Self-service banking is changing the way customers access banking services. Instead of waiting at a branch for a bank employee to help, they can now check their balances, transfer money or apply for a loan themselves — anywhere, anytime.

This has turned banking from a time-consuming chore to a highly convenient, user-friendly experience. But that’s not all — it has also helped banks realize new levels of operational efficiency. Unsurprisingly, both banks and their customers have been quick to adopt self-service tech.

In this guide, we’ll explain everything you need to know about self-service banking and the key role it plays in digital transformation. Read on to explore:

- How to implement self-service solutions effectively

- Key technologies and future trends

- How Intellias can help you deliver digital banking services that empower customers

The benefits of self-service banking

So why is self-service banking such a game-changer? Below, we’ll look at the key advantages it brings to both customers and financial institutions.

Improved customer experience

With self-service mobile banking, customers can access their accounts, manage their money, and use personalized financial tools instantly, from the comfort of their own homes. No more waiting in line at stuffy local branches. No more being limited by rigid opening hours.

The quality of digital services is now a key differentiator for banks. Those that consistently enhance the customer experience grow 3.2 times faster than those that don’t.

Greater operational efficiency

The benefits of self-service in banking aren’t limited to customers. By enabling people to help themselves, banks have been able to cut costs and increase operational efficiency. As a result, banks are increasingly downscaling their high-street presence. In the UK, almost 1,000 bank branches closed in the last two years alone — a trend that’s being echoed worldwide.

With fewer overheads, banks can cut costs significantly. At the same time, digitizing customer interactions improves transaction accuracy and fraud detection while minimizing the need for manual intervention.

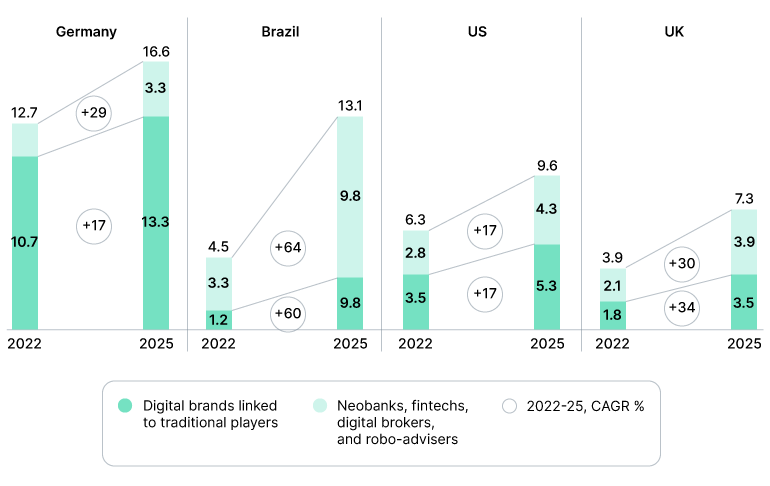

Some challenger banks have been fully digital since their launch, without a single local branch. These so-called “neobanks” are slowly claiming a larger stake of the overall revenue pool compared with their legacy counterparts, as you can see below:

Source: McKinsey

Enhanced customer engagement

Self-service banking solutions have unlocked new levels of customer engagement. Now, customers can receive tailored advice and service suggestions directly to their smartphones. They can get answers to their questions in real time with AI-powered chatbots. The result is greater convenience, control and personalization in banking.

Key components of self-service banking

Self-service banking is a combination of digital services and tools designed to help customers get what they need faster. Let’s look at different self-service banking components and how they work.

- Automated Teller Machines (ATMs). While ATMs have existed for decades, they’ve evolved over the years from simple cash dispensers to full-service portals. Customers can now make cardless withdrawals, pay bills and deposit money with ease.

- Online and mobile banking. Intuitive apps and online banking portals enable customers to open accounts, manage finances, make payments, invest money and create budgets. Biometrics and multi-factor authentication ensure robust security on the go. Chatbots provide real-time assistance and answer questions, reducing the need for call centers.

- Interactive Voice Response (IVR). Using IVR, customers can process transactions, check balances and resolve queries through automated voice systems. This enables human-like assistance without the wait, particularly during out-of-hours times.

- Self-service kiosks. Usually found within high-street branches, these are similar to ATMs but offer a broader range of services. Customers can open accounts, apply for loans, submit documents and even talk to human bank tellers via video call.

Implementing self-service features

Success with self-service banking isn’t a given. It requires careful consideration of customer needs and preferences. So what should you focus on when implementing self-service features?

First up, it’s crucial to prioritize customer-centric design. It can be tempting to design self-service banking experiences with tech-savvy young adults in mind. But your digital services need to be simple and intuitive for anyone to use — especially older customers whose high-street branch recently closed down. In practice, this means:

- Designing intuitive user interfaces

- Using simple language that everyone understands

- Reducing processes down to as few steps as possible

- Providing in-app support and clear instructions

Behind the scenes, you should focus on robust backend integration. You need your new self-service banking technology to integrate seamlessly with legacy systems, so everything runs like a dream.

But it doesn’t stop there. The tech landscape is constantly evolving, and with it, so are customer expectations. You’ll need to roll out continuous feature updates, additions and improvements to stay ahead of your competitors and retain customers. Real-time analytics and customer feedback can help you understand how different features are being used — and what areas need improving.

Technologies in self-service banking

So, what’s powering the self-service banking revolution? Several disruptive technologies are leading the way, enabling banks to provide highly secure, intuitive and personalized banking services on the go. Let’s take a look at the most important ones.

Artificial intelligence (AI)

As perhaps the most disruptive technology trend of all time, artificial intelligence is changing the way businesses and customers interact — and banking is no different. Thanks to a combination of predictive analytics and machine learning (ML), customers can enjoy personalized banking experiences, recommendations and financial advice.

ML-powered chatbots can provide 24/7 support, leveraging natural language processing (NLP) to provide human-like interactions. Customers can get answers to questions and resolve issues quickly, at any time of day.

Cloud computing

The cloud revolution has enabled banks to roll out digital services that are highly secure, scalable and cost-effective. Self-service banking apps can be deployed rapidly, with real-time updates and seamless accessibility over a range of channels. At the same time, cloud solutions make it easier for banks to integrate analytics and AI into their digital products and services.

Today, 55% of Americans and 85% of Europeans manage their accounts using mobile banking apps, most of which are hosted on major public clouds, such as Amazon Web Services (AWS), Microsoft Azure and Google Cloud.

Blockchain

While blockchain technology is yet to be widely used in banking, an increasing number of institutions are exploring how both public and private blockchains can be used to streamline and enhance banking processes.

Contrary to popular belief, blockchains increase financial transparency. The traceability and immutability of transactions make them a powerful tool in fraud prevention. For self-service customers, blockchains also have the potential to speed up identity verification, Know Your Customer (KYC) and anti-money laundering (AML) processes.

IoT integration

IoT (the Internet of Things) means that banking tools aren’t just smart — they’re able to talk to each other. This enables banks to deliver enhanced self-service processes while simultaneously improving operational efficiency.

Take smart ATMs and banking kiosks, for example. Built-in sensors can track cash levels, detect jams or flag hardware issues in real time. If an ATM is running low on paper for receipts, it’ll alert the maintenance team or branch staff. If replacement paper is also running low, it can be ordered automatically. The result is less human intervention and reduced downtime.

The Intellias method: self-service banking done right

To maximize the opportunity that self-service banking presents, it helps to work with an expert technology partner like Intellias. We build digital banking solutions that drive growth by focusing on three key areas:

- Business process optimization

- Outstanding customer experiences

- Technological innovation and software development

Whether you’re looking to build a digital bank from scratch, launch new self-service apps and services, or modernize your IT infrastructure, we can help. Our expert team brings deep industry and technical knowledge to guide you every step of the way — from ideation and planning to product delivery.

For instance, we recently helped one of the world’s leading banks build a custom banking solution for hassle-free customer onboarding. Instead of battling through an outdated, clunky process that took several days to complete, customers can now open accounts in minutes using an intuitive app. This has enabled the bank to:

- Cut new account onboarding time from 3 days to 15 minutes

- Reduce the number of application fields from 74 to 21

- Eliminate paperwork from the sign-up process

- Meet customer expectations in a highly competitive market

Read the full story here: Designing a World-Class Banking Solution for Painless Onboarding.

Emerging trends in self-service banking

So, what’s next in the world of self-service banking? In the coming years, we can expect more of the same — improved services, powered by cutting-edge tech. Here are some key trends to look out for:

- AI integration. Despite the disruption, AI is still in its infancy. In the coming years, we can expect to see AI capabilities integrated into banking apps as standard. Think personalized in-app assistants who know what you like and need.

- Biometric authentication. Biometrics are improving in-app security, enabling customers to access their accounts using fingerprints or retina scanners.

- Open banking and API ecosystems. Standardized APIs enable banking apps to pull in data from third-party services in real time. The result is broader self-service tools and a seamless, personalized experience.

- Non-fungible tokens (NFTs). NFTs might help streamline self-service banking processes by storing information on the blockchain in the form of digital tokens. Instead of sourcing paperwork to prove you own a car or a house, you’d simply link the NFT in the app.

Challenges and solutions

Implementing effective self-service banking solutions isn’t always plain sailing. To help ensure a smoother process, here are some common challenges to be aware of — and how you can overcome them.

Security risks

Self-service banking relies heavily on digital channels. This increases the risk of data breaches and fraudulent activity while creating new attack vectors for phishing attacks and other cybercrime.

Solution: Implement robust security measures, including AI-powered fraud detection, biometric authentication and end-to-end encryption. Educating customers on security best practices is also crucial.

Technological barriers

Many financial institutions continue to rely on outdated legacy systems. This makes it difficult to integrate modern self-service banking solutions.

Solution: Banks can choose to modernize their IT architecture. Alternatively, they can adopt middleware solutions that bridge the gap between legacy infrastructure and modern digital services. Partnering with a technology expert can help make digital transformation smoother.

Customer adoption

Not all customers are tech-savvy. Some may be hesitant to use self-service banking due to unfamiliarity, security concerns or a preference for more traditional banking methods.

Solution: Make your self-service banking solutions as easy to use as possible. That means great UX, clear user interfaces and in-app support. Education is also crucial to help customers understand the convenience and ease of self-service banking.

Maintenance and downtime

Self-service banking infrastructure such as ATMs and digital kiosks require regular maintenance. Unexpected downtimes can lead to frustrated customers and reduced adoption.

Solution: Banks can reduce downtime by using IoT-powered real-time monitoring and predictive maintenance to detect potential failures before they occur.

Top-performing examples of self-service banking

Self-service banking is now an expectation among customers, but some banks are better at it than others. Here are four examples of financial institutions taking a modern, innovative approach to banking that puts customers in the driving seat.

Monzo (UK)

Challenger bank Monzo has set the standard for digital, self-service banking. Founded in 2015, Monzo doesn’t have a single branch. Instead, its banking services are provided exclusively through its mobile app. It stands out from legacy banks thanks to its ultra-intuitive UX and simple yet powerful tools, including:

- Hassle-free, in-app account opening and onboarding

- Budgeting tools and money pots

- Data-driven insights into spending and saving habits

- Savings and investment accounts

Source: Monzo

DBS Bank (Singapore)

While not a newcomer like Monzo, DBS Bank has been quick to ride the technological wave. Its digital-first approach has resulted in a string of awards, including World’s Best Bank and Global Bank of the Year. Here’s what it offers:

- An award-winning mobile app

- Advanced self-service options, including video teller machines

- A digital banking portal where customers can manage accounts, pay bills, set up standing orders and apply for loans

Capital One

Capital One is a banking service provider that offers a range of self-service tools designed to empower customers, some of which are truly unique. For example, Capital One offers:

- Smart ATMs for depositing checks, making cardless withdrawals and paying bills

- Self-service kiosks where you can open accounts or apply for credit cards

- Eno, an AI-powered virtual assistant that offers service customization and real-time support

- Capital One Cafés — a welcoming space where customers can unwind, grab a coffee and do their banking

Revolut

Revolut is a FinTech pioneer that has changed the banking game since its launch in 2015. Like Monzo, it’s a digital-only bank with no physical branches. Its highly intuitive app empowers customers to help themselves, guiding them through account opening, setup and banking services. Revolut takes things beyond regular banking, however, offering features such as:

- Multi-currency accounts and in-app currency exchange

- Savings vaults, with the money held in an interest-earning account with a trustee

- Virtual, disposable in-app bank cards for secure mobile payments on the go

- Banking analytics for smart budgeting, cash flow management and spending insights

- Simple in-app investing in stocks, ETFs and cryptocurrencies