The insurance sector has a rich legacy. One of the first insurance companies was founded at the end of the 17th century. Present-day AVIVA still traces its origins to it.

Over the centuries, risk management has become more precise, claims management faster, and premiums more competitive.

But one element has remained constant — heavy reliance on agents for insurance distribution.

Today, the US insurance sector employs over 440,000 advisors. China has some 8 million agents in the life insurance sector alone, while the EU market has over 815,000 intermediaries, including brokers, agents, bancassurance, and others.

On the surface, that’s a strong distribution network driving the industry forward.

But in practice, distribution is often the weakest link in the insurance value chain.

![[whitepaperbox link="https://intellias.com/ebooks/ai-insurtech-embrace-the-tech-revolutionizing-insurance/" imageid="74480" title="AI Insurtech - Embrace the Tech Revolutionizing Insurance" ]Everything You Need to Know about the Insurance Industry and Artificial Intelligence[/whitepaperbox]](https://d3twecw9qvot3u.cloudfront.net/wp-content/uploads/2024/05/AI-Insurtech-cover-1.png)

Why the insurance sector needs digital distribution channels

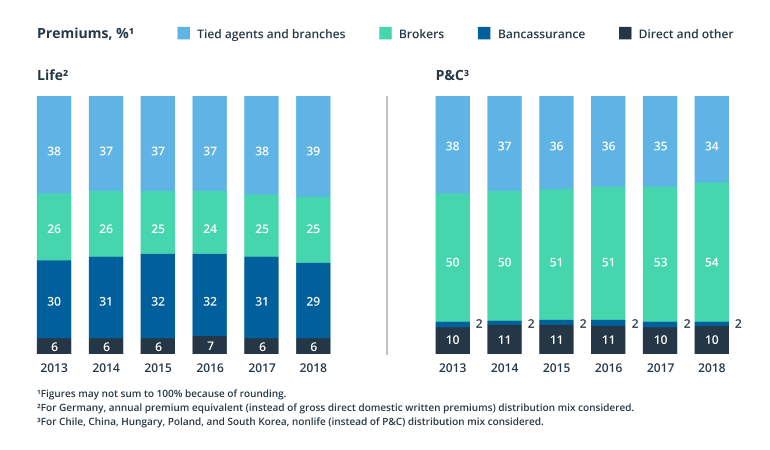

With agents and branches being the focal point for distribution, it’s not surprising that in-person sales dominate in the insurance sector.

Source: McKinsey — 2020 Global Insurance Pools Statistics and Trends: Distribution

Then the rocky 2020 came and things took a U-turn. A survey of US life insurance agents found that in January 2020, 90% of sales conversations and 70% of ongoing client conversations happened in person.

By May 2020, both of these figures had dropped to less than 5%.

Similar dynamics took place in other geographic markets and across insurance products. Though the numbers have somewhat improved in 2022, the pandemic revealed two major issues in the insurance sector:

- Low salesforce efficiency

- Overlooked changes in customer behavior

Operating a large network of agents, branches, brokers, and partners means little control over customer service quality and sales efficiency. Most insurers have sales quotas per agent and/or branch. But few can estimate the volume of missed sales opportunities.

Shopping for insurance is a chore for most people — and even more so for younger connected consumers. That’s literally what some of them tell us on Twitter:

Source: Twitter

The sentiment is even less peachy when it comes to going to the branch, where the wait times can be long, the agents mildly engaged, and the insurance software way too slow for the 21st century.

Between 2013 and 2017, the average insurance company lost $27 million in potential profit per year due to a series of factors, including low workforce productivity. Labor productivity is painstakingly low because most business processes are largely manual and paper-based.

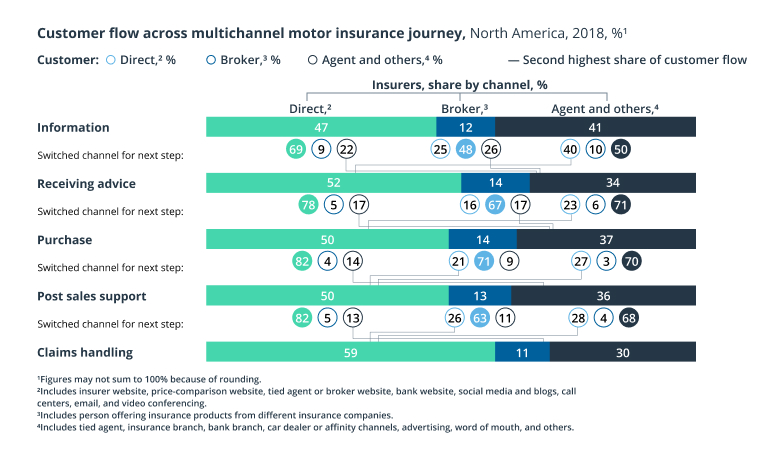

Many insurers have also overlooked wider changes in consumer purchasing behaviors. Even prior to the pandemic, a number of steps on the insurance customer journey happened online — and resulted in direct engagement.

Source: McKinsey — 2020 Global Insurance Pools Statistics and Trends: Distribution

An even larger segment of customer journeys is set to permanently migrate online onward. A 2022 SwissRe consumer survey notes that across all markets, 48% of consumers purchased policies via an insurer’s app or website, while 45% did so with an agent or broker. Another 27% favored non-traditional distributors, including InsurTech companies and adjacent businesses.

A 2022 J.D. Power study also found that consumers are happier when digital purchase options are available but get frustrated if the online buying experience isn’t great:

The average satisfaction score among the top-performing 25% of respondents using a mobile app is 885—significantly higher than any other channel. However, satisfaction with the bottom 25% of respondents using a mobile app falls 358 points to 527.

Pre-pandemic, insurers failed to act on these shifts in consumer behavior. This gave growth momentum for InsurTech players — specifically, companies specializing in digital insurance product distribution.

In 2021, InsurTechs focused on distribution and accounted for nearly 55% of all deal activity, a 7% increase from the prior quarter.

New players tend to focus on tech-enabled distribution to reduce their dependence on agents. Or build out attractive digital insurance shopping platforms and pool profits through commission. Both owning and reselling insurance products from others is profitable, as recent valuations prove:

- Extend, an embedded product warranty platform, has a $1.6 billion valuation.

- Ethos Life, an online life insurance platform, has a $2.7 billion valuation.

- Policybazaar, an Indian insurance marketplace, had a $6 billion valuation pre-IPO.

- The Zebra, a US online insurance marketplace, got a $1 billion valuation in 2021.

Despite different value propositions and operating models, these InsurTech companies capitalize on the same weak element — distribution.

Embedded as a new insurance distribution channel

Distribution is clearly a problem for incumbent insurers.

Embedded insurance has emerged as a solution to it.

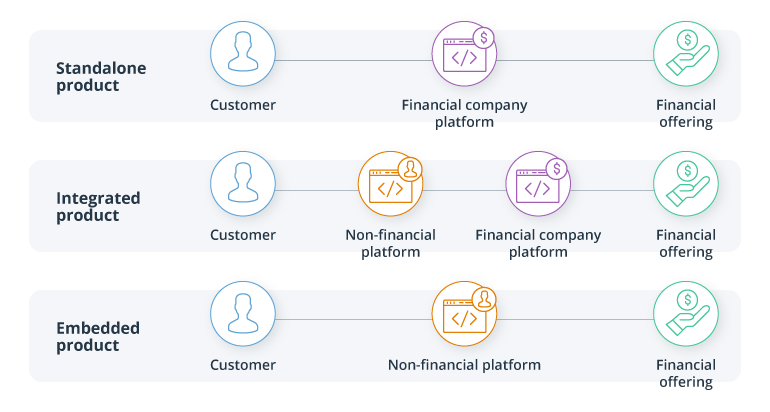

What is embedded insurance?

Embedded insurance is a technology-driven distribution model aimed at offering affordable, relevant, and customized insurance to customers when they need it most.

The term (and the tech behind it) may sound new, but the underlying concept is familiar to most insurers. Insurance policy upsells with rental cars, plane tickets, and new car purchases have been around for decades.

Embedded is a change in how you enable other companies — from ecommerce platforms to logistics companies — to upsell your policies to their consumers at a relevant time.

Similar to embedded financial services, embedded insurance distribution may be the driver the industry needs to offset rising customer acquisition costs and fend off digital disruptors.

Embedded insurance is an opportunity to get closer to customers at a lower cost

Making an insurance sale happen is expensive. Approximately 50% of total industry costs stay at the supply side — in other words, they go into luring consumers to buy insurance products they find boring, complex, or unnecessary.

The average customer acquisition cost (CAC) for traditional insurance looms at $487 to $900 per new account. Yes, a huge agent- and branch-dependent network costs a lot to maintain.

Direct insurers, relying less on in-person selling, achieve up to 70% lower operating cost ratios compared to the average multichannel insurer.

Embedded insurance, in turn, lets you combine direct selling with economies of scale. That enables you to add more direct distribution channels at minimum cost. Once you’ve developed an API-driven insurance product (or several), you can pitch it to an endless number of ecosystem partners, who will offer it to their audiences without any added costs.

In other words, insurers can create profitable ecosystems of partners for systematically generating value. That’s the allure of the $56 billion (and rapidly growing) global embedded insurance market.

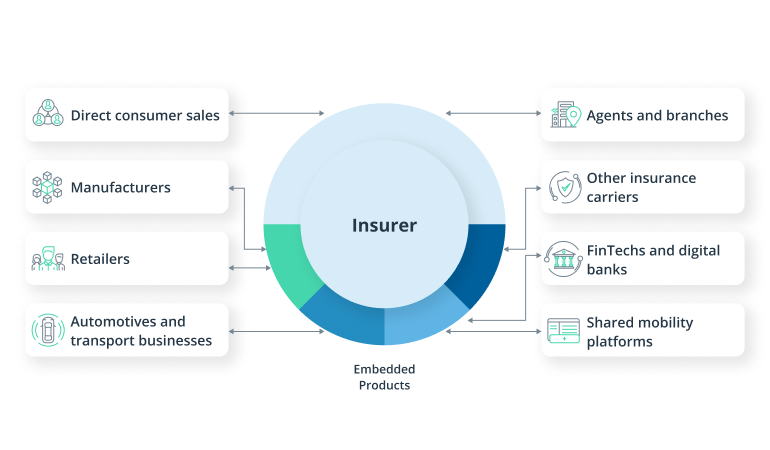

How embedded insurance ecosystems create value for participants

Bancassurance isn’t the only profitable partner for modern-day insurers. Manufacturers, brands, online marketplaces, telecoms, and FinTechs can also become part of your distribution ecosystem.

The beauty of embedded is that your partners don’t have to worry about industry regulations and compliance. That’s still on you.

Back-office operations like policy generation, underwriting, and management still take place within your system. Your partner merely rents your product and organically embeds it into their sales flow for consumers to consider and purchase.

That’s an attractive deal for both parties. Each earns a profit, gets extra customer data, and improves customer satisfaction.

Source: Penny.io — Embedded insurance index – part I

Here’s how embedded insurance can drive systemic value through partnerships.

Improved customer knowledge through owned and partner data

Data drives decisions in insurance. Policy costs and corporate bottom lines strongly depend on your ability to make precise estimates.

Embedded insurance products let you combine proprietary big data with extra insights obtained from partners. Consumers, in turn, are more than willing to chip in. According to Accenture, 69% of insurance consumers would share data about their health or driving habits in exchange for lower policy prices.

Unconstrained access to data (and the ability to operationalize it using the best risk assessment methods) can also lead to wider company transformations.

Take it from Ant Group — China’s financial super app that sells insurance products, among other things. The insurance arm emerged in 2017 as a distribution channel. Ant provided insurance partners with unbeatable access to consumer lifestyle data — from frequent purchases to favorite take-away dishes. In consultation with partners, the platform developed over 2,000 customized, affordable, and flexible non-life insurance offerings and actively marketed them to users. By mid-2020, Ant Group’s insurance platform serviced over 570 million customers, bringing in a 12-month revenue of CNY 52 billion.

Distribution channel partners can help insurers develop better visibility into customer needs — and customize policies accordingly.

Point-of-sale and usage-based insurance products

For most consumers, insurance purchases are need-driven: new car, new home, new family member. Few people proactively shop for insurance deals (because no one has the time to endure endless meetings with agents or brokers).

Embedded insurance lets you meet people at the point where their need emerges — at the point of sale (POS). Research by PYMNTS shows that 58% of consumers are more likely to buy retail products or spend more with merchants if insurance is offered at the point of sale.

For merchants, this presents an opportunity to increase sales and improve customer relationships. For savvy insurers, it’s profitable new turf to explore by creating embedded insurance offers based on consumer behaviors on retail platforms or product usage patterns. Cowboy e-bike, for example, leverages bike sensors, GPS coordinates, and remote diagnostics as part of its embedded insurance offering. By supplying insurers with rich insights, they manage to negotiate better premiums for their customers without expanding the risk radar for partners.

Usage-based insurance (UBI) products are another profitable growth avenue, already estimated to be worth $34.53 billion as of 2020. Pay-as-you-drive insurance products, in particular, are expected to see strong growth momentum as shared mobility ecosystems grow larger. Other promising use cases include personal insurance coverage for gig workers, flexible healthcare insurance for temporary workers, product warranties for subscription-based products, and various travel insurance packages. Zizoo, a boat rental company, recently embedded a digital charter deposit and a charter cancellation insurance for consumers, which helped the company diversify its revenue and improve the customer experience.

Data-driven POS and UBI products can help insurers acquire new clients en masse at a low cost without incurring extra risks.

Right-timed insurance offers tailored to customer journeys

Upsells and cross-sells are two familiar mechanisms for insurers. An embedded mechanism paired with data analytics helps insurers make the right pitches at the optimal time. As a result, insurers enjoy higher conversion rates and higher customer lifetime value through better retention.

Switching rates for some insurance products stand at double digits among European consumers.

Source: EIOPA — 2021 Consumer Trends Report

Suboptimal pricing and changes in personal circumstances are the two prime reasons for switching companies. Both issues can be addressed with personalized cross-sells. Provide customers with self-help tools to compare different standard packages and an opportunity to request custom offers. For example, Halifax has partnered with Trov to launch a flexible renters’ insurance product distributed as an application. Consumers need to answer just six questions (instead of 38 earlier) to receive a quote in 22 seconds. Renters can combine customizable monthly subscription plans with on-demand anywhere insurance for individual items (such as personal technology devices) and receive their policy with zero agent interactions. Claims management is fully digital too.

Apart from making insurance products flexible, you can also trigger the upsell at different stages of the customer journey (or even post-purchase). Remember: the power of the ecosystem is in data exchanges. Leverage new consumer intelligence to design better insurance offers. For instance, the online real estate platform ImmoScout24 noticed that up to 65% of landlords faced tenant payment issues. To alleviate the issue, the platform integrated an embedded insurance product for landlords. In several clicks, users can buy a policy to cover a loss of rental income in the early stages of a tenancy agreement.

Finally, if you don’t have a suitable insurance product in your portfolio (just yet), you can embed another carrier’s product into your sales flow. In fact, this is the route leading insurers choose to achieve operational resilience and sustainable innovation.

Customer experience reimagined

Ultimately, embedded insurance can bridge the gap between consumers’ expectations and preferences and insurers’ ability to meet them.

A 2021 IBM report found that 64% of consumers want their providers to understand them well. Yet only 60% of companies claim to have a solid CX strategy. This lack of understanding leads to poor trust, low satisfaction, frequent switching, and downright disengagement — all leading to high customer acquisition and retention costs.

By building wider product distribution ecosystems, insurers can address these issues by:

- Reducing policy purchase friction with convenient digital interfaces

- Pricing based on personalized risk assessments

- Offering competitive premiums and incentives as part of prevention activities (e.g. regular healthcare checkups or low workplace accident risks)

- Presenting timely value-added upsells and cross-sells presented at the point of need

- Offering innovative insurance products with coverage for shared, subscription-based, or leased items

By designing an experience where consumers can select the optimal coverage and pay for it instantly (or regularly), carriers also get to improve their cash flow and accumulate extra reserves for debt servicing and further innovation.

Partnership-driven distribution is the path forward

Embedded distribution acts as the equivalent of last-mile delivery within the insurance value chain. It’s a faster, lower-cost, and more scalable distribution model than agent- and branch-based distribution. But more importantly, embedded distribution empowers insurers to switch from transaction-driven to value-driven customer relationships.

Using ecosystem partners’ data and distribution capabilities, insurers can create personalized experiences for end consumers — and support them at different stages of their life journey. By focusing on the CX, insurers can become trusted advisors (rather than a bothersome chore) for prospects and policyholders, which will lead to higher customer loyalty and lifetime value.

Contact Intellias to discuss your technical strategy for launching embedded insurance products.