Legacy technology in the insurance industry is a 1982 Toyota Corolla on a highway full of Teslas. Like the aroma of exhaust fumes, an outdated legacy system might feel familiar in the era of digital insurance. But legacy data and platforms will never be as capable, efficient, or secure as their modern counterparts. As the performance gap between them widens, insurance legacy system transformation becomes increasingly necessary.

Many modern solutions are improving aging insurance systems, including cloud computing, robotic process automation, and artificial intelligence (AI). Insurance providers are using them for tasks including policy management, underwriting, and customer relations. They are also spending a lot of money on these modernization efforts. By 2027, Gartner predicts the insurance industry will spend US$15.9 billion on new software improvements. That is an five-year CAGR of 18.2%. Much of the money will go toward modernizing legacy insurance operations.

Companies are willing to spend money because the payoff of an insurance legacy system transformation can be significant. In fact, insurers can expect a 40% productivity increase after an insurance legacy system transformation. Why? Core insurance system (CIS) modernizations use technology that processes claims more accurately and reduces churn. These modern solutions also decrease processing costs and lower policy premiums. Moreover, they offer secure endpoints with many personal devices connected to the Internet of Things (IoT).

![[whitepaperbox link="https://intellias.com/ebooks/ai-insurtech-embrace-the-tech-revolutionizing-insurance/" imageid="74480" title="AI Insurtech - Embrace the Tech Revolutionizing Insurance" ]Everything You Need to Know about the Insurance Industry and Artificial Intelligence[/whitepaperbox]](https://d3twecw9qvot3u.cloudfront.net/wp-content/uploads/2024/05/AI-Insurtech-cover-1.png)

Legacy insurance systems

Yet, most insurance companies are not driving in the fast lane, instead relying on aging core systems for essential daily operations. Today’s legacy systems were once considered essential for streamlining workflows, preventing fraud, and delivering customer notifications. Today, these systems still process high volumes of data. But they do not meet modern business needs.

For example, legacy systems in the insurance industry cannot personalize policies. They also cannot automate claims, and they do not offer robust security. These restrictions affect customer relations and reduce competitiveness. Nevertheless, many insurance providers find value in their legacy systems. According to a Novarica survey of 10 large insurance providers, only 10% have modernized more than half of their systems.

A core insurance system includes four legacy technologies covering policy administration, customer relationship management, business intelligence, and underwriting.

A policy administration system (PAS) is a legacy claims processing system. It is important for claims and billing, but it operates in a silo. That makes it harder for modern applications to access data. A customer relationship management (CRM) system organizes customer data. However, CRMs often lack modern features such as analytics, which insurers can use to gain customer insights and provide personalized service. CRMs also tend to fragment data and lack modern communication tools.

To analyze large amounts of data, insurers use business intelligence (BI) systems. However, BI systems cannot analyze real-time data that could be used for risk assessment or fraud detection. Finally, underwriting systems ensure that insurance agents use accurate pricing and adhere to underwriting rules. Still, the rules must be applied and updated manually.

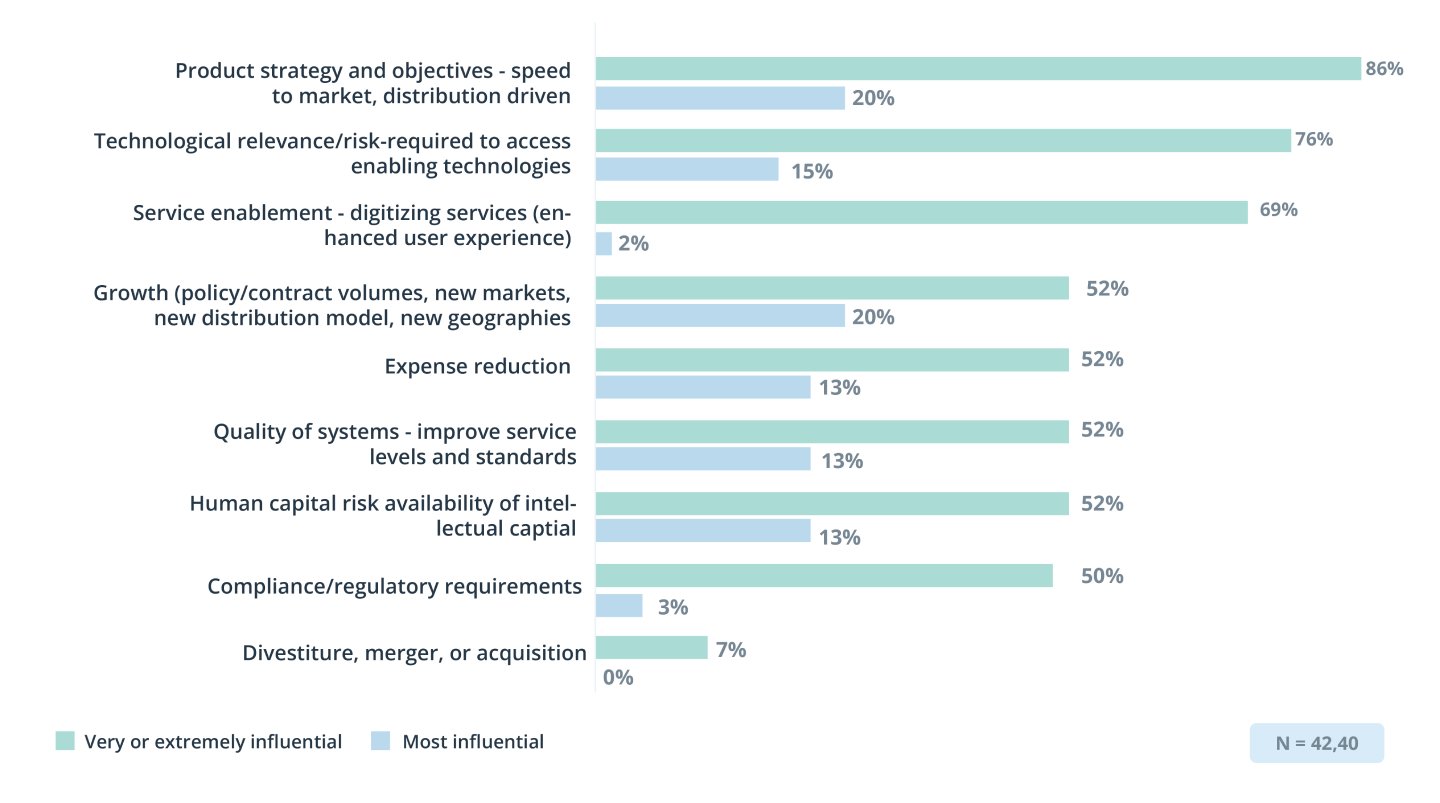

Drivers for technology investment

With aging legacy systems and advancements in technology, the insurance industry has a renewed interest in modernizing legacy applications and data. The main driver of this interest in the insurance sector is an increasingly competitive operating environment. Closely related is the effect of disparate systems on customer retention. Customers who cannot find the solutions they want will go elsewhere for insurance.

Drivers of insurance core system modernization

Source: Deloitte – Legacy Systems and Modernization

There are legal reasons for modernization, too. Regulatory actions have intensified. For example, the EU’s Financial Data Access (FiDA) regulation prioritizes digital access to insurance data, while the Gramm-Leach-Bliley Act (GLBA) in the US requires financial institutions to explain their information-sharing practices and protect sensitive consumer data. But many legacy systems work in data silos, which complicates compliance.

Reasons insurance companies choose to modernize systems

Source: Gartner – Top Customer Expectations for Insurance Transactions

An insurance legacy system transformation also helps companies analyze complex risks. For example, risk analysis can provide valuable insights about climate change trends that could affect property insurance. It can also predict patterns in vehicle crashes that could be used in auto insurance.

Roadblocks to modernization

Insurance companies are paying big price tags for these new features. In fact, sticker shock can be a roadblock to replacing legacy systems. In the US, insurance companies are expected to spend $132.86 billion in 2024 on modernizing legacy systems. By 2029, they are expected to spend $229.07 billion.

For large insurers, an insurance legacy system transformation can cost over $5 million. Delays in integrating legacy and modern systems can interrupt operations, and some projects can take 12 to 18 months to complete. Economic instability, market volatility, and inflation can also end a legacy insurance system transformation.

How much each challenge affects insurance legacy system modernization

Source: Gartner – Top Five Challenges to Legacy Modernization

Seizing digital opportunities

Still, companies can begin modernizing insurance legacy systems without having to spend millions. By partnering with a technology company that provides solutions such as cloud computing and custom software development, insurance companies can accelerate their digital transformation. They can also make data available to meet growing consumer demands.

Technologies like AI and ML are further reshaping the industry. AI-powered tools enhance risk assessment, streamline fraud detection, and enable tailored policies. They also improve customer satisfaction. For instance, AI-driven claims assessment accelerates settlements and reduces processing times.

Recently, generative AI has brought new opportunities for modernization. Deloitte reports that generative AI use cases for insurance are already helping customers, and the number of use cases is growing. For example, generative AI allows insurance agents to obtain information about their customers that allows them to write personalized policies. This lets them sell more efficiently. Generative AI can also create text- and image-based product summaries to help close sales and can develop coverage comparisons, personalized coverage recommendations, and real-time illustrations.

Choosing a path to modernization

To take advantage of these benefits, a company must first select a project management model to guide the process. Three models provide direction while transitioning from legacy systems:

- Centralized approach: Relies on existing legacy IT resources for CIS transformation, with the corporate IT team managing the modernization effort.

- Federated approach: Responsibilities are decentralized and distributed across various organizational units.

- Hybrid approach: Balances power by assigning some responsibilities to the central unit while giving others to different organizational units.

Modernization best practices for an insurance legacy system transformation

Regardless of the approach, using these best practices will ensure a successful insurance legacy system transformation:

- Break up large programs to make them manageable

- Establish strong program management risk controls

- Analyze digital best practices, and repeat

- Re-evaluate the entire architecture for legacy functions and processes

- Create unified goals across business units and with vendors

- Select a technical partner that understands the insurance sector

- Reduce complex legacy systems and vendor-dependent technology stacks

Modernization strategies

Insurers also must choose a technical strategy. Replacing the core is an option. But there are many alternatives for an insurance legacy system transformation that are less expensive, have fewer risks, and have better adoption. The choice of strategy depends on the project goals, resources, and existing systems.

- API integration/encapsulation: This method presents existing features in a modern format. However, APIs do not change the core infrastructure. Although API integration/encapsulation is fast and cost-effective, the legacy system’s architecture might limit its potential.

- Rehosting: This method moves stable applications to modern architecture, improving performance without changing the core legacy code. Although it does not resolve underlying limitations, the results are fast and inexpensive.

- Replatforming: This moves applications to a new runtime platform. It requires only minimal changes to the code, improves performance, and cuts costs. However, adjustments may be required to ensure compatibility.

- Refactoring: This optimizes the code of legacy applications but requires time and detailed knowledge of the existing system.

- Rearchitecting: This strategy changes the architecture to adapt to modern technologies. Although a new architecture provides long-term flexibility, rearchitecting is complex and risky.

- Rebuilding: This option redesigns applications to meet new business and/or technological needs. Although it is the most expensive and time-consuming choice, it results in modern insurance systems.

Assessing risks with GIS data

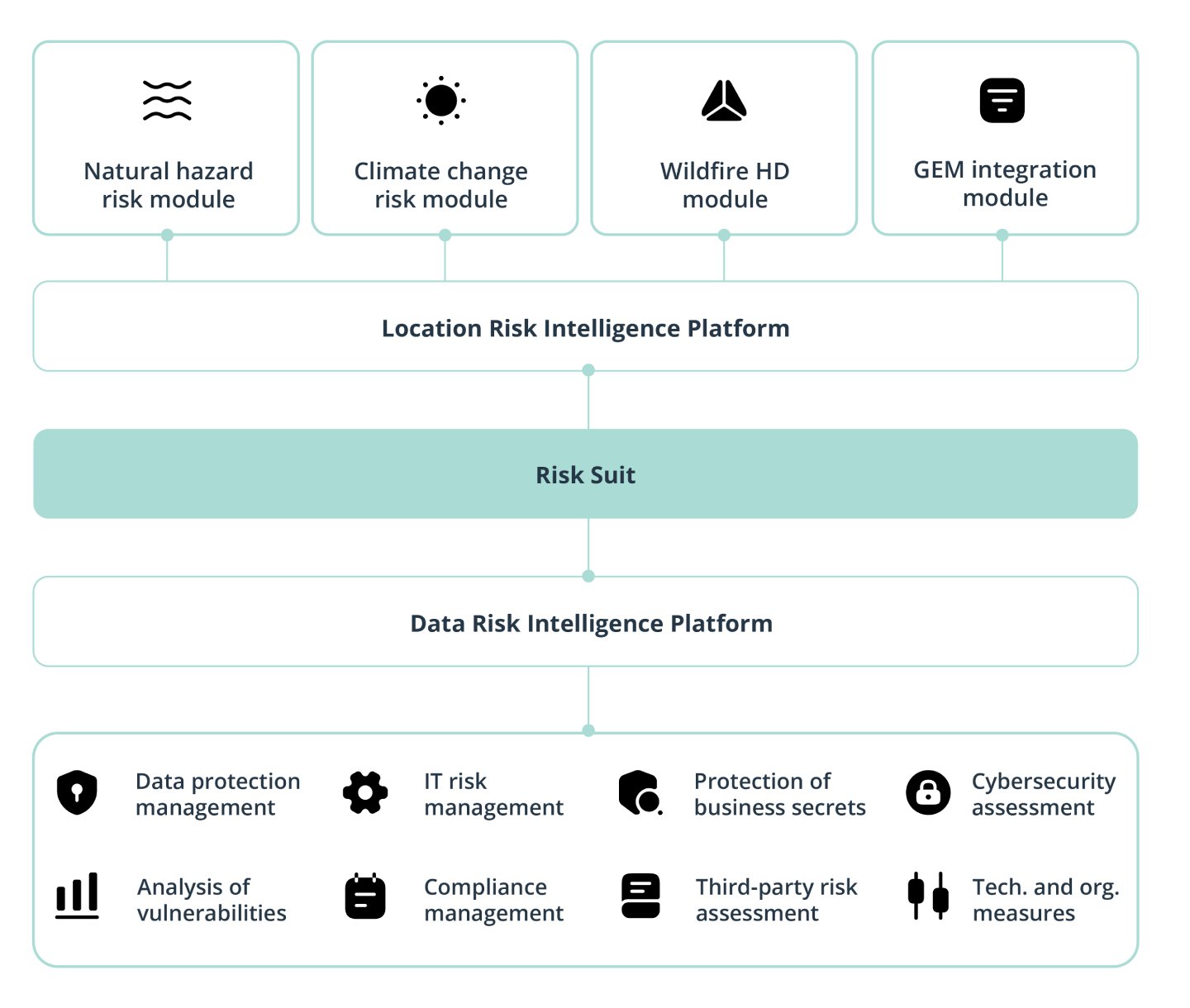

While modernizing insurance legacy systems for a global provider of reinsurance, primary insurance, and insurance-related risk solutions, Intellias developed a location and data risk intelligence platform that enables easy on-demand management of natural disaster risks.

To achieve this, Intellias created a solution with Geographic Information System (GIS) coordinates. The solution uses GIS data modeling to assess the risks of natural disasters and climate change. It includes two custom products: a location risk intelligence platform for managing natural disasters and a data risk intelligence platform for managing IT security. First, the solution accesses data about natural disasters. Then, it creates a comprehensive risk analysis based on location. It also generates helpful reports.

Source: Intellias – Risk Management Reimagined to Assess Hazards Globally

Entering an address gives a user an immediate risk score for the GIS coordinates. The user can also download a report on identified risks in several formats. Companies can integrate the solution’s services and risk scores into third-party applications using a REST API.

The new suite lets insurers assess risks 50 years into the future and anywhere in the world based on 12 risk score hazards.

Reducing fraud with the blockchain

Intellias has also helped a company develop an app for online vehicle insurance purchases. Based on blockchain technology, the app is part of a larger initiative to make insurance more affordable and accessible. It is built on the idea that blockchains can prevent insurance fraud and be resilient to cyber attacks. Purchase data is stored, updated, and validated on the blockchain.

After consulting Intellias software engineers, our client agreed to use AngularDart, a web app framework by Google that lets developers convert web apps into mobile apps for Android and iOS. Intellias also suggested UI/UX improvements within the company’s branding requirements and developed a workaround for the lack of functioning contract APIs.

In less than two months, Intellias delivered a fully functional web application that is now being incorporated into blockchain-powered middleware. If the project is successful, it will open a new opportunity for blockchains in the insurance industry.

Employing InsurTech solutions

These examples demonstrate how InsurTech solutions help insurance providers. Modern solutions can be tailored to fit specific needs and help insurers become more agile. They can also help insurance companies remain competitive with functionality from AI-powered risk assessments to automated claims processing.

Working with an experienced InsurTech partner ensures greater success during and after an insurance legacy system transformation. It prevents companies from bearing the full cost or risk of in-house development and can streamline operations. Solutions designed by InsurTech partners also reduce fraud, help insurance companies provide personal insurance policies, and keep insurance companies relevant.

Following market trends

Modernizing an insurance system is just the beginning. Modernization projects often trigger a series of technology projects that are trending in the insurance industry, including streamlining applications, upgrading legacy infrastructure, and implementing new data management strategies.

An insurance legacy system transformation might also require new infrastructure. Moving data and services to the cloud, insurance companies can provide real-time claims processing and more easily detect fraud, among other benefits.

A strategic imperative for the future

Although the modernization journey may be time-consuming and complex, the long-term benefits outweigh its challenges. Prioritizing an insurance legacy system transformation prepares companies for future developments. It also leaves legacy insurance systems in the rearview mirror.