On September 11, 1916, Tennessee entrepreneur Clarence Saunders opened the doors of his revolutionary store Piggly Wiggly — a place where you could come and pick your own products (across categories!) instead of relying on a clerk to assemble your basket.

Today, the supermarket shopping experience hardly feels novel. What’s more, we pretty much expect each type of business to offer us a roster of relevant products and services personalized to our needs. Plus, we expect to do so across physical and digital channels.

And when one company can’t meet all our needs, we quickly google another.

If public transport is crowded, we get an Uber. If the local store is out of our soap, we order it on Amazon. If our primary bank doesn’t have trading functionality, we try an app instead.

The grass is greener fallacy (paired with effective marketing) has prompted us to seek better experiences for whatever we do.

In the financial industry, this has led to two things — the FinTech boom and then the progressive rise of digital financial ecosystems.

What is a financial ecosystem?

There are two ways to interpret a financial ecosystem:

- As a business model, a financial ecosystem is an open-ended, multi-dimensional network that allows participants to generate value vertically and horizontally. It encourages participants to take advantage of one another’s strengths to access new target demographics, collaborate on new offerings, improve the customer experience, and boost bottom-line profitability.

- As a technological construct, a digital financial ecosystem is a modular, cloud-based IT architecture pattern that leverages a microservices architecture, APIs, and data analytics to enable effective collaboration between participants.

Both definitions sound complex, right? Here’s a simple analogy to explain the concept of a financial services ecosystem.

Let’s picture an ideal coffee shop.

You order ahead through an app (built by a tech partner). After picking up your brew (an in-house product), you settle in to do some work on your laptop. This coffee shop has excellent free Wi-Fi, courtesy of their telecom partner.

The morning goes by, and before you know it, it’s almost noon and you get a ping from the coffee shop app offering to schedule a free lunch delivery since the coffee shop doesn’t have a kitchen (channel partnership). In 20 minutes, you get your poke bowl and pay for another drink from the bar using the coffee shop app.

When you’re ready to wrap things up, it starts raining. You live several blocks away and don’t feel like walking. Once again, the coffee shop app gives a quick ping and offers to call a ride.

On your ride home, you think about how a single company — the coffee shop — fulfilled six different requests for you.

Now, the world of finance is more complex than ordering a coffee.

But a similar dynamic is at play: consumers have a wide range of ongoing and spur-of-the-moment needs you can meet through technology and channel partnerships.

In fact, that’s what many successful FinTech ecosystem players already do:

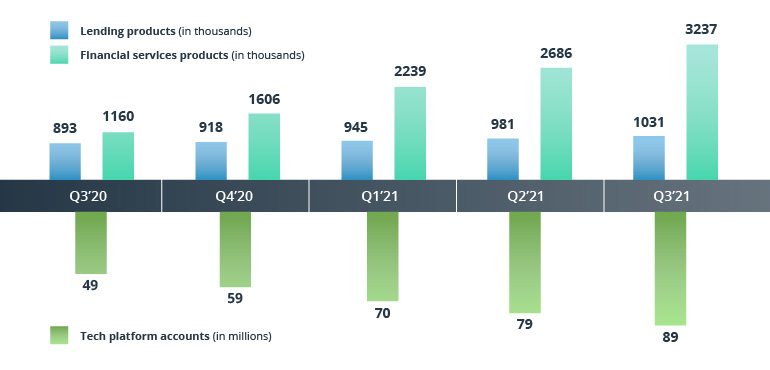

SoFi

Source: Partnerbase

SoFi leverages technology and channel partnerships to deliver a one-stop-shop experience for their customers. Savings, lending, insurance, mortgage, investing — you get a complete service through one interface (but not always from the same provider).

And this market strategy is paying off.

In 2021, SoFi attributed their double-digit (and even triple-digit!) year-over-year growth in members, revenue, and product adoption rates to their Financial Services Productivity Loop (FSPL) that “creates a compounding effect on member referrals, greater adoption of multiple products and cost-efficient scaling of our broad-based offering.”

Source: SoFi — SoFi Technologies Reports Third Quarter 2021 Results

Why the finance industry drifts to ecosystem thinking

They say finance is a “traditional” world.

Indeed, many of the core tech advancements in the industry date back to the 1960s to 1970s: ATM technology, the SWIFT payment system, IBM mainframes for core banking systems. Many banks are still tied to their legacy back end.

At the front end, the branch was historically the main hub for interactions. Need to deposit money? Go to a teller. Want to trade some assets? Call your personal manager.

All things went well, but then the 2008 financial crisis hit and many of the underlying back-office inefficiencies came to light.

Consumers lost trust in financial institutions. They also grew progressively disenchanted with the lack of convenience, low transparency, and oftentimes inaccessibility of banking services.

By the mid-2000s, the first FinTechs started to emerge.

What initially appeared like a “closed,” regulated industry no one liked soon became one of the fastest-growing market verticals.

Between 2010 and 2017, over 1,470 FinTech companies, specializing in banking and capital markets, were founded globally.

By 2021, 96 FinTech unicorns had amassed a collective worth of $404 billion. And the growth is far from slowing down.

The global FinTech market will reach $190 billion by 2026, growing at 13.7% CAGR. The US, the UK, China, Germany, and India are the largest FinTech markets.

Understandably, banks couldn’t ignore the booming FinTech ecosystem.

Some felt threatened. Others felt defeated. Many were bullish for mergers and acquisitions as a means to stave off competition.

And the smartest? They understood early that the financial ecosystem transformation is inevitable.

Because this is what connected consumers want.

The big wave of “unbundling” that FinTechs started has pushed people to hoard financial products — one for saving, one for travel rewards, another for investing, an app for sending payments. Then consumers started thinking about how to link all those options back together for more convenience.

It’s now apparent that what we really crave is not more options per se but continuity and breadth of financial service delivery.

You can call it a “one-stop-shop,” “Amazonification,” or anything else, but consumers have had their say.

According to various sources:

- 40% of Americans have more than one bank account because their primary financial institution doesn’t offer fully integrated services.

- 76% of US consumers name “the ability to connect my accounts to apps and services” as an important criterion for choosing a bank.

- 7 in 10 consumers say they value ecosystem offerings that improve their buying journey.

So where does this leave us?

In an emerging era where mature FinTechs, TechFins, digital-forward banks, and anyone in between is joining forces to operate as digital financial services ecosystems.

Financial players are now choosing cooperation over competition. Because growing jointly in an equitable partnership is easier than excelling across all touchpoints and product categories on your own.

Since before the pandemic, banks have been under pressure to digitize and innovate the customer experience. From improving digital account opening processes to adding new in-demand customer products for wealth management, trading, and lending — the list of projects was long, but the development speed was slow.

So instead of doing everything on their own, the frontrunners turned for help to technology and channel partners — from hyperscalers to newly minted financial technology companies and API providers.

Bit by bit, the biggest global banks are also turning into a patchwork of interconnected services delivered by a cross-section of partners.

For many, this has led to:

- Lower customer acquisition costs because of improved digital acquisition and new channel partnerships

- Higher customer lifetime value (LTV) thanks to better retention, personalization, and cross-sells

- Faster time to market for new products due to greater reliance on APIs and Agile in finance principles

- New revenue streams, courtesy of both technical and business model transformations

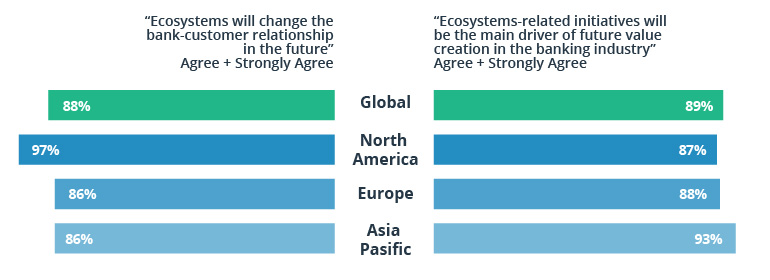

Based on the above, it’s not surprising that nine out of ten banks are strongly interested in forming or joining a customer-facing ecosystem.

Source: Accenture — Competing with Banking Ecosystems

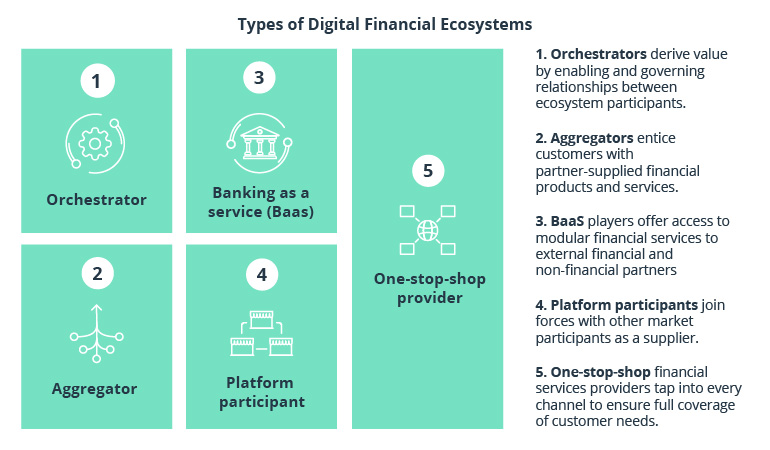

5 types of digital finance ecosystems shaping the future of finance

The power of an ecosystem lies in its unity. But it’s not easy to achieve consensus and equilibrium when more than two parties are involved.

Think of doing a seating chart for an event. You can’t put James and Jill together because they don’t talk to each other. Andy gets along well with Sam unless Paula is around. Then when Natalie and Paula get together, they always talk Jill and James into some crazy debate.

You try to work out the magic combination where everyone is happy.

The same level of operational and technical considerations go into determining the shape of a financial ecosystem.

There are some working “seating charts” you can swipe from other players.

Orchestrator

An orchestrator enables collaboration between different ecosystem participants. Think of an orchestrator as an event management company — they provide a venue, organize a line-up of performers (partnering companies), and help ensure that visitors (consumers) get the best experience possible.

Many platform businesses outside of the banking market — Google, Facebook, Uber, and others — successfully pursue this route.

But so do some FinTechs, especially in the payment space.

For example, Plaid (acquired by Visa) has built a lucrative business of integrating everyone with anyone. Through their API-based platform, you can build bridges to 11,000 banks and financial service providers.

Aggregator

Aggregators derive value by providing customers with a collection of financial products and services. Plus, they get to accumulate rich data consumers provide them with when integrating their accounts.

Some aggregators are pure play solutions built for the sole purpose of product comparison, shopping around, and personalized deals. Credit Karma, acquired by Intuit for $7.1 billion, is a good example of how a simple credit check tool grew into a valuable digital FinTech ecosystem of lending products.

Then we have part-time aggregators, aka financial companies that chose to augment their core services with a partner’s offers.

This is better known as marketplace banking.

The marketplace banking model entails delivering a spectrum of complementary financial or lifestyle services to existing users through partners. Some partnerships are one way, i.e. the marketplace player is on the giving end and only profits from a referral fee paid by the partner.

Other companies opt for co-branding deals and exchange customers with one another. For example, a digital bank can partner with a wealth management tool and embed its services into the banking app. At the same time, they can rent out their card-issuing interface to all partners.

Who’s successfully doing marketplace banking?

- Digital-native Starling Bank runs a personal finance management marketplace and business apps marketplace

- The Brazilian bank Itáu launched a marketplace platform of non-financial business services for SMEs last year.

- Another Brazilian innovator, Nubank, went for an integrated ecommerce shopping section as part of its marketplace strategy

- BBVA spun this idea the other way around and placed an open call for FinTech startups to pitch their offers for products, services, or integrations

Banking as a service platform

Banking as a service (BaaS) is a business model digitally mature banks and FinTechs with a banking license pursue to partner with aspiring TechFins and non-financial players.

Thanks to microservice architectures and APIs, banks can now rent out their core services — from card-issuing to treasury management services — to anyone. Then they can charge a rental fee or establish more complex data sharing and consumer exchange deals.

Goldman Sachs officially moved into BaaS territory at the end of 2020 with the upgraded version of the Sachs Transaction Banking (TxB) platform. Already, they have scored several attractive partnership deals — a Stripe Treasury API service and high-yield savings accounts with UK digital bank Saga. BBVA, Barclays, JPMorgan Chase, and Green Dot Corporation are three other top-ranked players in the BaaS space. Even more will join soon.

The global demand for BaaS services among FinTechs is projected to grow at a CAGR of 17% between 2021-2031 with sales figures to surpass $12.2 billion by the end of 2031.

Platform participant

At the same time, you can also be a performer in someone else’s show. Joining an existing financial or non-financial ecosystem can be extremely lucrative.

Citigroup is good at playing this game. In mid-2020, the company rolled out a buy-now-pay-later scheme with Amazon, offering instant installment plans for big-ticket Amazon purchases to Citibank cardholders (to stave off revenue erosion by BNPL companies).

Another lesser-known example is provided by Lincoln Savings Bank, a 120-year-old financial institution born in Iowa. While boasting relatively modest retail customer numbers, Lincoln Savings Bank is the bank partner for big-name FinTechs like Qapital, Money Lion, Acorns, and Cash App, and is an active participant in their ecosystems.

Similarly, a lot of FinTechs choose to team up as marketplace partners to receive a new avenue for acquiring users.

One-stop-shop provider

Becoming a one-stop-shop provider for an array of financial and lifestyle needs is the destination many digital banks aspire to reach. Apart from SoFi, mature digital players like Revolut, Chime, Monzo, and N26 are progressively expanding their product portfolios through in-house and partner-supplied offers.

Traditional banks such as Wells Fargo are also pursuing a similar route by simultaneously expanding their customer-facing offerings and building out BaaS offers for B2B partners. In 2021, they launched an SDK and a set of APIs that allow partners to embed a credit card application in their transaction flow. That’s on top of other API products that are already available.

The difference we see between digital-native and traditional banks is this:

The first group has the advantage of a modern, modular technical architecture that is well-suited for rapid prototyping and experimentation. Digital-native banks can quickly build new features (often using partner-supplied solutions). Then they can easily integrate with other players. But many digital-native institutions lack the trust and liquidity big banks have.

Digital banks also have the disadvantage of being used as a secondary/complementary account. Per a Galileo 2021 survey, only 21% of US consumers use a digital bank for their primary account versus 65% who use a traditional bank.

But 77% of adults who use traditional banks as either a primary or secondary account also store 43% of their funds elsewhere.

And this creates an interesting dynamic: each type of provider (FinTechs, digital and traditional banks) only gets to see a slice of consumers’ financial lives.

As a primary bank], you know that I am doing things on Monzo, but you have no idea what, why, or where I’m doing it. In other words, the financial intermediary who never believed they would be disintermediated has been disintermediated by a new intermediator. A data intermediary. The lifeblood of the bank’s future – customer data – has been stolen by a new middleman: the intelligent intermediator.

But the stealing goes both ways, as digital banks and FinTechs don’t always get to view data from primary banking institutions.

Open banking and the rise of account aggregation offerings attempt to fix that to an extent.

However, the upper hand will still be had by players who manage to build successful cooperation with others to not just capture all consumers’ data but to turn it into a better, more personalized, and more efficient customer experience.

Getting started with the financial ecosystem model

As we’ve talked about above, there’s no single scenario for building out an ecosystem.

Market leaders combine several options — a platformization strategy plus marketplace banking or banking as a service and aggregation.

What stays the same in each case is that you need to:

- Analyze your current data management system and locate inefficiencies and missing sources

- Assess your current IT infrastructure to determine the scope of necessary changes for platform development and API integrations

- Review available Open APIs to determine which features you can rent rather than build

- Determine which features you can develop/upgrade in-house and perhaps “rent out” to partners

- Examine which technology and channel partners can help you meet your current goals and/or provide access to innovation

- Infuse extra flexibility and agility into your development process to deliver on your goals at warp speed

The above is just a high-level outlook. Clearly, there’s a wide gap between having an idea for a financial ecosystem and breathing life into it.

However, it’s comforting to know that you don’t need to go on this journey alone. Team up with a technology partner to figure out the development aspects of your plan. Select channel and business partners with expertise that complements yours.

Stay focused on the “co” in the ecosystem — collaboration, co-existence, and continuity!

Intellias is a technology partner to market-leading FinTechs and Fortune 500 BFSI companies that are looking to link their innovative thinking to technical expertise. Contact us to talk about your new market strategy.