A customer experience (CX) now trumps price and product as the biggest brand differentiator in nearly every industry, and insurance is no exception. Customers today demand seamless, personalized experiences comparable to those provided by tech giants. Telematics insurance solutions can help insurers meet these expectations.

Technology is already making a huge impact on the insurance industry. For example, digital has become the preferred channel of interaction for many consumers. A 2022 SwissRe consumer survey found that 48% of respondents purchased policies via an insurer’s app or website, while only 45% bought them from an agent or broker.

Meanwhile, a car is no longer just a set of wheels and some machinery under the hood. Modern vehicles are connected devices equipped with advanced electronics, real-time connectivity, and robust computing power.

By 2030, 50% of vehicle value will come from electronics and embedded software.

The above dynamics, paired with other market factors, put insurers at a crossroads. They can keep driving down the traditional route, offering customers frustrating policies and high prices. Or they can take a promising turn toward the emerging market of telematics insurance.

In this article, we’ll explain the basics of telematics for insurance businesses, outline current market trends, and show how auto insurers and car manufacturers can benefit from this technology.

![[whitepaperbox link="https://intellias.com/ebooks/ai-insurtech-embrace-the-tech-revolutionizing-insurance/" imageid="74480" title="AI Insurtech - Embrace the Tech Revolutionizing Insurance" ]Everything You Need to Know about the Insurance Industry and Artificial Intelligence[/whitepaperbox]](https://d3twecw9qvot3u.cloudfront.net/wp-content/uploads/2024/05/AI-Insurtech-cover-1.png)

What is telematics insurance?

Telematics insurance is an innovative form of auto insurance. It uses technology to monitor the customer’s driving behavior and offer usage-based (UBI) policies considering this information. Thus, drivers can benefit from personalized premiums.

A key component of telematics auto insurance is telematics data, which is the detailed information on various aspects of driving collected from vehicle devices. Examples of telematics data points include:

- Vehicle status (RPMs, fuel consumption, engine load, state of charge for EVs, etc.)

- Asset usage (driving time, distance traveled, average speed, etc.)

- Vehicle maintenance (OBD diagnostic trouble codes, failure type information, parameter IDs, ECU information, etc.)

- Driving patterns (braking, acceleration, cornering, speeding, etc.)

So, in simple terms, telematics provides detailed information on what happens to a car over its lifespan. Meanwhile, insurance companies use this data to create personalized rates and offers for their customers.

How telematics insurance works

Vehicle telematics is made possible by a device that collects, stores, and exchanges data about vehicle use. This device can be either built-in or external. Built-in devices installed in the vehicle by automotive companies (OEMs). Meanwhile, external devices include mobile apps or onboard diagnostics (OBD) plug-ins that insurance providers connect to the car’s OBD-II port.

A telematics device gathers driving data and transmits it to the insurance provider via mobile networks or Wi-Fi. The insurance provider then analyzes this data to assess the driver’s risk profile. Based on the analysis, the company calculates personalized premiums.

With insurance telematics, save drivers get more favorable rates. A telematics policy can also be reviewed over time, allowing rates to be recalculated based on the most recent driving data.

How does insurance with telematics differ from traditional auto insurance? Traditional premiums are based on broad risk factors, some of which aren’t related to driving, such as age, gender, or credit score. As a result, safe drivers may end up in high-risk categories, while customers with dangerous driving habits may be underpriced.

Telematics for insurance: The way to easier distribution and competitive policies

Automotive companies already possess a wealth of information — and they will soon get even more.

By 2024, 83% of all new on- and off-road vehicles will have OEM-embedded telematics according to PTOLEMUS.

Insurers can use this data to create more competitive policies for consumers. Drivers always look for more favorable rates, while telematics in auto insurance often means lower premiums.

In the UK, telematics (or black box insurance) policies are already the cheapest option for two-thirds of younger drivers (aged 17–20), who can save as much as £1,307 annually over traditional policies. Over 40% of older drivers can also get premium discounts from such policies. Commercial fleet managers, in turn, gain even more perks from using telematics apart from lower premiums.

Using telematics for fleet management gives businesses even more advantages. Apart from lower premiums, they benefit from vehicle efficiency optimization. Specifically, telematics for fleets allows fleet managers to gather critical vehicle data that can be used for improving asset tracking, fuel management, truck dispatching, and more.

And yet the global usage-based insurance (UBI) market was a “modest” $18.9 billion in 2021 against the global $777 billion general auto insurance market.

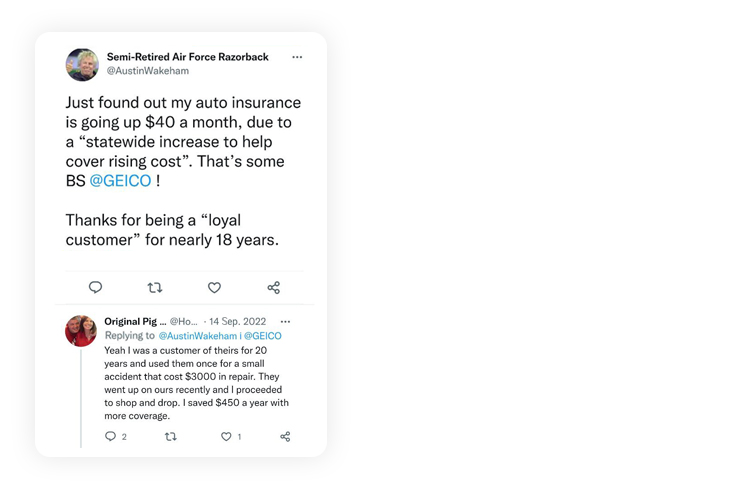

In 2022, auto insurers are once again upping premiums (by 4.9% nationally in the US), much to consumers’ dismay:

Sources: Twitter, Twitter

Sure, insurers need to absorb the costs of higher second-hand car prices, more expensive vehicle repairs, and other market forces.

But short-term price hikes won’t protect insurers against larger disruptions such as a decreasing car ownership rate (peak car) and a progressive transition to shared mobility.

In Western countries, the average distance traveled per person by car has been flat or falling since the early 2000s. In the UK, the average motorist drove 7,600 miles in 2018, down from 9,200 in 2002.

The 2030 UK ban on the sale of new petrol and diesel car models and a similar EU measure that will take effect in 2035 will further shake up the auto insurance market.

On the one hand, these changes may leave some players with an unprofitable customer pool. On the other hand, a new generation of connected, autonomous, shared, and electric (CASE) vehicles can open a vast new revenue pool for the industry.

Source: McKinsey — Connected revolution: The future of US auto insurance

Currently, the automotive industry generates over 1 zettabyte (ZB) of data per year. By 2030, a single car will produce up to 10 terabytes of data per day.

Most of this data will be generated by connected car subsystems and sensors such as ADAS, Lidar, collision sensors, rear cameras, night vision systems, and front/rear object radar systems.

A substantial part of new vehicle data will also come from inside the cockpit, directly from the driver. In-car dashboards are morphing into a standalone, robust interactivity channel resembling a smartphone.

OEMs including Toyota, Mercedes-Benz, and Volkswagen plan to deploy a proprietary car operating system (OS) by the mid-2020s. Paired with branded companion apps, the car OS presents a new channel to build stronger relationships with consumers — and not just for OEMs.

Mercedes-BenzOS is a direct interface for customer-experience features, which will become the basis for all future Mercedes-Benz vehicles as a unique and standard software platform. The MB.OS operating system will perfectly link the vehicles with the cloud and the IoT and comprise four central domains: Powertrain, Autonomous Driving, Infotainment, and Body & Comfort Systems.

By using proprietary vehicle software to gather car data for insurers, OEMs can assist their partners in reaching new customers and entering new markets.

How OEMs and auto insurers can jointly cultivate value from telematics data

The idea of entering the insurance market isn’t new for OEMs.

Daimler, VW, Porsche, and Toyota, among others, already have subdivisions in charge of financial and insurance (F&I) products.

This makes perfect sense, as vehicle and insurance policy purchases go hand in hand.

What’s more, 72% of US consumers factor in motor coverage costs when buying a new vehicle, and 71% of car buyers would like to get auto insurance at the dealership according to a Dealerpolicy report.

Yet selling policies is a cumbersome experience for dealerships. In fact, consumers perceive a dealership’s success rate differently than how the dealership perceives its success rate.

93% of dealerships believe they helped a consumer with insurance choices, but 49% of shoppers say dealers did nothing to assist with finding options.

In 2021, only 10% of US dealerships had a franchised insurance agency on-site, and 5% had an independent agency or agent available in the showroom.

OEMs are trying to rectify this issue by investing more in digital insurance distribution. Companion driver apps and onboard car operating systems can enable OEMs to seamlessly upsell F&I products to their customers at the most convenient time.

Tesla is said to be adding its insurance program into its smartphone app. Toyota launched an in-app usage-based insurance product in 2021.

Nearly every major OEM is now working on a digital customer platform — a consolidated gateway to all brand services, ranging from remote car diagnostics to navigation, in-car commerce, and, soon, embedded coverage policies.

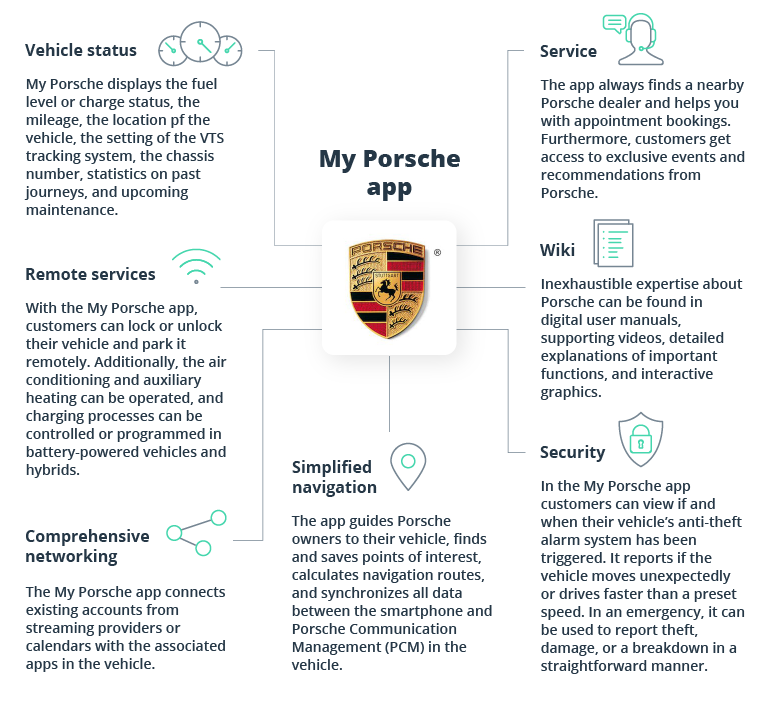

Redesigned Porsche customer experience platform functionality

Source: Porsche — New digital platform for all vehicle-related services

Insurers now have the opportunity to join these emerging ecosystems and forge profitable relationships with OEMs through:

- Entrusting OEMs with policy underwriting and claims management

- Designing exclusive usage-based and pay-as-you-drive insurance products for select partners

- Aggregating telematics data to offer preventive coverage policies

- Offering competitive reinsurance options for non-core exposures

In other words, auto insurers can switch from B2C sales to the B2B2C model, where they simultaneously sell to drivers directly and digitally distribute products to B2B partners — OEMs, auto dealerships, and aftermarket service providers.

Here are five models for OEM–insurance company collaboration that are rapidly coming of age across markets.

Usage-based insurance (UBI)

Vehicle data ranging from location and driving style to diagnostic insights and recent maintenance is a gold pit for insurers.

For one, telematics data can change the underwriting process. Instead of relying on vehicle build data (which may not age well for used cars) and self-assessments by the driver, insurers can go straight to the source of truth: the vehicle itself.

Telematics data enables insurers to build personalized risk profiles for each customer and extend tailored, competitively priced policies. Consumers already like the sound of emerging pay-how-you-drive car insurance offers.

Since the end of 2021, the number of customers offered a telematics policy to monitor their driving and help determine their rates rose from 32% to 40%—and the number of those who opted in rose from 49% to 65%.

For underwriters, telematics insurance enables more accurate, dynamic, and even real-time policy generation and updates. On the tech side, you can leverage big data analytics to perform real-time risk assessments for automatic underwriting and policy generation. Then you can use machine learning (ML) models to augment traditional statistical models for claims forecasting and subsequent claims management.

Telematics car insurance is also an attractive value proposition for the rapidly growing Mobility as a Service (MaaS) market.

Though personal vehicle ownership will likely decline, commercial CASE fleets will grow in number — a lucrative new B2B niche for insurers.

The balance of personal to commercial premiums is expected to shift from 80%/20% today to 40%/60% by 2040.

The smart mobility sector will require more agile products — pay-as-you-drive (PAYD) or distance-based coverage policies — embedded into the connected mobility ecosystem. Lynk & Co, a month-to-month car membership and sharing platform, partnered with Allianz at the beginning of 2022 to create such products. Allianz pan-European motor insurance and personal accident coverage are now embedded into different membership plans, generating a steady stream of new customers for Allianz at a low cost.

Streamlined claims management

Insurance telematics allows claims managers to conduct remote vehicle diagnostics as part of the pre-claims assessment.

Machine learning algorithms can rapidly collect and process vehicle sensor and onboard system data to assess the accident type or report on recent repairs. Automatically aggregating such insights reduces existing frictions in auto claims reporting; plus, it can dramatically speed up settlements.

The best part is that mobility industry players are open to sharing available data as part of their monetization strategy.

In 2020, BMW and Toyota agreed to provide Swiss Re with ADAS vehicle data for risk-scoring purposes. This partnership has enabled SwissRe to offer better rates to owners of ADAS-equipped BMW and Toyota vehicles thanks to the proven safety impact of advanced driver assistance systems. The same data can also be used for investigating claims and reconstructing potential claims.

In fact, that’s exactly what OCTO Telematics is already doing. The innovative fleet telematics provider and data platform has designed a fully digital crash and claims management product. Using a combination of real-time data and historical insights, AI-powered OCTO software can reconstruct and validate a recent crash event. Insurers can get an unbiased scoop on the event’s context and dynamics to correctly assess the damage, attribute responsibility, and automatically process the claim at warp speed. To date, OCTO Telematics has analyzed over 493,000 claims and insurance events and alleges to hold the largest database of vehicle telematics data globally.

Aftermarket insurance services and warranties

Insurers can also add value to automotive consumers by capturing another link in the customer-insurer relationship chain — aftermarket insurance and warranties.

Replacing parts, performing post-collision body repairs, improving the vehicle’s appearance, tuning the performance — vehicle owners have an endless list of tasks on their agenda. Getting regular vehicle inspections and performing regular maintenance (in authorized locations) is crucial for reducing the risks of an insurance event. By taking over the entire repair process, coverage providers can not only reduce risks but also gain more comprehensive vehicle data.

Fresh car diagnostics data and accurate information on current vehicle performance can help with designing more competitively priced policies for older (but gently used) vehicle models. Likewise, locking customers into using authorized aftermarket service providers can minimize the risks of poor repairs and fraud. Aftermarket auto insurance is particularly appealing to EV owners, as battery replacement costs can go north of $16,000.

Stolen vehicle recovery and security-related telematics applications are another area of interest for insurers. Such data can help prevent events for coverage, especially when insuring commercial carsharing fleets.

Zurich Insurance recently released a competitive EV package featuring a host of repair, replacement, and anti-theft guarantees to complement OEM warranties. In the UK, the company also presented a like-for-like electric vehicle replacement offer for SME customers who use one of its approved repair networks.

Advances in EV battery analytics will soon enable insurers to capture even more data about performance across vehicle lifespans and design more competitive policies.

Preventive insurance offerings

Preventive coverage products are the next evolutionary step for the industry. With advances in big data analytics and machine learning, insurers can soon switch from predicting to preventing risks.

In practice, this idea is simpler than it sounds. For decades, insurers have been rewarding customers for good behavior — be it having zero accidents or installing an anti-theft system. Digital technologies, paired with connectivity, will allow insurers to identify and reward consumers for more granular behaviors, ranging from not speeding to taking the vehicle in for regular diagnostic checks with sanctioned providers.

Mitsubishi Motors recently partnered with LexisNexis Telematics, a platform offering aggregated access to vehicle data to insurers for risk management, claims management, and claims settlement. Thanks to this deal, Mitsubishi vehicle owners can get lower motor insurance premiums as early as when they get an initial quote and then earn further discounts based on their driving behavior.

Using a combination of embedded and video telematics, insurers soon will be able to analyze even more factors affecting drivers’ behavior such as:

- Common driving patterns

- Fatigue/drowsiness

- Driver distraction

- Traffic and road conditions

- Heart rate and anxiety levels (indicating stress or fear)

Then they can employ the above for personalized, on-demand premium calculations. Such systems are already feasible and are seen as a solution to minimizing road rage and aggressive driving.

GM and Tesla are both looking to bring such behavior-driven auto insurance to the market in the coming year or two. Tesla first started testing the program in Texas at the end of 2021 and expanded to several more states in 2022. GM-owned OnStar Insurance requested regulatory approval for behavior-based coverage in three states in Q1 2022, but there have been no further updates.

Both companies are eying the sector, with GM hoping to generate $6 billion in annual insurance revenue by 2030.

Embedded insurance distribution

Ultimately, the pursuit of telematics data by insurers can set them on a new and profitable path of embedded distribution.

Instead of merely sampling vehicle data from OEMs, insurers can choose to become a core part of automakers’ emerging platform businesses.

Embedded insurance is a technology-driven product distribution model, aimed at offering affordable, relevant, and customized policies to customers when they need them most.

For motor insurance, embedded translates into offering policies inside OEM-driven apps, at dealerships, on digital customer experience platforms, and within upcoming vehicle operating systems.

And that’s a value proposition many automotive companies are ready to accept as they seek further differentiation in the customer experience, paired with extra revenue streams:

Good customer experience = salience. This equals more customers for insurance carriers. Salience is how easily a company, in this case, an OEM selling a car, can make an additional sale, in this case, a policy. At the point of sale, salience is at an all-time high. Customers are not only in a “buying mood,” but they are also likely to value protecting their new purchase.

Tesla, GM, Ford, Toyota, and countless other OEMs are already embedding F&I products from their insurance partners straight into their customer journey flows.

Soon, the motor insurance experience may become fully invisible for customers as tailored products will be included in the vehicle purchase by default, with premiums dynamically updated based on driver behavior.

For insurers, this state of integration is a relatively passive and affordable path for customer acquisition and solid guarantees of customer retention.

Is telematics insurance worth it?

The short answer is yes. Combining telematics and insurance offers many benefits for everyone involved, including insurers. Here are the key advantages:

Better pricing

Auto telematics takes risk assessment in insurance to the next level, helping insurers avoid underpricing high-risk drivers and overpricing low-risk drivers. Plus, telematics in insurance allows providers to continiously monitor risk levels and adjust premiums as they change.

Enhanced claim management

Telematics data provides detailed information on the circumstances of an accident, helping insurers speed up claims processing. It also adds an additional layer of protection against insurance fraud by providing unbiased evidence for insurance cases.

Stronger customer relationships

Telematics allows insurers to personalize insurance products to the specific needs of individual drivers, thus enhancing customer satisfaction and loyalty. Additionally, telematics car insurance creates a foundation for value-added services, such as maintenance alerts and stolen vehicle recovery, which can differentiate an insurer from competitors and help it attract more customers.

Operational efficiency

Telematics insurance also boosts efficiency in core insurance operations, including underwriting, which results in lower administrative costs. Additionally, it helps insurers make more informed and faster decisions regarding individual cases and overall business strategies, such as policy design, marketing, and customer service.

The biggest disadvantage of telematics for insurance is the high implementation cost. Developing telematics software systems and setting up telematics infrastructure in vehicles require significant investments. However, balancing the advantages and disadvantages of telematics presents a great opportunity for the growth of insurance and automotive businesses.

Driving the telematics opportunity home

Insurers and automotive companies have been operating side by side for ages. But until recently, there have been few truly close partnerships in deep tissue connectivity. The transition to platform-based business models and rising levels of connectivity are about to change that.

With OEMs looking to grow beyond their core business, many are sizing up the profitable turf. Some insurers may feel threatened, but smarter ones are truly excited about joining the OEM ecosystem to harness available data or become fully embedded partners.

Some insurers may feel threatened, but smarter ones are truly excited about joining the OEM ecosystem to harness available data or become fully embedded partners.

Don’t just watch others drive this opportunity home. Add telematics to your product development roadmap! Intellias is a technology partner to global OEMs and Fortune 500 F&I companies. Contact us to discuss how you can benefit from our cross-sectoral experience.