transparent and comply with legal requirements, such as the GDPR.

Legacy systems

Insurance companies often focus on adopting new technologies but overlook the challenges posed by existing legacy systems. Outdated software can be difficult to integrate with modern digital solutions, potentially slowing down your digital transformation efforts. Therefore, it’s crucial to take a phased approach: start by modernizing your legacy systems before introducing new innovations. Skipping this step can hinder progress and limit the benefits of your subsequent digital initiatives.

Skill gap

The shift to digital insurance requires expertise in new technologies, data analytics, and digital customer service, which may not be present in your current team. It’s essential to invest in training and development programs to upskill existing employees. Additionally, you may need to hire new talent with experience in insurance technology, either directly or through an outsourcing provider.

Key takeaways

You don’t grow a tree from the leaves down. Without fertile soil and sufficient room for developing a strong root system, you can’t grow an orchard. Similarly, digital insurance transformations should be established from the bottom up:

- Prepare the grounds first — establish cloud connectivity and address gaps in existing IT architecture.

- Then help your root system develop — optimize and digitize existing business processes.

- Next, shift to the front office and look into digitizing customer channels and establishing a robust customer data collection pipeline. Cultivate it further by integrating data from third-party sources via APIs.

- Once that’s done, you’re ready for cross-pollination. Identify gaps in operational knowledge and determine which emerging technologies could help you fill them.

- Finally, pull your new digital insurance system together with AI algorithms to cover the remaining manual steps in standard workflows.

To successfully navigate this transition, be prepared to shift your business from a traditional model to a digital-first approach. Partnering with an experienced tech provider is also key to making the right technology decisions and staying on track.

Contact Intellias to discuss your digital maturity level and growth potential.