Ever read Alice in Wonderland? The deeper Alice progresses into Wonderland, the fewer things she considers impossible. The insurance sector has gone on a similar journey of self-discovery over the past several years.

Many who viewed remote work as improbable before the COVID-19 pandemic had to make the switch as soon as lockdowns began. Others who previously believed their policies made a digital customer journey impossible successfully switched to providing online service.

Innovation in the insurance industry might be less visible for users, but it sure does happen in the background. We break down why there’s no use for the insurance sector to go back to yesterday’s practices and where it’s heading instead.

Insurance resilience in the digital-first world

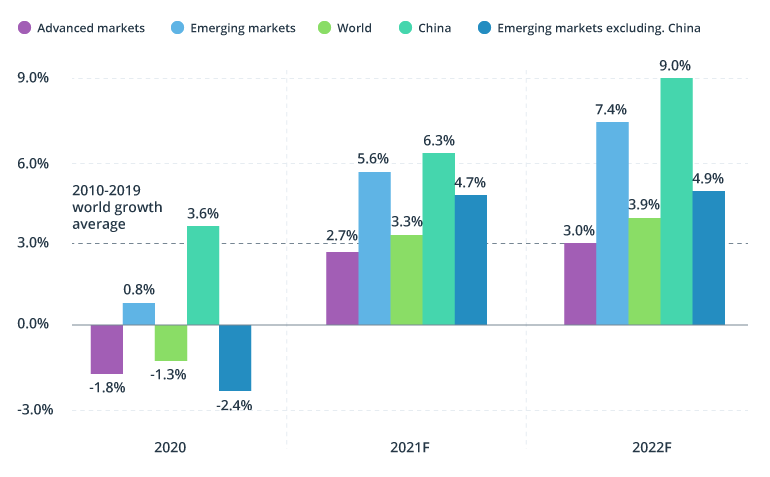

Insurance markets have had a bumpy period in the past year: claims volumes are up by a sizable notch, life insurance payouts saw the biggest spike in the past 100 years, and the overall risk radar across regions has expanded.

Despite all these calamities, most insurers are back on the high-growth track.

Source: Deloitte – 2022 Insurance Industry Outlook

Dwindling premiums and reduced profitability aren’t the only defining characteristics of the “new normal.”

Similar to other industries, the insurance industry has gotten a strong taste of the remote — and subsequently hybrid — reality. In a matter of weeks, most businesses had to close offices and switch to fully remote operations (insurance offices included).

Despite making tempered progress, digital innovation in the insurance industry was far less sweeping compared to innovation in adjacent financial sectors like banking, payments, or wealth management.

In 2018, half of the insurance leaders surveyed by PwC said they were “extremely concerned” by the speed of technological change. At the same time, 72% admitted they were relying on “organic growth” as their prime method for generating revenue and didn’t place technology investment higher than other priorities.

This sentiment makes perfect sense. Insurance companies weren’t as severely undercut by tech players as their counterparts in finance. The sector has fewer digital-first players, challenging the status quo and raising the bar for customer experience (CX).

Unlike finance, InsurTech players didn’t go for the highest margin revenue lines and mostly concentrated on lower-entry, consumer-facing products such as renters’ and homeowners’ insurance (Lemonade), auto insurance (Clearcover), or travel insurance (Insured Nomads).

Digital transformation in traditional insurance companies happened at a leisurely pace: there wasn’t a rush to adopt new back-office technologies or push digital products to the market.

Then the tide changed in 2020. Businesses and consumers alike switched to online mode. Everyone now wants to get things sorted online, without lengthy trips to the branch for selecting a policy or in-person claims submission.

41% of consumers say they are likely or more likely to switch insurance providers due to a lack of digital capabilities.

The insurance claims management process itself underwent major transformations: submissions come from different channels, B2B clients demand streamlined integrations with their data systems, B2C consumers want convenient online tools and fast issue resolution.

These mounting pressures have fostered a new wave of insurance industry innovation — one that’s focused on rewriting business processes that hinder operational effectiveness, service-level agreement (SLA) compliance, and growth potential, with and without technologies.

Key priorities for insurance business transformations

- Achieve better operational and business resilience against market disruption

- Improve service delivery and product design

- Strengthen cybersecurity protection of new digital processes and systems

- Align rules management and insurance policies with new market realities

- Accelerate the detectability of and response times to early market signals

- Reduce the friction in service acquisition and delivery

- Reposition the business to retain existing customers and attract new demographics

3 defining insurance industry trends to infuse resilience in your business operations

The insurance sector had an obvious rough patch, but the future of the industry is not just shaped by macroeconomic events.

Ongoing calamities have turned manageable issues — like low operational efficiency, long processing times, and immature digital capabilities — into pressing problems. Without addressing them (and doing so fast), insurers risk a longer recovery period and reduced revenue.

Over $200 billion in revenue will emerge from technology-enabled products and services, value-added services, and monetization of data and technology until 2025.

What will shape insurance transformation in the short-term perspective and impact long-term industry prospects? We’ve mapped three main forces.

Customer experience (CX) will become a strong competitive point

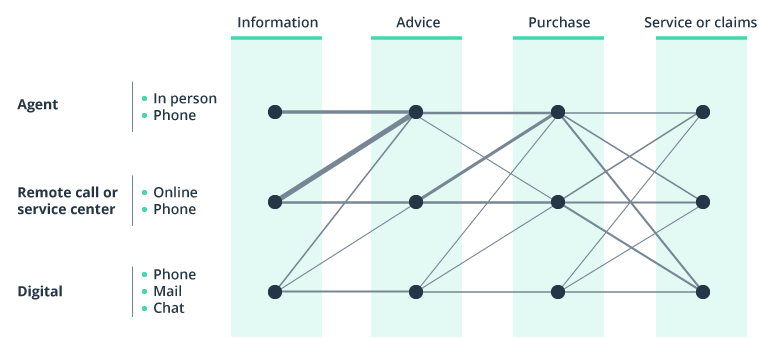

Insurance is no stranger to online and even mobile sales — the two channels most companies have already set up (and profit from to an extent). But CX is more complex than just allowing people to chat with agents online or purchase a policy via an app.

Modern tech-savvy consumers interact with insurers across multiple channels because that’s how they’re used to interacting with other service providers:

Source: McKinsey – The multi-access (r)evolution in insurance sales

However, omnichannel interactions aren’t an area where most insurers excel.

A study of Belgian BFSIs, conducted by SIA Partners, found that most bank insurance players such as BNP, CBC/KBC, Belfius, and ING allow consumers to complete most steps of their customer journey online. Traditional players like AXA, AG Insurance, and Allianz, among others, eventually add possibilities to call an agent, visit an office, or mail paper forms.

What’s wrong with that? you might be wondering. At least we are doing something online. That’s admirable, but soon such online services might not be enough to attract and retain new demographics.

We don’t want to make this about generations, but… the average age of a life insurance agent in the US is 59, and agents tend to sell to consumers within five years of their own age. At the same time, the largest gaps in life insurance coverage are among Millennials (44%), Gen X (44%), and Gen Z (45%).

Members of these generations don’t begin their purchase journey with a visit to the branch. According to PYMNTS research:

- 39% of bridge Millennials search for life insurance options on the web.

- 35% of Millennial and Gen Z consumers prefer a hybrid approach combining in-person sales and online information.

Digital hasn’t just supplied us with new technologies for doing things — it has led to seismic mindset changes in how we expect businesses to connect, engage, and sell to us. The new generation of shoppers expects Amazon-like experiences for purchasing policies and receiving subsequent services.

70% of Millennials said they’d be more likely to buy life insurance if they better understood offerings and benefits, while 67% would if the process were faster or easier.

Why do insurers struggle to connect with new audiences? Because most don’t have processes conducive to speed, scale, and personalization that modern consumers demand. Rethinking your processes and policies from the perspective of customer-centricity should be a pillar of any insurance company transformation.

Transition to ecosystem thinking in product development

Consumers want better products and fast online services. Great! So let’s build new digital products for the front and back office!

That’s a good idea, but a somewhat premature conclusion. It may be tempting to rip out a legacy IT system and replace it with a newer component to power a flagship digital insurance product.

Indeed, 70% of insurers’ IT budgets are tied to maintaining legacy systems. But let’s backpedal and think why this happened.

Back in the day, your company decided to build an in-house product, let’s say an interface for rapidly issuing malpractice insurance for small business owners. Ten years down the road, it brought revenue and loads of new customers. But with every year:

- the IT architecture became less reliable and couldn’t handle increased loads

- app availability and performance metrics dipped

- scheduled maintenance and periods of downtime grew longer

- IT engineers who knew the programming language began to retire

As a result, you have a once glorious in-house tech product that requires expertise no one on the talent market has, money that could be better spent elsewhere, and modernization that’s hard to execute because of the system’s age and complexity.

Product innovation in insurance can’t be a closed loop. When you develop fully custom IT systems, you put the ability to integrate new data, features, or third-party partners at major risk. Scaling custom systems is hard (if not fully impossible), and re-architecting them is too expensive.

For these reasons, many insurance companies size up platform business models instead. By selecting this business model, you can effectively combine in-house systems (and products) with modular offerings from InsurTech players. That’s a more viable strategy to innovate insurance services at a steady speed and at moderate cost.

76% of insurance executives say “getting transformation right” will require new ways of innovating with ecosystem partners and third-party organizations.

A platform business model (and supporting IT architecture) also serves as a gateway to economies of scale — the ability to improve profit margins through scaling your distribution capabilities across multiple axes.

A platform architecture allows you to connect more players into your ecosystem and aggregate services. Likewise, you can gain missing digital capabilities by embedding software components from other players. Or, on the contrary, you can rent out some of your systems to strategic partners (e.g. banks) for them to incorporate into their product portfolio. All of these approaches require a mature API strategy as well as a technology partner who can evaluate your existing IT architecture and determine the necessary scope of transformations.

Outcome-based approach to adoption of emerging technologies

No industry conversation about insurance transformation can happen without mentioning emerging technologies: blockchain, IoT, drones, augmented reality, artificial intelligence.

Indeed, 80% of insurance leaders now view their organization’s business and technology strategies as inseparable. While we do agree that tech and operations are connected at the hip, it’s important to draw the line between them.

Think of this relation as a standard city layout. In some areas, two roads run in parallel, then merge into one highway only to break off at the next intersection.

While technology can (and should) augment your business operations, it’s not a self-contained solution to all your operational issues.

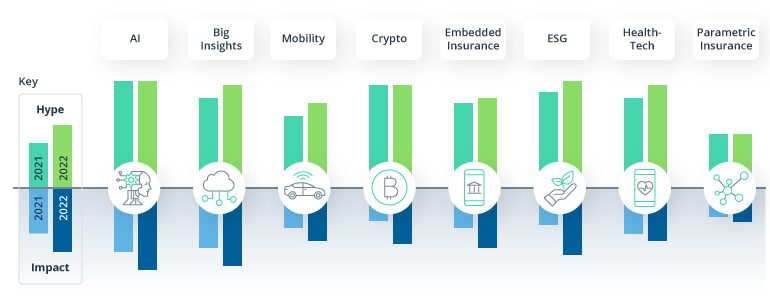

The hype and excitement about the possibilities of emerging tech — be it AI for claims processing or telematics data for usage-based insurance — often goes beyond the tangible impact these solutions deliver on the market.

That’s why Gartner often pegs the timeline between “innovation trigger” and “slope of enlightenment” (actual value generation) at 10 to 20+ years — if the technology survives the disillusionment phase.

Source: InsurTech Insights – Insurtech 2022: Hype vs. Impact

So how should you place your bets on innovation?

Think from the perspective of desired outcomes. Technology is a tool for achieving your goals — but if those are murky, your results will be too.

As you lead internal conversations about insurance business transformation:

- Determine your most pressing issues

- Pin down desirable outcomes

- Analyze which tech stack will bridge them

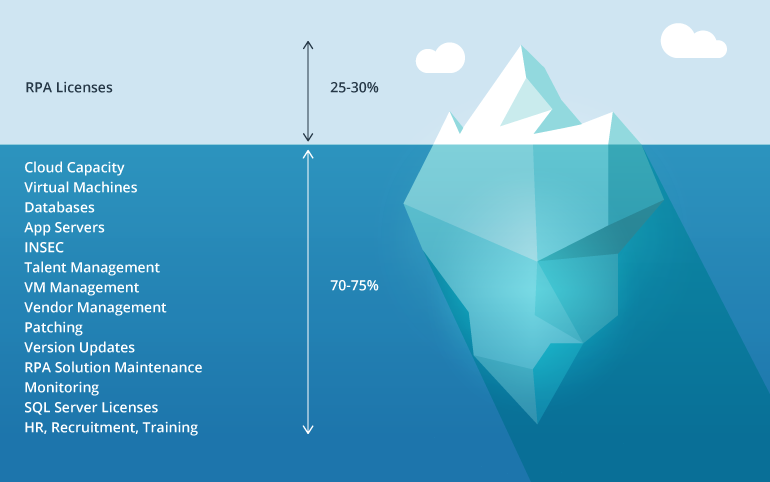

For example, the rates of robotic process automation (RPA) and, more recently, intelligent automation (IA) adoption have been at a record high in the insurance industry compared to others. Why? Because RPA solves a very acute problem — the need for better operational efficiency.

RPA can reduce average claims filing times by 25% and drive a 94% first-pass yield.

So once again, hold the magnifying glass over your business processes. Where do most of the bottlenecks occur? Why do they happen? What can you change process-wise without increasing risks? Which data do you need for faster and better decisions?

Once you get answers to the above, you can start vetting different technologies and assess their impact.

For example:

- Siloed data access can be resolved by developing a cloud data management platform

- Long document processing can be optimized with RPA, natural language processing (NLP), and optical character recognition (OCR)

- Endless waiting on partner organizations can be fixed by establishing API-based integrations between your systems

The key here is to understand the strategic business value behind the technology, then progressively adapt your operations and IT systems to become a better fit for new technologies.

After all, most technologies require a wide spectrum of supporting transformations to deliver on the advertised benefits:

Your goal is to holistically assess if the perceived benefits fully compensate for the hidden costs of adoption.

Innovation in insurance starts with business, not technology

The insurance sector is finally grappling with the manifest needs the pandemic has brought to light. For many, the rapid transition to remote work was a nerve-wrenching test of operational resilience. For others, it revealed the magnitude of sweeping changes coming to the industry.

No, branches and insurance agents aren’t going to be replaced by AI and robots. But existing business processes will need to be adapted to match new consumer preferences and market realities. Understandably, technology will play a key role here, but it will fail to bring tangible changes without a future-oriented operational strategy.

Intellias is a strategic consultant and technology partner to Fortune 500 BFSIs. We help businesses address real market problems with fit-for-purpose technology solutions. Contact us to discuss strategies for insurance sector transformation.