With more customer data up for grabs, financial institutions (FIs) finally have the opportunity to turn into one-stop-shop banks.

“I once had a single bank account. Can you imagine that?” This is a tale Millennial grandparents will one day tell their offspring. However, those children or grandchildren will just shrug and say: “Yeah, I also use just one bank account.”

The difference is that those future bank accounts will provide a connected one-stop-shop banking experience rather than the banking-in-app experience we’re used to today.

So what exactly will happen between now and then? Open banking will mature into open finance.

Open banking to open finance: An inevitable (r)evolution?

The open banking movement and supporting legislation empowered consumers with the right to share their transactional data with any third party.

This gave a sizable boost to the API economy. FIs and FinTechs gained the opportunity to securely exchange data with one another to provide consumers with a consolidated picture of their financials. By 2022, the new opportunities created by open banking standards in the UK are expected to generate over £7.2 billion in revenue.

The rapidly maturing API ecosystem, paired with the global surge in open banking regulations, has effectively launched the digital-first banking epoch. Plus, it has prompted incumbent banks to double down on digitization efforts.

Open banking has served as a springboard for new use cases such as:

- Digital account opening and KYC

- Account aggregation

- Personal finance management

- Automated accounting for business accounts

- Lending pre-assessments

- Instant payments

- Personalized loyalty and customer retention programs

As of 2021, over 2.5 million UK consumers were engaging with open banking products. Among these, one million adopted such products between January 2020 and August 2020. API calls rose from a modest 66.8 million in 2018 to nearly 5.8 billion in late 2020.

The open banking ecosystem is booming. Why push it further?

Because the finance industry is still far from seeing it all.

Open banking participants in the EU and UK can only view customers’ payment data, which tells just half of the story. In the US, regulations are laxer. Still, many financial companies aren’t fully capitalizing on emerging data sharing opportunities. To some extent, this is due to legacy technology constraints. In other cases, it’s due to reluctance to innovate.

Few traditional financial institutions use alternative credit data for lending decision-making, despite a favorable regulatory stance on it. Many also shy away from POS lending, crypto trading, and AI-driven wealth management — niches that have gained significant traction among consumers thanks to FinTechs.

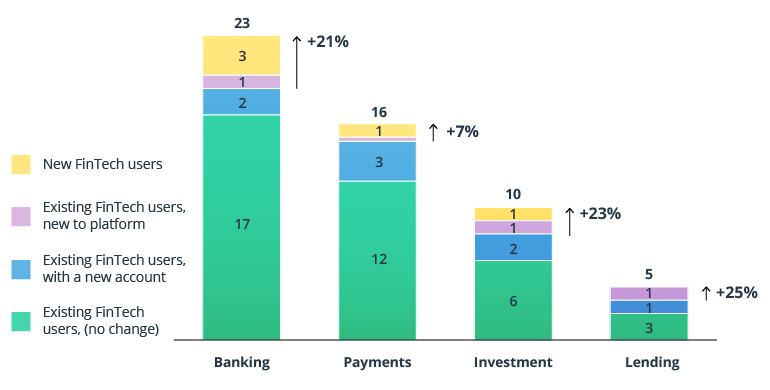

Open banking gave consumers the convenience to easily hop into new financial services, which they tend to do a lot. No single FinTech type dominates the landscape — and all have grown since the start of the crisis.

Source: McKinsey — How US customers’ attitudes to FinTech are shifting during the pandemic

People want more digital financial products, and they have no trouble with finding a solution to fill a particular need.

However, such fragmentation is a zero-sum game for all participants.

- FinTechs gain marginal profits from higher-value-added services such as trading, only to re-route those profits in the relentless aim of acquiring primary banking customers from traditional banks.

- Traditional banks lose wealth management revenue to some FinTechs but still profit from holding most customer savings (and data) and a majority of transactional profits.

- Consumers benefit from using multiple apps but also grow tired of the inability to just get everything in one place, Amazon-style.

Almost one-quarter (23%) of consumers believe that banks are in the best position to provide them with products and services outside of their core areas of expertise, compared with only 16%, 12%, and 11% of respondents who said the same for tech providers, social media companies and neobanks, respectively.

Open banking has helped FIs transform into multi-brand convenience stores. Open finance provides headroom for them to transform into platform businesses.

What is open finance?

Open finance is a new regulatory and product development vector aimed at securely extending the perimeter of financial data sharing capabilities to a wider range of participants — pension providers, lenders, insurers, brokers, and others.

Basically, open finance enables consumers to delegate access to their financial data to any type of institution in exchange for better service.

When you want to get a mortgage, for instance, with open finance you don’t need to collect and file all your personal information with a bank to get a quote. You can merely provide access to your aggregated data, telling the full picture of your finances, and get an instant decision.

Banks, in turn, gain the opportunity to embed new data sharing APIs to provide one-stop financial services — a personalized, informed, and all-encompassing range of financial products to meet customers’ needs at every stage of life.

The concept of a universal banking app has already been implemented by the BAT (Baidu, Alibaba, and Tencent) group. Chinese super apps provide a wide range of financial and non-financial services, effectively undercutting not just traditional banks but also lenders, insurers, and brokerage firms.

In the West, traditional financial companies are also joining forces with digital startups via partnerships (SoFi + Bancorp Bank), acquisitions (Visa + Plaid), or banking as a service (BaaS) arrangements (BBVA + Simple Bank).

The underlying idea of open finance is to boost the development of a wider ecosystem of embedded finances and integrated financial experiences housed under one roof.

Regulations such as PSD2 and PA-DSS (soon to be replaced with PCI-SFF) have drastically improved customer data portability from a compliance perspective. Meanwhile, tech innovations such as standardized APIs and BaaS, paired with rapid IT infrastructure modernization, have improved the feasibility of implementing complex integration scenarios.

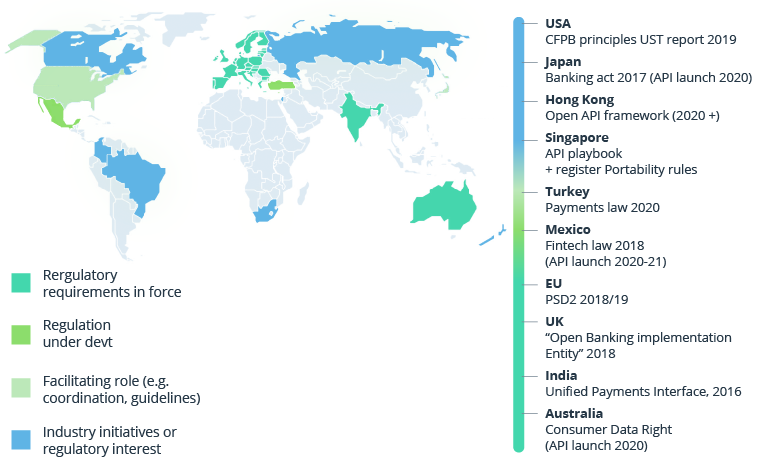

Now global regulators, once again, are looking to further secure and ease customer data exchanges. Approaches to open banking regulation:

Source: BBVA — Open banking regulation around the world

The next step: One-stop-shop banking with open finance

The mid-2010s was the glorious era of single-function digital banks. Launching a mobile banking app with a no-fee debit card and instant account transfers was enough to sway oodles of consumers frustrated by the clunky online banking capabilities of incumbents.

In the 2020s, we are past that stage.

Insatiable connected consumers now demand more than just banking in the app — they want trading, bill management, wealth management, pension plans, lending, P2P payments, and every other financial service out there to be at their fingertips.

49% of affluent investors across all age groups would prefer to use a single company for most of their financial needs. Among investors under 30, this inclination jumps to 66%.

For banks, this may sound like a technical nuance, since integrating a wider range of services often assumes a range of costly back end and front end transformations.

But the allure of open finance is that you don’t always need to build a new product from scratch.

Instead, you can:

- Integrate third-party services to deliver extra value to consumers and share profits

- Populate your ecosystem with offers from third parties (marketplace banking)

- Add new service distribution models to the mix (embedded finance)

- Improve customer lifetime value through advanced analytics (such as decision analytics)

Effectively, open finance enables new scalable vectors of product development and unlocks access to alternative revenue streams — while also delighting consumers with more seamless and faster onboarding and KYC, a consolidated view of finances, more personalized offers, and better service.

One-stop-shop banking means that your customer gets a total package of financial tools, accessible from one account, courtesy of both you and your partners:

- Checking accounts

- Mortgage offers

- Personalized savings plans

- Pension funds

- Payment tools

- Credit products

- Insurance

- Investment tools

- Wealth management

Access to these tools can make consumers elated but also less price sensitive. Over 55% of global banking consumers are ready to pay more for relevant add-on services from their bank. This, in turn, can give a much-needed boost to dwindling corporate revenues.

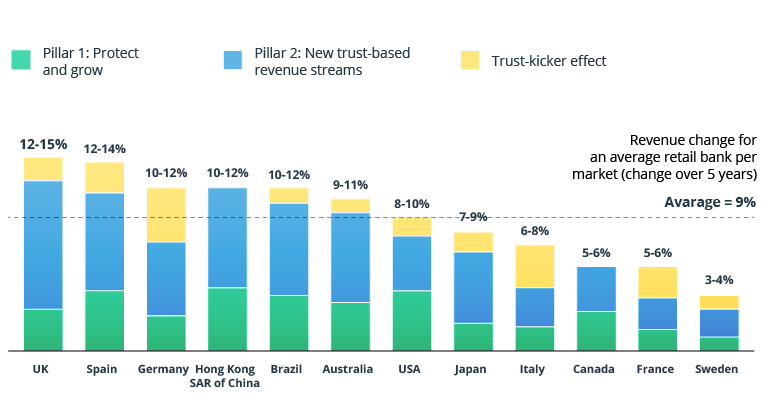

Trust-based propositions boost incumbent banks revenue

Source: Accenture — Purpose-Driven Banking: Can Trust Create Win-Win Banking Relationships?

Why gear up for open finance now?

Platform businesses lure in users by the thousands with seamless multi-product customer experiences. Shopping for books on Amazon is as easy as provisioning extra cloud computing instances in AWS (if you know what you’re doing).

Banks, however, are far from being as comprehensive or convenient when it comes to providing even a core service such as fast money transfers.

Payments have already been massively eroded by FinTechs. Sixty percent of bank executives believe their institution will lose up to 15% of payment revenues to non-banking competitors in the next three years.

But incumbents still have many strengths, especially in areas such as lending, wealth management, long-term savings, and pension investments.

By integrating data from third-party platforms, you can attract customers with better deposit offers, use alternative data in making lending decisions (or even fully automate the loan origination process), and extend more personalized products to low-risk customers you have acquired.

Beyond improving the customer experience, open finance opens up a wider range of B2B partnerships. The Australian Westpac bank, for example, teamed up with Afterpay last year to provide customers of the pay later provider with savings accounts. Stripe recently launched the Stripe Treasury service, backed by Goldman Sachs, Bank USA, Barclays, and Citibank, which enables Stripe users to embed financial services into their operations.

Other incumbents are taking an enabler stance and attracting extra revenue through banking as a service offerings. The benefits are two-fold. Apart from earning a leasing fee for the supplied financial infrastructure, banks gain access to a platform’s user data, which, in turn, they can leverage to attract, onboard, and cross-sell to those users. Oliver Wyman’s research estimates that customer acquisition costs via BaaS fall in the $5 to $35 range versus $100 to $200 for traditional routes.

Start opening up to new opportunities

Competition now happens at a platform rather than solution level. As most finances have gone digital, consumers have an easier time switching to a new provider that may offer less friction and lower costs.

Banks no longer control the end-to-end value chain. At best, they hold the fort until consumers find a better deal. But this shouldn’t be the case. Rather than letting people flock out of your ecosystem, you can prompt them to stay within it by bringing the financial tools they need to their doorstep — and be the one-stop-shop banking app many now seek.

Technologically, both banks and FinTechs have all the means to break down the complex barriers of integrating data. Certainly, integrations are still a complex matter. But they’re feasible.

At the end of the day, you still hold the most customer and market data insights. It’s time to put them to better use.

Contact Intellias to receive a consultation on how you can sustainably adapt your banking systems with new integrations.