Switching between apps and digital devices is as easy as breathing. Sometimes this continuity extends into the physical world as well.

One tap to book a shared car. Another to pay for it. If you are lucky, your vehicle is instantly ready for pickup.

…Or you get a reality check: no available cars in your area, heavy congestion, and exorbitant parking costs no one warned you about.

Is it possible to transfer the seamless digital experiences of mobility solutions into the physical realm?

Yes. That’s what smart mobility platforms intend to do.

What is smart mobility?

Smart mobility is an umbrella term for physical and IT infrastructure that enables better transportation experiences. It includes optimized public transit networks, carsharing, ride-hailing, micromobility, and intelligent transportation systems for freight and logistics.

Some also count in future mobility nodes such as urban aerial vehicles, logistics drones, and (semi)-autonomous vehicles into the growing ecosystem of smart mobility as a service (MaaS) solutions.

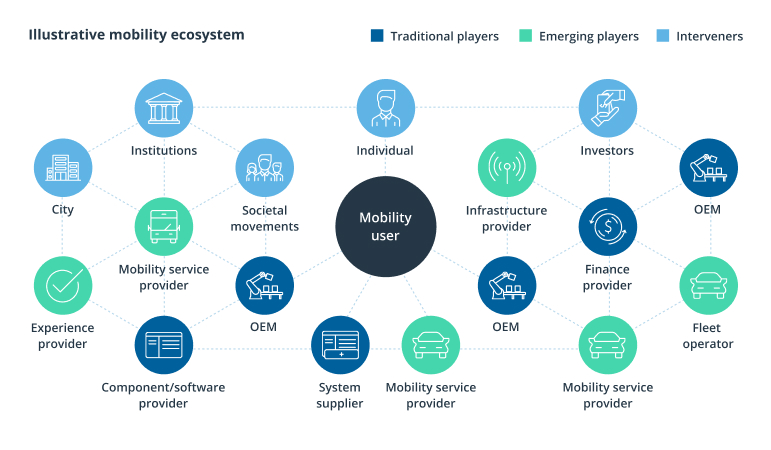

Mobility service-centric ecosystems

Source: McKinsey — Defining and seizing the mobility ecosystem opportunity

In other words, smart city mobility is a sprawling ecosystem of digital and physical assets:

- Physical elements: Connected private, shared, and commercial vehicles with robust data exchange capabilities; connected road infrastructure — smart traffic lights, connected CCTV cameras, connected toll gates, road sensors, etc.

- Digital elements: Cloud-based systems and supporting infrastructure for enabling connectivity and management of physical assets including MaaS apps, traffic management systems, and EV fleet management software.

In both cases, the focus of smart mobility solutions is connectivity.

Decoding the value of connectivity in smart mobility

Already, almost 50% of all new vehicles sold globally are connected, meaning they can communicate with other systems over networks (4G/5G, V2X, wireless, GPS) and/or via sensors (Bluetooth, NFC, RFID).

By 2030, 95% of newly sold vehicles will include communication services — and 45% will have intermediate or advanced levels of connectivity.

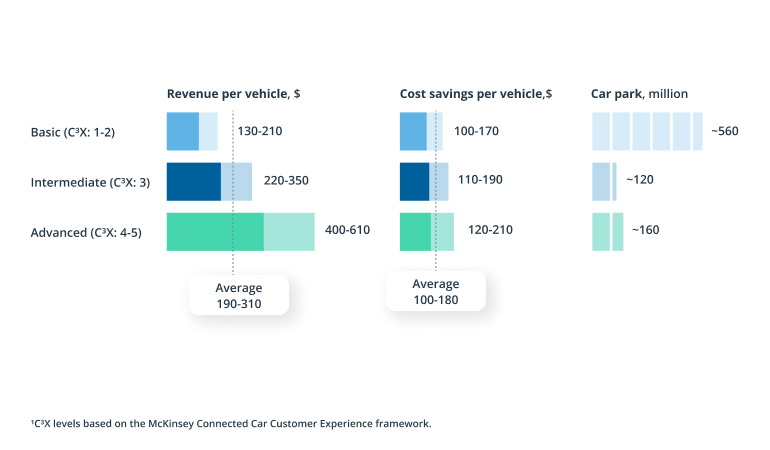

How use case potential differs by vehicle connectivity level

Source: McKinsey — Unlocking the full life-cycle value from connected-car data

What are the perks of packing so much technology into a car? Computing and connectivity technologies enable a daisy chain of controls for including physical road actors (drivers, bike riders, passengers, and pedestrians) into the wider ecosystem of connected mobility services.

This inclusion, in turn, leads to better:

- Mobility efficiency — The ability to exercise dynamic control over traffic management, public transit scheduling, parking management, and commercial delivery operations based on real-world information.

- Road safety — Real-time information exchanges between road actors and road infrastructure can alert drivers of nearby dangers and/or automatically prevent accidents.

- Revenue generation — On-board connectivity, paired with external services, opens a wide range of new revenue generation models, from in-car commerce to subscription-based fleet leasing options.

Emerging [connected mobility] revenue streams only amount to about $2 billion per year today, but they are expected to grow to $141 billion—a 7,500% increase—by 2035.

Let’s zoom in on road safety and transportation efficiency.

Road accidents remain a pressing issue globally. According to the World Health Organization (WHO):

- Most countries lose 3% of their gross domestic product to road traffic accidents.

- For children and young adults (aged 5 to 29), road traffic injuries are the leading cause of death.

- The risk of fatal crashes increases by 4% with every 1% increase in mean speed.

At the same time, traffic congestion further aggravates the collective cost of owning and using vehicles (something we aren’t ready to give up yet).

- Traffic on London’s roads costs the UK economy £5.1bn a year, or £1,211 per driver. Interestingly, over a third of car trips made are equivalent to 25 minutes of walking and two-thirds are equivalent to cycling 20 minutes or less. Yet Londoners still choose cars over alternatives.

- In the US, the total cost of congestion in the freight sector is as high as $74.1 billion annually, with urban areas accounting for $66.1 billion in costs. In 2022, freight traffic volumes have increased significantly (along with fuel prices), which will further hike operating costs.

- European transport costs locals over €1 trillion a year through air pollution, carbon emissions, congestion, accidents, and other external costs. Mind that Europe is a region with one of the most developed public transport systems and a strong commitment to transport sector de-carbonization.

Across the board, underlying inefficiencies continue to pervade commercial and urban mobility.

Why can’t we solve these issues when there are already viable technological solutions?

The answer isn’t simple, but it has a lot to do with human habits and the industry’s current approaches to technology adoption.

Why smart mobility is a collective task (and a collective gain)

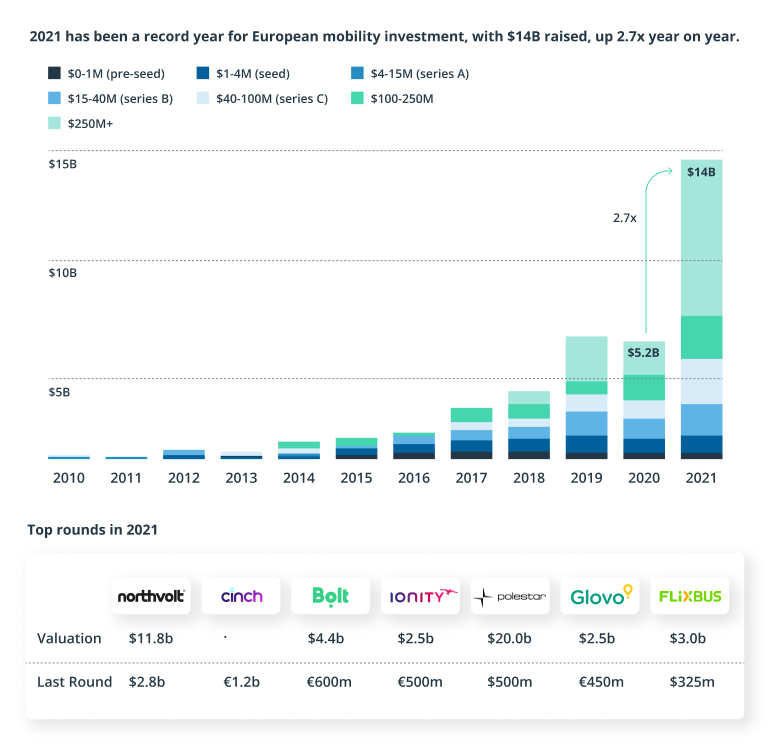

A cursory scan of the transportation sector reveals a booming ecosystem of players.

In one corner, we have promising connected vehicle and mobility as a service startups with growing investor support in almost every region.

Source: Dealroom — The State of European Mobility in 2021

In the other corner are OEM-led smart mobility platforms such as ShareNow (by Mercedes-Benz), Volkswagen-owned MOIA, and Kinto mobility services from Toyota.

Separately, automotive companies are exploring alternative connected mobility solutions to diversify revenue beyond direct car sales. Porsche runs a flexible vehicle subscription service in the USA. Mercedes-Benz offers a telematics-based InScore insurance policy to users. Ford just signed a five-year deal with Stripe to expand its scope of in-car commerce services.

The global transportation management systems market stands as another pillar of smart mobility. It’s already worth $96 billion and is set to hit $389 billion by 2030. Within it, you have multiple SaaS software providers as well as companies specializing in custom transportation management system development.

Finally, we have connected road infrastructure players working on everything from real-time traffic detection and analysis to parking management and urban transportation planning solutions together with local governments. Without physical links, the big promise of connected vehicles and smart mobility solutions will fail to materialize.

In between are many more market players, specializing in one or another element of mobility services — from electric mobility and mapping services to urban aerial mobility and autonomous commercial fleets.

So why does smart mobility remain (mostly) at a conceptual stage when so many players are operating in the field?

Because like the blind man, mobility players are more focused on figuring out their part of the elephant rather than coming up with a joint vision for the entire market.

Smart mobility companies mostly focus on standalone solutions, but more value can be generated cumulatively through ecosystems.

To become smart, mobility providers have to think in terms of continuous platform offerings, where different players chip in to deliver convenient, safe, entertaining experiences for road users.

The progressive creation of connected mobility platforms will also change people’s on-the-road behaviors and transportation node preferences.

Humans are social creatures — and we are inclined to do what others are doing. Scientists have found that traffic rule violations are highly contextual and depend on the time of day, road situation, and other road user behavior. However, drivers’ behavior can be proactively course-corrected with situational road controls. For example, if the road is empty at 5 am, there’s no need for a long red light, resulting either in unnecessary congestion or collective red light running.

Likewise, another group of researchers found that when everyone wants to minimize their commute time and cost, the result is the worst-case scenario where the average commuting time is maximized. In other words, if residents are inclined to think that going by car is the fastest way to get places, everyone will choose to drive — and the commute time will become longer as more cars hit the road. If people perceive that going by public transport will be faster, they’ll leave the car behind.

Both of these behaviors can be moderated with technologies in a way that helps all ecosystem players generate extra revenue.

Smart mobility ecosystem: 4 elements to explore independently and with partners

For smart mobility to become a reality, transportation industry players must opt for collaboration over competition — and do so in sync with government agencies.

That’s no small task, requiring both operational and technology planning.

We mapped four elements mobility leaders must get right to grow in this decade.

Cloud-centric thinking and platform-based operations

The cloud acts as a force multiplier for emerging technologies — big data analytics, AI/ML, IoT, and location-based services, among others.

You can’t establish connectivity with other players without setting up a robust cloud architecture to aggregate and process data from:

- Hardware elements such as connected vehicles (cars, trucks, micro-mobility nodes) and road infrastructure (edge devices, road sensors, CCTV cameras)

- Software modules via API integrations — proprietary and third-party — with low latency and strong security

A number of purpose-built smart mobility solutions and services are available such as:

Such cloud mobility platforms offer premade components for

- Standardized data exchanges

- API programming

- IoT connectivity

- Scalable cloud architecture

Generally, you should design smart mobility systems with modularity in mind. Structure different sub-elements as microservices. Then leverage APIs (internal and external) to hook more partners into your platform.

The platform as a business model helps transportation companies maximize market reach by offering a mix of interconnected products, services, and solutions, built in-house and delivered via third parties.

Data governance

Platforms enable wider data exchanges. By leveraging third-party data, participating companies can offer service continuity and integrity in the customer experience (CX).

Think of the above as an upsell. Let’s say your local coffee store partners with the bakery next door and now offers mouthwatering croissants. They’ve also upgraded their Wi-Fi thanks to a new telecom partnership so that your weekly work session is even more delightful.

In the transportation sector, data exchanges and embedded third-party services can drive an even more agreeable customer experience.

Transportation companies can use data to:

- Launch new services

- Improve pricing

- Offer safety add-ons

- Provide after-market services

- Offer upsell/cross-sell deals

Cumulatively, industry data from the automotive, mobility, and public transportation sectors can improve urban planning, government services, and, ultimately, the attractiveness of municipalities.

But to make that happen, you need a strong data governance process.

Your ability to locate, securely process, and operationalize data from various sources — public and partner APIs, connected road infrastructure, government agencies — will determine your product’s success rate.

A truly connected mobility solution needs to have secure, low-latency, real-time data processing capabilities. With those in place, you can create instant consumer experiences such as convenient multi-modal travel journey planning, cost-effective dispatch management schedules, and seamless public transit management.

Core revenue streams

Smart mobility systems unite different players — automotive companies, logistics companies, fleet managers, public transit authorities, and mobility startups offering on-demand services.

Each already has a business revenue stream, such as B2B/B2C vehicle sales or transit ticketing, that can be augmented by partners.

For example, automotive companies can expand into:

- Leasing / renting vehicles to carsharing startups

- Selling e-vehicles to public transport authorities

- Offering demand-based vehicle subscriptions to logistics companies during busy seasons

In fact, that’s what leaders already do. In 2018, Toyota invested in the SEA mobility startup Grab. Since then, they’ve been advancing the scope of their partnership. Apart from cash injections, Toyota set up competitive financing and trade-in deals for Grab drivers, while Grab profits from Toyota’s telematics technology.

Autofleet — a startup offering an AI-driven vehicle as a service supply platform — counts Ford and Fujitsu Limited among partners who plan to use its technology for launching on-demand mobility and logistics solutions.

Distribusion, in turn, has built its entire business model around connecting ground transportation carriers with retail partners to help them improve distribution. Covering 70+ countries, Distribusion offers access to a vast network of mobility platforms, online travel agents, and metasearch websites via one API. Since 2020, the company has achieved 10X passenger volume growth and plans to service 100 million passengers per year by 2024.

New revenue streams

Beyond strengthening core revenue streams, smart mobility ecosystems open new vectors for product development.

By combining scalable cloud-based operations with APIs, transportation players can pursue data monetization, improve pricing, and expand into adjacent markets faster and at a lower cost.

Here are five revenue opportunities worth looking into.

Mobility as a service (MaaS) offerings

The MaaS market includes multimodal transportation players, offering on-demand access to mobility services. It features a growing number of ride-hailing, asset-sharing, and public transit companies operating in every market.

The global MaaS market generated a $12.8 billion revenue in 2021 – and is expected to grow 4X to $51.9 billion by 2030.

As urban populations increase, MaaS providers will help public transport authorities better navigate passenger flows. Already, the daily commuting category accounts for the largest market share — and it’s expected to increase further as people prioritize carsharing over vehicle ownership.

Decarbonization plans put in place by global governments would also accelerate the development of the e-mobility sector both for public and commercial transportation.

Joint smart mobility programs aimed at managing congestion and pollution levels are already happening. Transport for Greater Manchester (TfGM) has recently partnered with SkedGo — a local MaaS player — to offer a better multimodal transit experience. TfGM incorporated SkedGo’s journey planner into its website, letting users build routes, compare costs, and see CO2 outputs for their journey. That’s a win-win partnership because SkedGo can organically grow its ridership while TfGM gets better visibility into residents’ journeys and exercises better management of public transport.

Parking management solutions

Parking is another pressing problem that can be solved through better collaboration between cities and commercial players. By tapping into smart mobility ecosystems, urban planners can gain insights about:

- Carsharing/car rental usage patterns

- Commercial fleet parking needs

- Common last-mile routes requiring curbside use

- Overall traffic flows and current demand for parking

These insights can be used to implement better zoning — adding/removing parking spaces, clearing the curb, regulating street parking hours, or implementing dynamic parking prices.

Industry partners, in turn, can act as enablers and supply:

- Modern parking management software with parking guidance, online reservations, and connected payments

- Dedicated parking spaces and competitive rates for logistics companies

- Better parking apps for drivers that are integrated with navigation apps, journey planners, and urban mobility apps

Infotainment and connected car services

The concept of smart mobility also extends to connected cars. By 2030, 50% of vehicle value will come from electronics and embedded software — the connectivity components for new revenue models such as:

- In-car commerce — Seamless product/service purchases straight from the car dashboard

- Zero-click M2M payments — Automated payments between a vehicle and connected infrastructure such as toll gates, fuel pumps, and charging stations

- Premium onboard media — Natively accessible from the dashboard and easily distributed to all passenger screens or devices

- Aftermarket and predictive maintenance services triggered by usage patterns and driving behaviors

The above revenue models work best for OEMs. But public transport managers and shared mobility companies can also monetize their audiences.

For example, public transit companies can offer personalized combined fares with local attractions to urban travel app users (based on demographics and behavioral data). Or they can run location-based advertising campaigns with local businesses, such as by highlighting a sponsored restaurant to the user.

EV charging

The demand for EV charging infrastructure will only increase in the coming years. Yet private companies keep passing the buck to governments — and vice versa.

Given the costs and complexities of developing EV infrastructure, cross-industry collaborations present the next best course of action.

OEMs, mobility companies, and other businesses (such as retail locations) could create competitive charging infrastructure cost-sharing agreements. For instance, Volkswagen partnered with Schwarz Group (featuring retailers like Lidl and Kaufland) to co-fund EV charging infrastructure. In return, VW gets exclusive overnight charging rights for its WeShare fleet.

Collectively, mobility and EV infrastructure companies can negotiate better prices with energy market players — and perhaps even co-fund green energy infrastructure (as Tesla does). Or they can develop even more intricate partnership networks as Swobbee, a battery as a service startup, is attempting to do. Swobbee closely collaborates with logistics companies (DPD, Hermes) to supply charged batteries for micro-mobility nodes and to provide smart mobility services to asset sharing startups. At the same time, they are backed by EIT InnoEnergy, a major accelerator of sustainable energy in Europe, which likely allows them to secure competitive energy rates.

Road intelligence

To be safe and effective, all smart mobility services require real-time traffic information, HD mapping data, and low-latency navigation. To get it, most rely on established players like TomTom, Waze, or Google Maps.

By joining ecosystems, individual players can unlock data generated and exchanged by partners. Then they can use it to create better mobility experiences:

- Urban planners and cities can supply GIS data, planned road construction data, and parking data.

- Mobility and asset sharing players can provide data on asset use, rental frequency, common routes, occupation rates, etc.

- Automotive companies can supply vehicle telematics data, emissions data, and analytics on common traffic flows.

- Connected road infrastructure providers can provide real-time congestion and accident rates, traffic flows, traffic patterns, etc.

- Public transport authorities hold valuable ticketing data, passenger volumes, and travel flow insights.

By fusing all of these data sources, every player in the ecosystem can gain a 360-degree view of transportation flows, frequencies, and shortcomings. Then they can translate this knowledge into a better travel experience for residents and lower network management costs for participants.

Final thoughts

In response to population growth, the transportation industry has pioneered new travel modalities to support farther, faster, and cheaper journeys.

But the proliferation of transportation nodes has come at the cost of a more disjointed travel experience. In urban areas, you have a tad too many transport nodes. In rural ones, a tad too few.

In the next chapter of growth, the transportation industry will have to rebalance these inefficiencies and join up on better terms so that passengers receive better commute experiences, authorities receive better road safety and traffic management, and smart mobility service providers establish sustainable growth models.

Intellias is a technology partner supporting transportation and mobility services providers on their growth journey. Contact us to discuss the perks and perils of mobility platform development.