Delivering a personalized customer experience in retail banking comes with changing channels and customer behavior, and yet profit is directly tied to customer satisfaction and loyalty. Banks stand to influence these metrics.

How? By providing a hyper-personalized banking experience to each and every customer.

Personalized banking allows financial institutions to provide better, more relevant services on an individual basis, resulting in a higher customer satisfaction rate and strengthening the bank’s position in the market.

Personalization in banking means you as a bank can provide financial services that align with each client’s specific goals, spending habits and risk tolerance. Essentially, your bank will understand each person’s financial needs even before they communicate them to you.

Intellias has been delivering technology services to businesses in the financial services and insurance for more than two decades. Trusted by leading market players, we have numerous successful financial services development projects under our belt. In this article, we discuss what it takes to adopt banking personalization for your organization and how you can benefit from doing so.

What is personalized banking?

Personalized banking services refer to the ability of a financial services provider to identify the specific financial goals each customer has and present them with the most relevant financial offerings.

How does personalization in banking work? Banks should first gather extensive customer data, which is processed by advanced analytics software powered by artificial intelligence and machine learning. Based on the insights gained from these analytics, banks can customize their services to fit the preferences of a specific customer.

Machine learning, location-based services, and big data enable banks to anticipate customers’ needs and match them with major life events.

But that’s just a simplified overview of the process. In the following sections, we will discuss some of the technical aspects of banking personalization in more detail.

Why personalized banking is the future of customer experience in finance

A forecast says that digital banking is here to stay. Up to 75% of bank customers plan to keep the digital banking habits they adopted during the pandemic.

Source: PYMNTS — Leveraging the digital banking shift

The banking sector is embracing the era of the connected customer — a digitally savvy individual who engages with financial institutions through various digital channels.

In fact, 54% of US financial institution consumers want financial providers to use their data to deliver more personalized banking experiences. Also, 72% of customer experience leaders say personalization in banking becomes even more in demand during economic uncertainties.

Recognizing this shift, 86% of financial institutions prioritize personalization in their digital strategy. Plus, banks already possess a wealth of customer data. However, not all of them are using it fully to enable personalized banking experiences. Why?

As many as 45% of banking executives find it challenging to meet evolving customer expectations. Meanwhile, 72% of financial institution leaders say their organizations struggle to integrate data quickly for personalized online banking due to manual processes – that is, they are lacking the necessary technological tools.

To start delivering a personalized banking experience, pay attention to the following points:

- Customer data and a credit of trust to request more. Research shows that 62% of banking consumers are ready to share personal information to have more relevant interactions with a financial institution .

- Non-invasive analytics solutions that can co-exist with your legacy core. The ability to deliver personalization in banking doesn’t hinge on being a fully digital native company. While you will need to transform and upgrade certain systems, you are not required to lift and shift your entire core (at least for now).

Overall, personalization in banking is something all market players need to focus on. FinTechs and digital native banks have made significant advances in customer experience excellence and customer acquisition. But they still need to keep up with rising customer expectations. Traditional banks, in turn, have a competitive edge due to wider service portfolios. However, they need to improve this portfolio based on customer needs to stay relevant.

Source: Deloitte — “Realizing the digital promise” report

Benefits of banking personalization

Personalized digital banking offers clear advantages for customers: they get more convenient services tailored to their individual needs. But what about banks? Let’s explore the benefits they gain.

Increased customer loyalty

Implementing personalization solutions in banking is key to an enhanced customer experience. When customers feel cared for and valued, their loyalty deepens. This means they’re far less likely to switch banks, which translates to higher retention rates and lower attrition.

But that’s not all — it’s also easier to re-engage loyal customers, even after a period of inactivity. They’re more receptive to new offers and additional services, which we’ll discuss next.

Revenue growth

Banking personalization drives revenue growth by delivering the right offer at the right moment. Timely and relevant offers, such as personalized loan rates or investment opportunities, are more likely to be acted upon. Personalized recommendations encourage customers to explore additional products and services themselves, making cross-selling and upselling much more efficient.

Personalization helps banks develop new products that cater to evolving customer needs and preferences and, thus, tap into additional revenue streams.

Better risk management

Personalization in digital banking involves creating accurate profiles of each customer and crafting financial offerings based on their individual risk levels. This ensures that customers get services suited to their financial situation. For example, a high-risk customer might receive a secured credit card with a lower limit, while a low-risk customer could be offered a higher credit limit.

Personalization solutions in banking also allow financial institutions to spot early warning signs of potential fraud with predictive analytics. This allows for a swift response, minimizes losses, and keeps both the bank and its customers secure.

Types of personalization in banking

Banking personalization can take multiple forms, each aimed at enhancing the customer experience in a different way. Here are the key types:

Communication personalization

At the heart of personalized banking is communication tailored to each customer’s needs. This includes sending personalized messages such as warm welcomes, timely transaction alerts, and updates on services — delivered through the customer’s preferred channels.

Personalization of communication also allows a financial institution to stay proactive. For instance, it can send payment reminders if a customer has missed payments or provide savings tips when a customer has excessive spending patterns.

Product and service personalization

This type of personalization in banking is about customizing financial products and services such as loans, credit cards, and savings accounts based on individual customer profiles and needs. It also enables a bank to adjust its offerings dynamically based on the customer’s changing behavior, risk level, and context.

Overall, the scope of this personalization depends on the data you gather and the software you have. For instance, adopting AI-powered solutions allows banks to anticipate customer needs, proactively address issues through predictive analytics, and deliver data-driven recommendations.

Predictive personalization

Predictive analytics in banking personalization isn’t limited to anticipating issues. It can also provide insights into customer needs before they are explicitly expressed. This helps a bank to enhance a customer experience and services in multiple ways:

- Suggesting the next best action based on the customer’s current financial situation and behavior

- Detecting abnormal transactions and patterns that indicate a potential fraud

- Predicting churn risk and proactively offering personalized incentives to reduce it

How to get started with personalized banking

In a very basic sense, personalization means being present at the right time with the right offer.

A consumer in their late 50s may be more interested in building a cushion for retirement, while a 20-year-old wants to get out of debt faster while also building up funds for a rainy day.

Pitching 401K savings plans to both sounds fine on the surface. But far fewer 20-year-olds will take you up on this offer if they are underemployed or freelancers.

Personalization in banking empowers business leaders to distinguish primary target audiences from secondary audiences. Then companies can zoom in on each audience’s needs based on their financial status, lifestyle preferences, and life events. The above is a basic explanation of decision intelligence — wealth management banks are good at delivering for individual consumers and, sometimes, even en masse.

Retail bankers too can build digital indirect rapport with customers if they invest in the right technological frameworks. Here are the main steps to follow.

1. Establish a data collection process

Banks already have plenty of data to use for personalization. The only constraint is enabling secure and compliant access to it.

That’s the challenge data governance addresses.

Data governance refers to a set of technical processes, practices, and policies that help financial institutions securely collect, manage, and use their data.

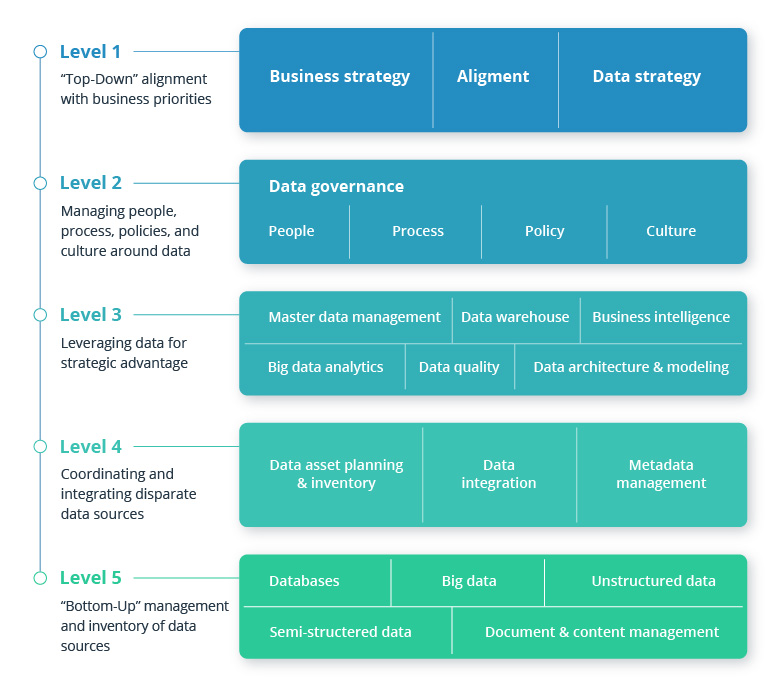

Aligning business and data strategy

Source: Dataversity — The Evolving Role of the Data Architect

Data governance helps to:

- Enable data collection from different sources

- Standardize data injection and storage formats

- Promote data quality and uniformity

- Establish unified data security and compliance standards

- Improve the state of data interoperability and integrations

- Unlock new data modeling techniques and approaches

As the chart above illustrates, you can use either a top-down or bottom-up approach to building a data collection process. In the case of personalization, you may want to start from the top down and inventory your data sources.

Data points to use for personalization in banking:

- Transactional information indicative of spending patterns

- Financial services and product usage data

- Demographics and CRM data as a proxy for customers’ lifestyle preferences

All of these insights are already stashed in your system and apps. Your goal is to locate them and then create an integration for collecting, standardizing, cleansing, and storing insights in an analytics-friendly format.

Next, you’ll need a place to securely store those insights.

Most banking leaders go for a data lake or data warehouse. Both types of storage have technical merits for different types of analytics projects.

- Data warehouses are better suited for storing structured, transformed data you can plug into proprietary or custom analytics and business intelligence tools.

- Data lakes can house large chunks of big data in a raw state, meaning no extra manipulations are needed. They provide a range of intelligence that data scientists and machine learning experts can leverage for predictive models and AI algorithms.

2. Connect extra data sources via APIs

A personalization engine for banks is based on critical data from core software systems. Thus, it’s important to leverage a viable solution that is modernizing only the necessary components. Instead of breaking down the entire monolith, you can upgrade only several services to a microservice architecture. Then, you can build a private API to connect them with your analytics system.

Apart from setting up internal APIs, you should also dip into the growing ecosystem of open APIs other industry players provide. By incorporating data from wealth management platforms, credit scoring apps, and other entities, you can learn about a wider range of your customers’ needs, preferences, and behavioral patterns (without sending yet another annoying survey).

3. Mine customer intelligence with AI technologies

Customer intelligence refers to your ability to collect, analyze, and convert data into business knowledge.

From a technical standpoint, big data analytics and machine learning (going under the colloquial term “AI” these days) are the gateway for obtaining customer intelligence.

There are many predictive, prescriptive, and recommendation models you can use to transform the harnesses and organize data into customer intelligence for decision-making. The same models can be used to power the frontend banking experience for consumers.

When it comes to establishing a personalized banking experience, here are several options approved by consumers and industry leaders:

- Personalized digital account opening and customer onboarding

- Intelligent personal financial management apps

- Robo-investing and AI-driven wealth management products

- Behavior-based product recommendations, upsells, and cross-sells

- Accurate credit scoring and tailored lending product USPs

- Dynamic account pricing and service fees

- Micro-segmented marketing campaigns with better ROI

- Digital concierges and AI service advisors

No matter which personalization use case you decide to go for, one thing is certain: you will not only improve customer satisfaction and retention but also bump your revenues.

For every $100 billion in assets that a bank has, it can achieve as much as $300 million in revenue growth by personalizing its customer interactions.

4. Use AI for further analytics

AI use cases in banking personalization go beyond merely gathering customer intelligence. For example, you can rely on AI to:

- Streamline decision-making, such as creating personalized offers during customer interaction sessions

- Enhance the personalized banking experiences with value-added products developed based on new insights

- Enable the customization of user-facing digital platforms based on customer preferences and behaviors, for example, by providing customizable dashboards in banking apps

In 2023, banks invested approximately $21 billion in AI, demonstrating one of the highest adoption rates across industries, according to Statista. The message is clear: the time to innovate is now, and implementing personalization is an critical step in this journey.

Examples of personalized banking done right

According to McKinsey, among the 40% of consumers who use FinTech products every day, 90% are satisfied with their experience. Personalization contributes to these statistics. So here are some successful examples of personalization in banking to inspire you.

Personalized customer onboarding

In terms of onboarding, the credit goes to Wealthfront. This wealth management platform balances UX best practices with data collection during the onboarding stage. Users are presented with an interactive questionnaire inquiring about their financial goals and lifestyle preferences.

Such a conversational experience helps the company collect all necessary information for KYC and connected personalization algorithms without turning the experience into a drag for prospective customers.

Personalized financial coaching

Credit Karma is another example of personalization in banking as it has taught a lot of users how to curb excessive spending and pay off debts. The company has developed a sophisticated predictive algorithm that captures over 2,600 data attributes per user. In a matter of seconds, it translates data into 8 billion predictions about what products or actions to recommend to the user.

Best personalized lending experience

Atom Bank is often praised for the interface customization it provides. From a recent design-your-logo campaign to card and account view customization, Atom does a lot to delight customers with design.

As lending as a service changing the financial services landscape, Atom Bank has made a progress in lending to stay competitive. The mobile bank has streamlined the mortgage application process. Now it takes 22 minutes to apply for a loan and the remortgage application takes just nine days.

Implementation challenges of banking personalization

Personalization in banking can significantly elevate customer experiences, but as with any initiative, it comes with challenges.

Privacy regulations

Implementing personalization means handling vast amounts of personal data, which is subject to stringent privacy regulations in the financial sector.

For instance, banks must comply with data privacy laws: GDPR, which governs data protection in the EU; CPRA—California Privacy Rights Act; PIPEDA—Canada’s Personal Information Protection and Electronic Documents Act; and others. These laws impose limitations on personalization capabilities, such as requiring transparency in data processing practices, which can be technically challenging with AI-based software.

Thus, banks must integrate the requirements of these regulations into their personalization strategies to carefully balance innovation and data protection. Working with a reliable financial development provider can significantly simplify this task.

Data quality and governance

The success of banking personalization hinges on the effectiveness of AI models, which, in turn, rely on data quality. Put simply, personalized customer experiences cannot be achieved if data is fragmented, biased, or inaccurate.

To avoid this, prioritize robust data governance. Ensure your data sources are integrated, and eliminate errors, duplicates, and outdated information that can compromise insights and personalized recommendations. Maintaining advanced data security measures is equally critical for this purpose as they minimize unauthorized data access and modifications.

Resources and expertise

Implementing banking personalization requires the right resources and technology. According to Dynamic Yield research, 63% of financial managers admit that resources for personalization are limited or only allocated on-demand when there’s a clear business case. To overcome this obstacle, there should be a shared vision of the personalization strategy among key bank stakeholders.

Successful personalization in banking demands comprehensive expertise in AI development, data science, and ongoing model refinement. Finding a tech partner with proven experience in the financial industry is practically always the most optimal scenario.

To conclude

The above list just scratches the surface of personalization opportunities in banking, fueled by big data and machine learning algorithms. Consumers have cast their votes too — and they demand banking to be digital and personal.

Now it’s time to step up and deliver. Re-assess your product portfolio and make it serve your customers’ needs.

Find an unmet consumer need. Analyze which financial products can best fulfill it. Then look for data sources and algorithms to personalize the experience. In the end, what matters is that you listen to your customers, and approach them in a way that proves that your bank can address their needs in a way that is accessible, easy and efficient.

Contact Intellias to dive deeper into the technical aspects of personalized banking and emerge more customer-oriented than ever!