In the United States, where approximately 20% of adults fall into the category of credit invisible due to limited or no traditional credit history, the financial landscape is undergoing a significant transformation thanks to alternative data sources for credit scoring

Lenders are leveraging alternative credit data to extend access to a wider consumer base, transcending the boundaries set by traditional scoring models. But it doesn’t stop there. By incorporating alternative data into credit risk modeling, accuracy soars to new heights.

In this article, we delve into the world of alternative credit scoring data, exploring its significance, sources, and applications to help you find out the following:

- What is alternative data for credit scoring?

- Sources and types of alternative data for credit scoring

- How to get alternative credit data and adopt AI for credit scoring

- How this approach can increase scoring accuracy

What is alternative credit data?

Alternative credit data is information obtained from non-traditional sources that can help assess a consumer’s creditworthiness. Whereas traditional data refers to a person’s credit report, alternative data for credit scoring includes information about utility payments, insurance payments, rental payments, public records, and property records. These points can help lenders get a sense of an individual’s financial reliability. What’s more, employment history can assist by demonstrating the stability of someone’s financial situation.

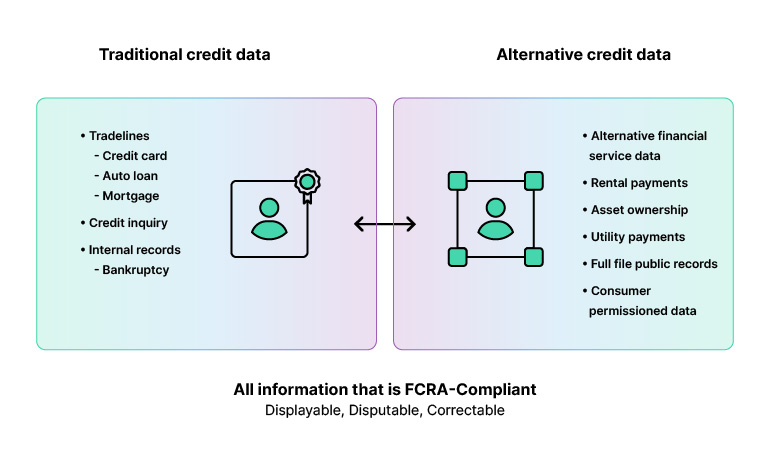

Differences between traditional and alternative credit data:

Source: Experian

Alternative credit data may be merely supplemental when banks consider consumers with extensive portfolios or look to build personal financial assistant apps. But it may be the only way for individuals with an insufficient history to get a loan. Today, lenders can extend their client base by using an automated loan processing system and and alternative data to score thin-file consumers..

Alternative data sources (such as property, tax, deed records, debit account management, address stability, payday lending information, and club subscriptions) have proven to accurately score more than 90% of applicants who otherwise would be returned as no-hit or thin-file by traditional models.

Practical use cases for enhancing accuracy

In the previous section, we briefly discussed how this approach streamlines credit evaluation for individuals with thin credit files. Now, let’s delve into specific scenarios where alternative data plays a crucial role.

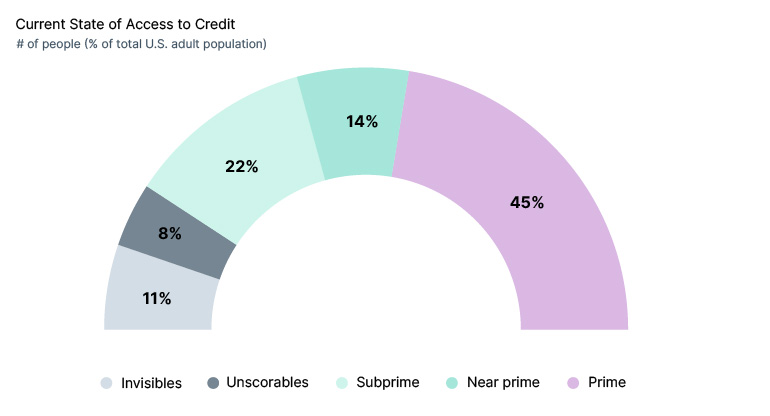

Access to credit in the US

Small business owners often encounter challenges when seeking loans due to the separation of their personal and business finances. Leveraging data sources such as business bank account transactions and supplier payment histories empowers lenders to extend loan to deserving entrepreneurs who may lack solid personal profiles.

Immigrants and foreign nationals. For individuals new to a country or foreign nationals, international banking transactions, remittance histories, and rental payment information can be essential in assessing creditworthiness. Lenders can make more informed lending decisions by gaining a more comprehensive understanding of an individual’s financial behavior.

Auto loans and leasing. In the auto financing industry, lenders can consider factors like consistent utility bill payments, insurance premium history, and on-time rent payments. This broader perspective of an applicant’s financial responsibility leads to more accurate decisions and may result in lower interest rates for borrowers.

After reviewing these practical cases, let’s highlight alternative data sources contributing to a more precise and inclusive assessment process, benefiting lenders and borrowers alike.

Sources of alternative credit data

Alternative data for credit scoring comes from various sources, including digital footprints, full-file public records, and banking accounts. The range and types of alternative data for credit scoring differ depending on the information-collecting entity.

According to research by Oliver Wymana good information source should have the following characteristics:

Coverage. A broad and consistent range of information.

Specificity. Information about a specific individual.

Accuracy and timeliness. Information must be accurate and regularly updated.

Predictive power. Information should be relevant to the behavior being predicted.

Orthogonality. Ideally, alternative credit data should complement traditional credit bureau data.

Regulatory compliance. Information sources must comply with existing financial rules.

How to collect alternative credit data for lending

One approach involves obtaining additional information directly from loan applicants. This may include details such as debit card transactions, income and employment records, asset ownership documentation, digital and physical receipts, rental agreements, social media profiles, and mobile contact information.

Alternatively, loan providers can streamline the process by collaborating with data aggregators. By partnering with vendors or utilizing information aggregation platforms, lenders gain expedited access to crucial consumer information. This approach not only accelerates loan processing but also enhances efficiency. Consequently, lenders may find partnerships with FinTech providers to be advantageous.

How alternative credit data works for credit scoring

Incorporating alternative characteristics into evaluating creditworthiness is a promising avenue for improving accuracy. However, details collection alone is insufficient; effective processing is required. Manually scrutinizing an individual’s transaction history can be time-consuming. Fortunately, the realm of finance has witnessed an array of advanced analytics and machine learning applications.

Modern lending companies use AI technologies and machine learning solutions to quickly gain insights from numerous datasets. An AI model can rapidly analyze copious amounts of information, lowering the processing time. Plus, machine learning algorithms and AI in wealth management solutions can identify patterns in unstructured information that help evaluate a loan applicant’s consumer behavior and predict loan repayment.

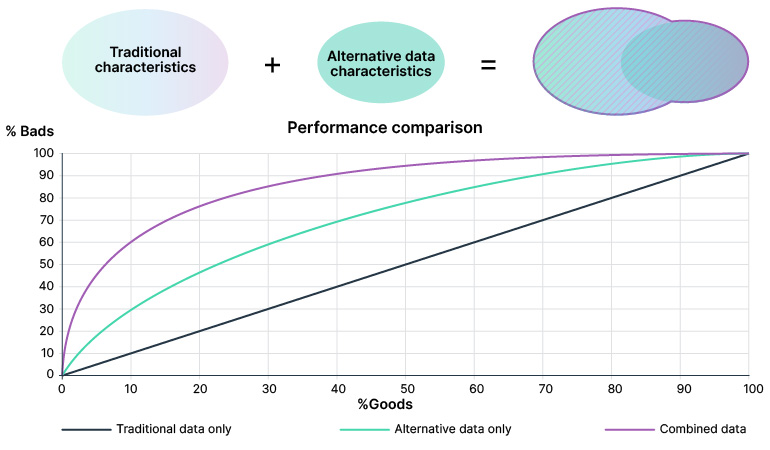

According to FICO research, alternative credit data captures less value than traditional credit data, and traditional data alone present more insights into a person’s creditworthiness. However, enhancing credit scoring with alternative data in risk modeling is the only method of letting the credit-invisible consumer qualify for a loan. Combining both traditional and alternative details will help build a more accurate model.

How combining traditional and alternative characteristics affects performance:

Source: FICO

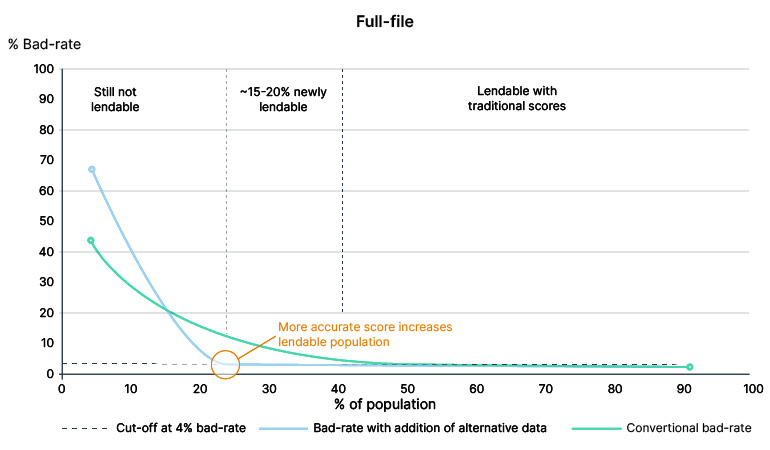

A high level of accuracy for alternative scoring affects all types of consumers. It helps separate lendable clients from risky ones — even for the full-file population — making it much easier to minimize lending risk.

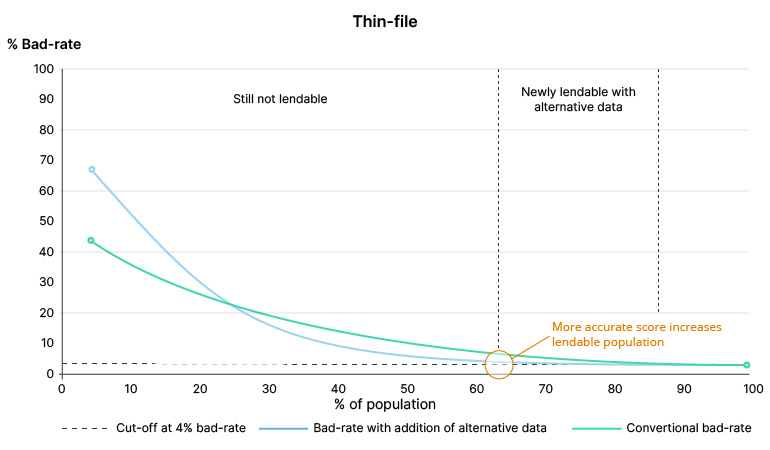

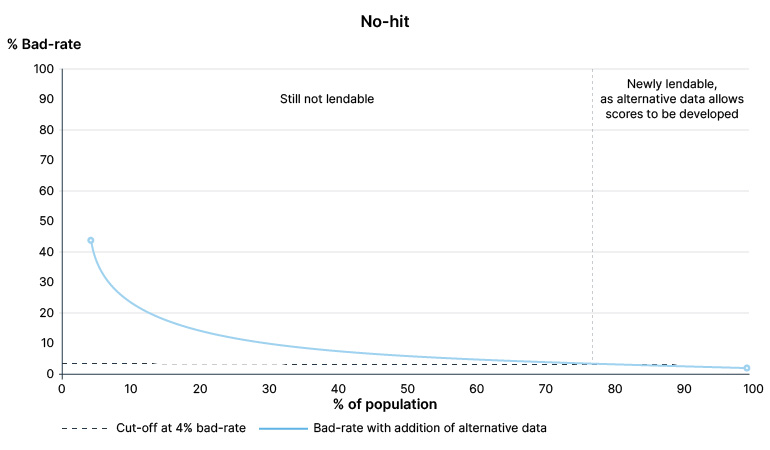

Depiction of lendable population with the addition of alternative information:

Source: Oliver Wyman Report

According to a LexisNexis Risk Solutions survey, 84% of lenders already incorporate alternative data for credit scoring into their lending decisions. This information aids in developing scores and offers advantages such as predicting creditworthiness for individuals without a traditional history. Consequently, lenders can expand their customer base and enhance the accuracy of their risk assessments.

For this reason, many leading FinTech lenders like Zestcash and Global Analytics are already effectively leveraging AI technologies for lending marketplace development. In this way, they streamline processing of large information volumes, reduce evaluation times, and achieve comprehensive creditworthiness insights.

Experts at Intellias have showcased the power of technology in the FinTech industry in several big projects. For example, we have recently created a non-performing loan platform for one of Europe’s top loan management players. With advanced business intelligence (BI) and data warehousing services, we introduced a data-driven and cost-effective non-performing loans management system.

Are you ready to experience the benefits of alternative credit data for lending? Then contact Intellias. Our FinTech experts will consult with you on the latest technology solutions for lending companies.