How do you create a digital wallet to pay on the fly using a smart device in your pocket, around your wrist, or in your garage? And why is everyone so big on smart payments these days?

You know that feeling when you order a cup of coffee in a café and realize you left your wallet at home? Or worse, you’re standing at the checkout counter in the store with a long line behind you… Keep calm and let your Things (phone, smart watch, or even sunglasses) pay for things (shopping, gas, or a dinner out).

Internet of Things payments are a lucrative new field for FinTechs, banks, and OEMs — the same crowd attacking the mobile payment space. Though the IoT sphere is still not that crowded, it’s surging in profitability. Matt Good, senior vice president and general manager of Elan Advisory Services, says in an interview with PYMNTS that the volume of wearables payments may soon top $500 billion. That said, IoT painfully lacks viable electronic wallet solutions to facilitate growth.

Supporting technology companies in launching their products is what drives us forward. We know how to build a digital wallet from scratch, and in this article we share useful tips on how to make the most of your digital wallet app development journey.

What is a digital wallet?

Digital wallets, or eWallets, securely store a customer’s details for various payment methods and enable IoT payments, allowing users to make purchases easily and quickly. Integrating QR code payments in digital wallets enables swift and safe transactions through smart devices by connecting a user’s bank account to the eWallet payment platform. Transactions are made with a one-time scan, ensuring personal or sensitive data stays private and secure.

Among companies in the payment space, it has become mainstream to develop eWallet apps that seamlessly integrate with banking solutions, vending machines, cash registers, and loyalty reward programs. Below are just a few numbers to illustrate the digital wallet market dynamics.

Key stats behind the digital wallet trend

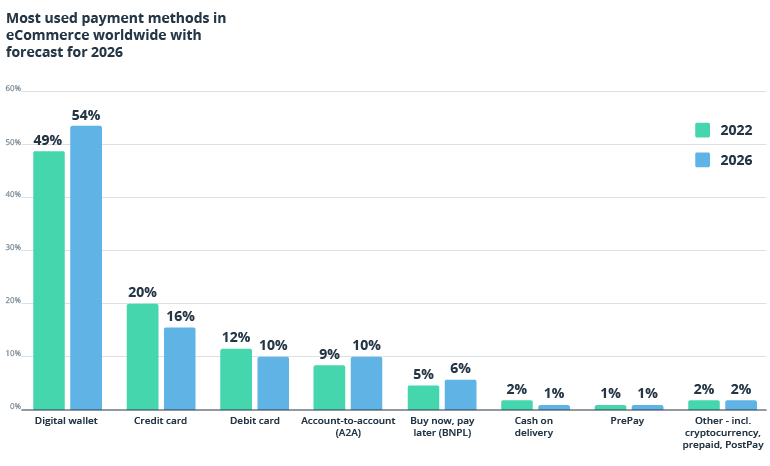

Mobile wallets make up almost half of all eCommerce payments globally. And this figure is only set to grow, projected to exceed 54% by 2026.

Source: Statista

The increasing adoption of smartphones, the proliferation of various connected devices, and the growing popularity of contactless payments have spurred demand for smart payments solutions. This has given rise to a host of innovative digital wallets that are quickly becoming the preferred payment option for consumers.

- According to Grand View Research, the worldwide digital wallet market is expected to experience consistent annual growth of 20.8% between 2023 and 2030.

- The market size of mobile wallet transactions worldwide is forecasted to near $9.5 billion in 2025 according to Statista.

- In 2026, over 5.2 billion people will be using digital wallets according to Jupiter Research.

Benefits of building a digital wallet for your business

As the smart wearables market is booming and digital payments are on the rise, there’s an open door of opportunity for new entrants to the payments space. Creating a digital wallet offers numerous advantages to businesses and can take the customer payment experience to a whole new level.

Cost efficiency

Implementing an electronic wallet system can bring significant cost savings for both businesses and users. Businesses can cut operational expenses by streamlining payment process flows and minimizing dependence on physical infrastructure. Besides, digital wallets allow companies to simplify financial reporting and accounting processes, bringing down administrative costs. On the other hand, users can benefit from lower transaction fees and budget-friendly offers provided by digital wallets.

Frictionless payment experience

Thanks to a well-thought-out digital wallet system design, users can easily and conveniently manage their finances, complete cash-free transactions, and access loyalty programs. Digital wallets eliminate the need for time-consuming steps like entering payment details and confirming identities. Instead, they accelerate transactions by storing card information securely and providing fast verification techniques, such as facial recognition and fingerprinting. This results in an instant checkout process and a seamless payment experience.

In addition, digital wallet technology can integrate different payment options by bringing multiple cards and accounts into a single unified platform. This allows users to view and manage all their financial operations in one consolidated place.

Customer engagement and loyalty

A well-crafted digital wallet can attract, engage, and retain customers by suggesting personalized offers, bonuses, and promotions based on users’ spending habits and preferences. To attract more customers, some digital wallets also provide value-added features including cryptocurrency, virtual IDs, coupons, insurance cards, and tickets. Through this approach, electronic wallets nurture a stronger bond with their users, fostering a sense of loyalty and encouraging customers to return.

Data-driven decision-making

Digital wallets are gold mines of transaction data, providing valuable insights into customers’ behavior, spending patterns, and preferences. Using advanced analytics, businesses can better understand their customers, personalize their offerings, and build informed growth strategies.

Hack-proof security

Digital wallet system design emphasizes user security through advanced encryption and authentication techniques, ensuring that personal data will never leave the user’s device. Tokenization, biometric verification, and secure data storage protect sensitive data from potential breaches and fraud. As a result, users can rest assured knowing their personal financial information is reliably secured.

Why digital wallets are the key to capitalizing on IoT commerce

One-quarter of European shoppers expect to start using contactless payments with wearables — smartwatches, keyrings, stickers, bracelets or another form of a wearable device.

The Smart Payment Association mirrors this data, anticipating that 72% of new wearable devices shipped will be used for making payments.

The rising popularity of branded mobile wallet apps also serves as a great proxy for rising consumer interest in cardless payments. Already, you can choose to store your card in:

- Apple Pay

- Samsung Pay

- Amazon Pay

- Garmin Pay

- Fitbit Pay

- Chase Pay

- Or any other “Pay” you fancy

The mobile wallet market is ripe. Wearable digital wallets are on the rise. But the question remains: Who will dominate the IoT payment landscape as it comes of age — new or existing players?

As we highlighted in our post about IoT commerce, every connected device can now become a payment enabler, resulting in a multitude of cross-industry use cases.

- Smart home: Connected food/supply ordering, maintenance payments, consumer credit payments, pay-per-use billing for rented equipment

- Utilities: Smart meters, P2P electricity trading, pay-per-use payments

- Automotive: In-car commerce, in-car entertainment, connected parking payments, pay at the pump, pay-per-use insurance

- Wearables: Smartwatches, fitness trackers, jewelry, and stickers can be used for both retail and P2P payments

- Retail: Contactless cashier-less stores, smart vending machines

- Smart cities: Transportation and mobility payments, tax and government services payments

- Manufacturing: Automated supply ordering, predictive maintenance payments, servitized offerings

Now connect this multitude of use cases with the fact that the financial industry has worked out a secure, unified framework for processing remote transactions — the EMVCo Secure Remote Commerce (SRC) framework.

EMVCo is defining a technical framework and specification that enables a merchant to obtain a consistent, secure payload of customer payment information that can be used to facilitate authorization through existing channels.

In essence, this is a new method for securely tokenizing payments that drastically reduces security risks and allows customers to view how their credentials and personal data are used and stored. Mastercard, Visa, American Express, and Discover are jointly supporting this protocol. The Secure Remote Commerce framework can unify the payment experience across channels and create a “single button in the digital world for consumers to use to check out,” to quote Jess Turner, EVP,

Head of Global Open Banking and API at Mastercard in an interview with PYMNTS.

Even better news? The EMVCo framework was specifically designed to accommodate the emerging payment experiences enabled by IoT and voice-activated devices. So yes, you already have a solid base for launching new IoT wallet solutions.

Main challenges of building a digital wallet app

While digital wallets are all about convenience for users and profitability for businesses, there are plenty of pitfalls that might impact your product’s performance before or after you create a digital wallet.

Varying compliance requirements

For a successful take-off, a digital payment product needs to comply with legal requirements and standards that vary from country to country or region to region. Most FinTech solutions must be compliant with GLBA, AML, and the JOBS Act in the US and the GDPR and PSD2 SCA in Europe.

Fraud and security risks

Even though the popularity of digital wallet technology is off the charts, some people are still hesitant about using it for security reasons. Embedding advanced security measures into the very fabric of the system ensures efficient fraud detection and protects against data theft and hacker attacks.

Technological challenges

Building a secure, easy-to-use, and competitive product that will convince consumers to switch to digital wallet payments calls for strong engineering expertise. Simply put, you need someone who knows how to make a digital wallet from A to Z. Finding the right technology partner experienced in developing digital payment solutions is one of the major factors that will make your project a success.

7 key steps to create a digital wallet for IoT payments

The security of IoT devices has been repeatedly questioned. But after a series of false starts, most device manufacturers are finally on the fast track to success, as the latest cybersecurity trends illustrate.

Combining payments with IoT initially raised some valid security concerns — an issue EMCo prominently addressed with tokenization. Tokenization is a secure method for protecting a customer’s sensitive information (such as account numbers and card numbers) with a unique digital identifier (token). This token is exchanged with another IoT device during an online or NFC payment.

Here are seven steps you should take when creating a digital wallet for Internet of Things payments.

1. Understand the new token-enabled payment flow

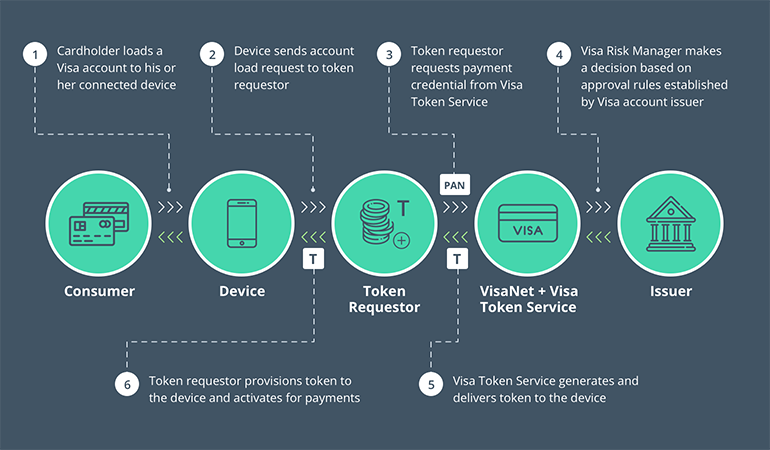

To illustrate this, let’s use a connected car with an embedded in-dash wallet as an example. To get started, you need to load your card to the car wallet. Once you do, the following data will be automatically dispatched to the card issuer for tokenization:

- Primary account number (PAN)

- CVV2

- Cardholder name

- Cardholder address data for verification

- Device data

- CDCVM from the connected device (optional)

All of the above will be stored as tokens in your car wallet. If someone manages to hack into your car (or any other IoT) wallet, all they’ll get is a useless string of numbers — not your actual credit card details.

Source: Visa — How things pay for things

2. Choose your tokenization integration option

Now you need to figure out how to enable tokenization within your wallet. The most common option is to use an existing Token Service Provider (TSP). These are official entities that can provide surrogate PAN values.

Here are some of the popular TSPs that enable IoT payments:

- Mastercard Digital Enablement Service

- Visa Token Service

- Gemalto Trusted Services Hub

- Amex Tokenization Service

3. Map out your data storage layer

Authenticating core payment-related data such as tokens, cryptographic keys, and authentication data (for device and cardholder verification) is key to the long-term success of IoT payments.

There are two places you can store this data:

The IoT device itself.

In this case, you can protect critical data at both the hardware level (e.g. using tamper-resistant microcontrollers) and the software level (e.g. with code obfuscation).

In the cloud.

A cloud services provider takes on the burden of protecting critical customer data. However, you’ll need to create a secure communication channel between the IoT device and the cloud.

4. Decide on the device authentication process

Every IoT device needs an ID that can be authenticated when it attempts to connect to the payment network or another gateway.

By assigning a unique ID to every device with your wallet installed, you can track these devices individually and effectively address suspicious behavior. For instance, if a smart fridge suddenly starts ordering an extremely high volume of food from an unknown retailer, you can revoke its payment privileges and securely investigate the matter.

Microsoft suggests the following authentication options for IoT devices:

- X.509 certificates

- Trusted Platform Module

- Symmetric keys

5. Create a seamless consumer authentication experience

The user-to-device connection is the weakest link in IoT security. Biometrics is the most likely contender to strengthen it. Here’s why:

Biometric payments already dominate the mobile channel. According to Javelin Research, mobile biometrics authenticate $2 trillion worth of in-store and remote mobile payment transactions annually. That’s a pretty strong indicator that most consumers are on board with this authentication method and will welcome it within other mobile and connected devices.

Europe’s Strong Customer Authentication (SCA) requirement mandates that all card-not-present transactions be authenticated with at least two of three methods:

- Something you know (password/PIN)

- Something you own (phone/hardware token)

- Something you are (fingerprint or face/voice recognition)

Considering that most IoT payments will be highly contextual, passwords are neither the smoothest nor the most secure option. Biometrics, on the contrary, offers a foolproof way of identifying individuals.

Lastly, biometrics better support behavioral security. Paired with location-based services, biometrics can tell a lot about where the user is and what they’re doing. Payment services providers can leverage that data to create cross-platform identity checks and custom authentication levels depending on the transaction type.

For instance, voice-based or finger-based authentication can prevent your kids from ordering a bunch of candy through a smart fridge or a home voice assistant.

6. Give your wallet an attractive UX

Payments are largely invisible. But that doesn’t mean users don’t deserve an attractive mobile payment processing interface that guides them through the transaction. The biggest challenge is designing for the variety of IoT form factors we have:

- Small wearable screens

- Larger smart fridge and vending machine displays

- In-car dashboards, head units, and other types of human machine interfaces

There are also cashless QR payments, which are gradually replacing point of sale systems in the Asia-Pacific region. These will also need a separate interface within your mobile wallet app.

Ultimately, screen size and operating system will dictate most of your design choices. So study those specifications in advance and ask yourUX design team to create several wireframes for different payment flows.

Investing in exceptional UX design is a strategic move that will ensure delightful payment experiences and will keep users coming back. An exceptional UX can be achieved by avoiding complexity in interface design, navigational logic, and digital wallet database design. Your focus should be on user-centric usability principles, including responsive interfaces, intuitive navigation, and personalized experiences.

7. Implement robust security measures

Do we even have to talk about security as a top priority when building a digital wallet? You can only build trust with consumers if they are confident that their data is safeguarded from leaks and threats. We’ve already explained how tokenization is an effective tool in keeping intruders out. Now, here are eight more ways to make a digital wallet more secure:

- Multi-factor authentication (MFA) adds a protection layer to the sign-in process. MFA is a multi-step user verification method that requires more than one factor of authentication, such as a password along with a biometric identifier (like a fingerprint) or a verification code sent to a user’s device.

- End-to-end encryption (E2EE) prevents third parties from intercepting sensitive data while it travels from one device or system to another. Data is encrypted prior to sending and can only be decrypted by the intended recipient.

- Point-to-point encryption (P2PE) encrypts payment data right from the point of capture until it reaches the intended destination: a secure decryption endpoint. This safeguards against interception and ensures confidential data remains secure throughout the transaction process.

- Password protection measures such as password complexity requirements, secure storage, and password recovery techniques significantly strengthen digital wallets against unauthorized entry.

- Account freezing is used to block a wallet in case of suspicious user behavior or activity. The wallet owner can also suspend the wallet by call or message.

- A transaction ceiling can be set to prevent users from transferring too much money in a single transaction or making transactions unusually frequently.

- Security audits must be conducted systematically to pinpoint gaps and vulnerabilities so security teams can address them proactively, avert potential threats, and provide a secure payment environment to users.

- Firewalls act as a barrier between a digital wallet and a network, keeping control of incoming and outgoing traffic. A firewall adds an additional layer of protection to an app by preventing unauthorized access and blocking suspicious traffic.

Top 5 must-have features for digital wallets

You can only win customers’ love and loyalty with your eWallet if it offers delightful payment experiences that make people feel their needs are catered for and their lives are easier. Here are the most wanted eWallet features that can convince consumers to switch from traditional payment methods to a digital wallet.

Seamless registration, sign-in, and onboarding

People typically experiment with several apps before choosing the best fit. If the registration process is messy and makes the user feel stuck at the first interaction with a wallet, they will never come back. Make sure users love your wallet at first sight and will stick with it because of a warm welcome with a flawless onboarding experience.

Easy and fast payments

People want simple and instant payments with their smart devices. If this payment need is met, they will not only use your service again but will probably recommend your digital wallet to their friends.

Transaction history visibility

With detailed transaction records at hand, users can track their spending and manage their budgets much better. Especially when it comes to handling multiple cards and accounts, a well-organized transaction history is a life saver.

Multi-currency options

Grant your customers the flexibility to store their funds in various currencies on the account and let them exchange currencies within their wallets.

Gamification rewards

Customers should be rewarded for their trust in your product and loyalty to your brand, right? If a digital wallet features attractive cashback rewards and gives bonuses to users for making payments, customers will feel appreciated and entertained and will keep coming back for more fun and treats.

What will the future of IoT payments look like?

As smart payments move from the margins to the mainstream and the digital wallet market keeps forging ahead, the key question is who will own the payment experience and all the rich customer data that comes with it.

Already, we have several contenders including OEMs, FinTechs, and banks. Every party can capture significant benefits from creating a digital wallet to support both person-to-device and machine-to-machine transactions. With further advances in AI and connectivity, use cases for machine-to-machine payments will surge, creating even more exciting opportunities for payment services providers.

Connect with our team to get more insights into the Internet of Payments landscape and discuss new financial software development opportunities!