The call to become an “Agile financial company” has been making the rounds since the early 2010s. But despite being nearly a decade in the making, there’s still a lot of mystical woo-woo around what it means to be Agile.

Many talk about Agile as a cultural practice. But a strong culture emerges out of shared best practices, which, in turn, are based on processes. In this post, we talk about how any incumbent bank can put the right Agile practices at its core.

What is Agile in the banking industry?

Agile is an operational strategy focused on breaking lofty, long-term, hierarchical processes into smaller increments for continuous execution. Originally conceptualized as an approach to software development, Agile has since made its mark across an array of operational processes, from marketing to procurement.

Agile is not a destination — it’s a path towards changing how your organization define roles, plans, accountability, and mechanisms for responding to market changes.

An Agile financial company, in turn, is an entity that has a strong but flexible process for determining which product features are due for production next, who will take the lead, and how a new project will be integrated with other operations.

Unlike traditional chain-of-command financial organizations, Agile financial players focus on solving targeted pain points on customers’ journeys with equally sized teams that are fully responsible for developing solutions for particular issues.

Key characteristics of Agile tech teams:

- Small and multidisciplinary

- Innovation-driven

- Bounded by specific projects

- Self-governing and accountable

- Aligned with overall business goals

Agile development in banking

Agile is also a methodology for setting up a software development lifecycle (SDLC) — the cadence for delivering new products to market.

Financial leaders are already in the know about Agile best practices in these contexts:

- Continuous delivery and continuous integration (CI/CD)

- Automated quality assurance (Agile QA)

- Scrum adoption and product backlog planning

- Infrastructure orchestration and optimization

- DevOps and DevSecOps adoption

The idea of the Agile SDLC is to break down the software delivery process into a series of predictable steps and feedback loops augmented by automation.

Such an approach allows for complex software products to be delivered incrementally.

Source: Scaled Agile — How SAFe empowers businesses to compete in today’s marketplace

FinTechs and digital-only banks are setting the trend for implementing Agile methodologies in the financial services industry.

- Starling Bank treats software as something that’s never finished and needs to constantly evolve. They keep iterating on what they’re doing while also being the only digital bank in the UK with a full banking license (and all the compliance burden that comes with it) since day one.

- Revolut scaled to five million users in under five years by maintaining lean practices despite an increasing headcount and by relying on rapid prototyping, the API economy, and rapid feedback loops to quickly deploy and test new products.

- Tencent is a proponent of feature-driven development (FDD), a strong product ownership culture, Scrum, automated testing, and continuous integration for speeding up release times.

What sets these Agile financial companies apart is that they have concurrent processes for defining the product vision and determining the execution:

- The product vision (WHAT) is defined collaboratively, based on grassroots feedback and a strategic vision from top management.

- The execution (HOW) is fully determined by multi-disciplinary teams who know the ins and outs of the technology infrastructure, customer demands, and corporate goals.

As a result, Agile organizations can pursue multiple growth vectors at once to scale the business in the right direction. They can experiment (fail and succeed) fast, embrace change, and take full responsibility for outcomes while retaining a strong connection with customers.

61% of CX leaders say their company has a clear view of which technology platforms they need to leverage in order to remain competitive and relevant to customers—compared to only 27% of their peers.

In 2021, however, Agile adoption in banking spilled well beyond the FinTech scene. From BBVA and Credit Swiss to JP Morgan and ING, international banks have turned to Agile as a solution for common bottlenecks — from scheduled end-of-the-month maintenance to bloated codebases and subpar IT architecture configurations.

The decision to embrace Agile in banking has borne positive results:

- Since 2014, BBVA has been working on transitioning 33,000 employees to a new Agile structure. The bank has established new cross-functional teams and departments, introduced a Single Development Agenda (SDA), and introduced baseline Agile technical best practices such as CI/CD, automated testing, and DevOps. Subsequently, the BBVA mobile banking app was recognized as best-in-class three years in a row. BBVA was also the first to launch a banking as service (BaaS) platform and fully capitalize on the open banking movement.

- ING Netherlands also started its Agile journey in 2014 as a response to growth in the demand for mobile banking services. As part of change management, the bank created 2,500 redesigned positions for newly minted Agile squads — cross-disciplinary teams of up to nine people who are focused on delivering and maintaining products and services serving one specific customer need. DevOps and cloud adoption were the focal points of the bank’s transformation. By focusing on improving underlying IT infrastructure and individual application infrastructure, ING managed to attain 24/7 availability.

Why Agile in banking remains an uphill battle

Despite progressive shifts and numerous success stories, many incumbent banks are still a step behind digital-native banks in terms of scaled Agile adoption.

As the earlier cases illustrate, Agile adoption in banking requires significant determination and cross-company organizational shifts. But while carrying out transformations, many banks run into common roadblocks:

- Lack of a common vision and strategy for Agile adoption

- Legacy technology portfolio and infrastructure

- Concerns regarding compliance and regulatory requirements

- Looming knowledge and collaboration gaps between departments

- Low levels of standardization for business processes

- Fragmented product and technology landscape due to various M&A activities

- Low to no automation adopted for IT processes

Over 85% of teams agree that lack of skills, legacy infrastructure, and dated delivery culture are the main blockers to adopting DevOps (a higher-level Agile practice).

The above issues have a common underlying cause: deep-rooted fragmentation and a low degree of individual accountability among teams, departments, and mid-management.

Legacy IT departments have little clue as to what customers need. Appointing product owners is hard because no manager fully understands the product lifecycle.

In that sense, Agile is a massive cultural shift that often requires radical transformations such as creating brand-new roles for everyone and asking people to re-apply for them (the way ING did).

But that doesn’t mean you should orchestrate a transformation at once in one fell swoop.

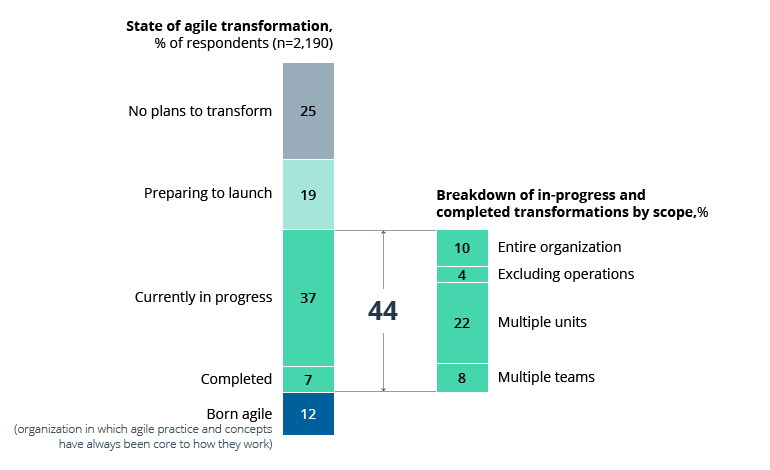

A 2021 survey by McKinsey found that most leaders start testing Agile on a team level. Then they scale to other units and departments. Interestingly, the financial sector is leading the way in Agile adoption.

Source: McKinsey — The impact of agility: How to shape your organization to compete

If you are Agile-curious and want to get into the action, start at a small scale and experiment with establishing several Agile software development teams. Then provide them with the decision-making power, resources, and support for stretching lean practices into other units and scaling them across all IT infrastructure.

Main Agile and lean principles in finance

Similar to DevOps in finance, Agile assumes people, process, and technology shifts.

In this sense, the baseline principles of Agile and lean are the same. But given the financial industry’s history, they’re given a particular spin:

- Sustainable modernization of core legacy banking systems

- Paced migration to a service-oriented architecture (SOA) and/or microservices

- Cross-functional teams and strong collaboration between business units

- Empowered teams taking over product ownership

- Continuous integration and continuous delivery (CI/CD) implementation

- Shift from future-proof 5+ year planning to short-term sprint planning

- Planned backlog aligned with market demands and current priorities

- Continuous testing (CT) throughout the software development lifecycle

- Infrastructure as code and process orchestration (DevOps)

- Faster change management and faster software delivery pace (weeks > months)

- Infusion of security best practices into the development process (DevSecOps)

- Continuous commitment to excellence and incremental improvements

All of these principles are meant to serve the ultimate goal of improving infrastructure efficiency to level up the customer experience (CX).

[As part of our Agile journey], infrastructure’s mission would have to change from building and operating mostly custom solutions to creating tools for developers to deploy standardized infrastructure on their own.

At the end of the day, customers will judge the efficiency of your processes through the prism of the product they interact with. Despite a 200% increase in mobile banking adoption, over a third of consumers are not happy with the in-app customer experience they get according to the Mobile Banking App report by PYMNTS. In the US, 37% of all respondents and 42% of baby boomers prefer web apps to mobile apps because they find online banking to be easier than mobile banking.

The frontend banking solutions you provide may be jam-packed with in-demand features, from AI for wealth management to personalized lending. But if these are backed by subpar technical infrastructure, all customers will experience high latency, constant glitches, and a desire to quit using the app altogether.

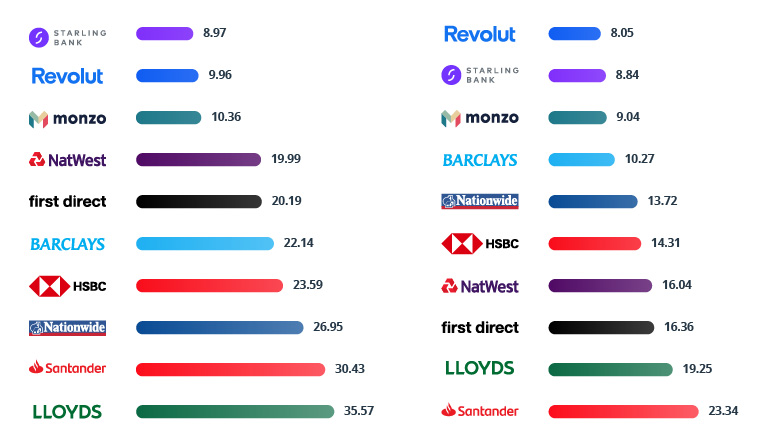

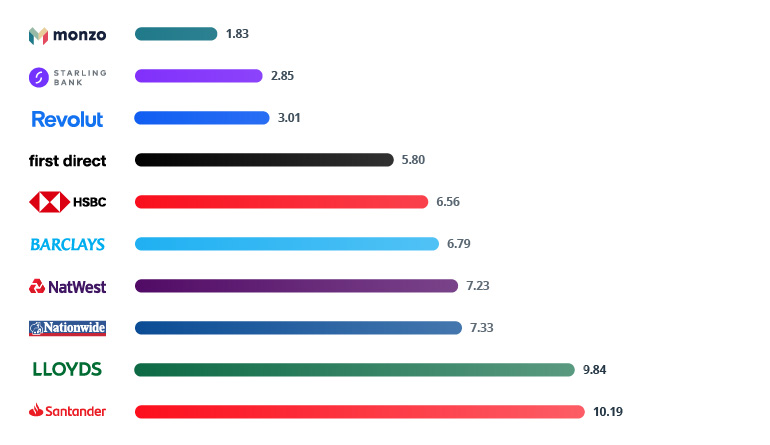

Peter Ramsay of Built for Mars conducted a UX case study comparing how UK banks stack up when it comes to providing open banking functionality. He evaluated the time needed to complete certain customer journeys in mobile accounts:

Seconds to complete payment authorization journey vs account information sharing journey

Source: Built for Mars — Open banking case study

The timing was drastically different for digital-only banks compared to their traditional peers. Did they require fewer steps to complete each flow? No.

But their mobile banking apps loaded two to five times faster than any app from an incumbent bank. Each loads in under five seconds — a speed standard for most software products.

Seconds to load app and redirect to auth screen

The takeaway: Without a properly optimized supporting infrastructure (and processes behind it), your bank will keep losing UX and CX points at every step of the customer journey.

By implementing Agile, you not only improve your operational practices and approaches to software development but also ensure that your IT infrastructure is right-sized for supporting delightful and high-performing applications.

How an Agile methodology in financial services pays off

For banks just entering the Agile race, there’s some good news: By committing today, you can get to the same performance levels as Agile-born companies.

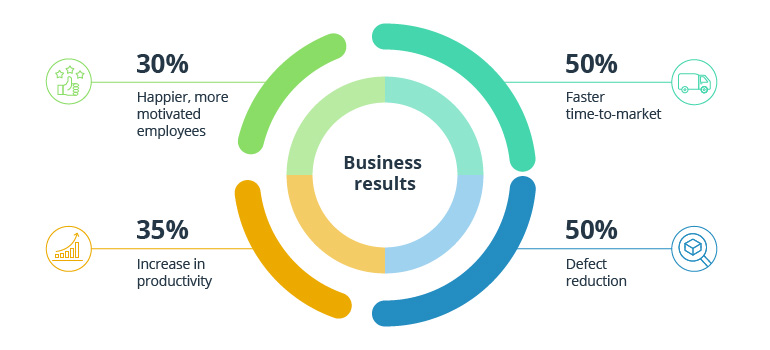

Highly successful agile transformations delivered around 30% gains in efficiency, customer satisfaction, employee engagement, and operational performance. Also, they made companies 5X-10X faster.

Here are even more benefits of going Agile in banking and the ROI of doing so:

- Improved customer intelligence. Successful Agile transformations lead to 30% increases in customer satisfaction.

- Faster time to market for new products. Standard Bank saw a 23x decrease in time to market for new software products after scaled Agile adoption.

- Operational cost savings. Businesses that adopt continuous testing, one of the Agile practices, have recorded up to $7 million in operating cost reductions over three years.

- Better software quality. One bank recorded a 50% reduction in the software defect/error rate after adopting Agile practices.

- Faster growth. Agile helps improve and scale digital channels and launch new customer offerings. A US bank attributed a 25% increase in revenue from digital channels to their shift to Agile.

- Higher team efficiency. The purpose of Agile is to get rid of red tape and eliminate low-value processes. Such targeted efforts can lead to up to 30% improvements in team efficiency.

To conclude

Consumer demands change. Markets fluctuate. Yet many banks remain static when it comes to governing their operations. Decisions happen from the top down, and by the time an important idea lands with the right person, a savvier competitor has already released a new feature.

The purpose of Agile in the banking industry is to help organizations of any size and any heritage act as nimble startups. Agile enables banks to deploy squads to release new features faster, have cross-functional teams plotting the next best growth vector, and empower tech leaders with tools for ensuring that IT infrastructure can effectively scale and support the growing spectrum of business needs without a hitch.

Contact Intellias to learn more about building modular teams and adopting Agile and DevOps practices.