Why reach for the credit card when you can use your phone to pay for your coffee? That’s the kind of convenient, invisible payment experience we’re getting used to. But what if you could just walk into your favorite coffee shop, pick up a hot brew already waiting for you at the counter, and dash out the door? Ahem, what about paying? Well, that’s settled by a happy combination of analytics, connectivity, and payment infrastructure: the Internet of Payments.

Brainstorming a new payment service? Hop on a call with our FinTech team for a quick consultation!

What is an IoT payment?

IoT payments are machine-triggered payments based on real-time data analytics.

Imagine your connected car’s dashboard automatically suggesting you authorize a payment for fuel as you approach the pump.

In the future, IoT payments might look like a wearable healthcare device sharing your prescription and payment details with a smart pharmacy vending machine or an AgriTech system paying for water and ordering supplies when certain conditions are met.

By 2023, this new market of machine-to-machine (M2M) transactions will hit $27.62 billion according to Medici Global. While some of this revenue will come from payments currently made using other channels (e.g. credit cards being replaced by in-vehicle digital wallets), new payments will also emerge, as the examples below illustrate.

Cross-industry use cases for the Internet of Payments

Picture this: you’ve just returned from vacation. At the airport, you pick up your car and are billed automatically as you drive out of the lot and through the toll gates onto the highway.

As you head home, you receive a quick update from your smart meter, saying that your monthly electricity bill just went through. Your fridge has a quick update for you too, reminding you to reorder groceries since you’re completely out of food. You ask your voice assistant to confirm all suggested items from the list and authorize payment as you pull into a store. You quickly pop in, grab some lunch, and head back to your car. As you pass the checkout, you get billed automatically.

That’s the kind of seamless contextual payment experience custom IoT development can bring. And we’re already seeing the early onset of it across industries.

Smart cities

Cashless cities can be happier cities. Adding a sensor plus payment option to any object and connecting it to the network can eliminate a good dozen frustrating inefficiencies we deal with every day, from paying for transportation to paying taxes.

Consumers across the 100 cities [analyzed in the study] currently spend an average of 32 hours a year – nearly a full work week – on cash-related payment activities. Greater adoption of digital payments is estimated to reduce this figure to 24 hours a year, saving consumers in the 100 cities an average of over $126 million per year.

But cashless payments aren’t just a win for urban dwellers. Research by Visa indicates that eradicating cash can provide the 100 cities they studied over $470 billion in direct net benefits per year. Faster economic growth and improved wages plus productivity come as attractive side benefits.

So what type of connected payment experiences should urban planners look into to capture those figures?

- Public transportation and multi-modal journey ticketing

- Payments for government services and taxation

- Parking, traffic management, and tolls

Learn more about how new technologies are solving the pressing challenges of urban living.

Sweden is among the first countries to extend the concept of cashless from a city to a country-wide level. Two-thirds of the country’s population already use a mobile payment service launched jointly by the country’s six biggest banks along with a unified BankID for accessing financial services.

Sweden’s long-term vision is to establish a pan-Nordic real-time payment infrastructure for the 27 million residents of Sweden, Norway, Denmark, and Finland by 2021. As ambitious as it sounds, this project is on the fast track to success. Soon, Nordic citizens will be able to enjoy a seamless multi-currency payment experience. Clearly, this initiative will bring a surge in cross-border business ventures and ease the process of collaborating on new urban projects to fuel sustainable growth.

Smart houses

Our homes contain a lot of devices that can host embedded financial functionality — everything from automated utility payments to automated supply ordering. What’s more, IoT opens up a brand-new world of possibilities for pay-per-use business models and servitized offerings.

According to PwC, 52% of customers are more likely to buy a pricey smart home product in the future if it comes with a payment plan. Embedded payment functionality can automate the process of repayments.

Additionally, the general consumer sentiment is geared towards renting over ownership. Allowing customers to walk into an unattended rental location or pick-up point, grab the item they’ve pre-ordered, and have their account billed automatically during the period of use creates another avenue of growth for all sharing economy companies.

Moreover, IoT payments can boost the after-service market. We all know how frustrating it can be to get ahold of an HVAC engineer or even someone to repair a leaky dishwasher. A smart appliance can send a distress signal to the retailer/manufacturer, ask the owner to confirm an appointment, and automatically bill the owner’s account once the job is done (or credit it towards the prepaid guarantee).

Lastly, IoT payments can majorly improve the delivery of utilities in underserviced areas. For instance, in Niger, CityTaps is pioneering a smart prepaid water metering system that can increase the availability of running water in underserved areas and reduce non-revenue water losses by up to 46%. Using ultra low energy ISM band radio and GSM/GPRS, CityTaps created a two-way communication gateway between local water provider and customers. This setup also allows customers to settle their water bills via a mobile money account, which is useful since most people in Niger are underbanked.

Automotive

Gas, parking, drive-throughs — there are a lot of monetary operations happening on the commute to work. So much so that connected car payments are estimated by PYMNTS and P97 Networks to be a $230 billion opportunity.

And OEMs are already in the race, rushing to incorporate payment functionality into connected cars. GM pioneered an e-commerce marketplace in 2018 and keeps onboarding new service partners. Honda, together with Visa, delights drivers with a voice-powered infotainment system that allows users to pay for everything from gas to parking and food. Meanwhile, Amazon has been touting its Echo Auto device for customers, along with embedded voice connectivity and commerce offerings for OEMs. BMW, Lamborghini, Rivian, Fiat, and GM are among those already on board.

Retail

IoT payments can spur a brand-new subdivision of commercial activities: unattended retail. While the idea of self-service and vending machines is hardly new, the latest payment technologies can majorly overhaul the standard business models and retail setups.

Amazon’s new cashless, cashier-less stores — which allow customers to just grab items off shelves and automatically get charged upon exiting, thanks to a bevy of sensors and cameras — bring in about 50 percent more revenue on average than typical convenience stores, according to new estimates from RBC Capital Markets analysts.

If analysts’ estimates are correct, one Amazon Go store generates an estimated $1.5 million in revenue per year. That explains why the ecommerce giant plans to open an extra 3,000 Go stores by 2021.

Amazon isn’t alone in its pursuit of becoming the ultimate smart store. Several other retailers (and tech startups) are in the race:

- Kroger is working with Microsoft on a new cashier-less retail pilot.

- 7-Eleven is building cashless tech in-house and is testing a concept store in Texas.

- Caper is a startup offering AI-powered shopping carts that are being tested in two unnamed retail chains.

Some might argue that commerce will still remain a social activity, so the full automated shopping routine won’t stick in every niche. Perhaps. But by PYMNTS and USA Technologies counters that sentiment with some first-hand insights:

- 39.4% of consumers who have already shopped unattended are more likely to make purchases at automated rather than traditional stores.

- 30.9% of consumers are even ready to pay more for such an experience, as it’s “faster, means shorter lines and less talking to employees.” The latter is particularly important for 33% of respondents.

- The majority (56%) of such shoppers earn over $100,000 per year, making them a highly attractive target audience.

Retail and grocery stores, laundromats, car washes, and cars are the most frequent locations for unattended retail experiences. Partially, this is because few alternatives are available (for now).

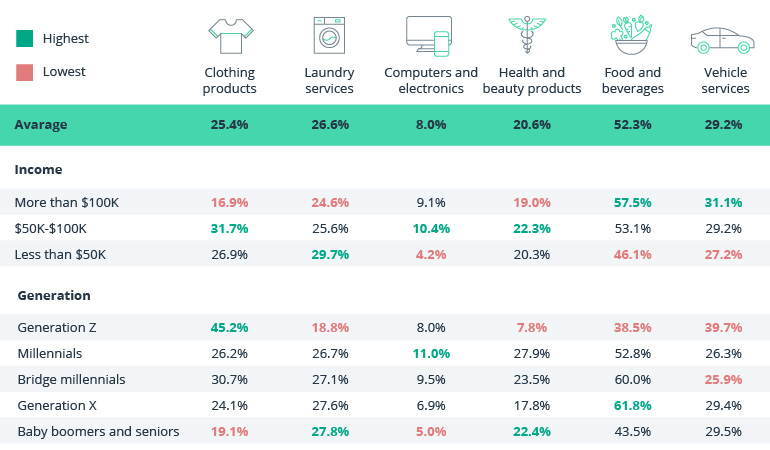

Products consumers purchase via unattended retail channels

Source: PYMNTS and USA Technologies

Here’s what this data means: trained by seamless e-commerce experiences, most consumers are getting comfortable with shopping sans assistance in real-world settings. For brands, this means the need to strengthen the omnichannel experience and focus on providing customers with all the information and assistance they need via digital means rather than in-person.

As the data shows, 38.4% of people who have already purchased via unattended channels are eager to shop for non-traditional vending products in the same way.

So what can you sell in a smart vending machine, smart device, or cashless store?

- Beauty products. L’Oréal recently unveiled Perso, a personal beauty device that uses AI and 3D printing technologies to create custom skincare and beauty formulas on the spot.

- Books and magazines. We all like to browse books without drawing the attention of a helpful assistant.

- Clothes and accessories. Uniqlo is experimenting with smart vending machines in select locations.

As consumer interest in unattended retail grows, we’re soon to see even more interesting IoT payment experiences.

How payment service providers can capture the value of IoT payments

As financial networks grow bigger and bolder, spilling over borders and spanning multiple devices, payment service providers (PSPs) need to make an important choice:

- Do it all. Deliver seamless, secure infrastructure and an integrated customer experience.

- Divide and conquer. Focus on expanding and securing the payment infrastructure and outsourcing the customer experience and other operations to partners.

In the wake of open banking, divide and conquer may be the far better choice. Here’s why: Payments is an expensive business to be in. Payment activity at an industrial scale has significant technology and regulatory hurdles.

Regulatory hurdles are well recognized by tech companies who have tried to make cautious forays into payments. Amazon, Uber, and Apple all struck partnerships with banks and payment service providers at some point.

For most players, building a payment infrastructure from scratch doesn’t make sense because:

- there are already plenty of payment services on the market

- these services are popular among customers

But when these two conditions are not met or financial institutions fail to bother much with innovations, tech companies tend to move into the payment space. This happened with so-called Chinese super apps.

Source: A.T. Kearney and Australian Payment Network, Towards an Internet of Payments — Global Platforms Redefining the Payment Landscape

To keep the upper hand in the IoT payment space (and beyond), payment service providers need to focus on making access to their infrastructure seamless, secure, and affordable.

In technical terms, this means:

- Evolving the core infrastructure to accommodate new embedded financial offerings and value propositions such as proprietary digital wallets for customers that can later be incorporated into IoT devices.

- Adopting a microservice payment platform architecture and launching new APIs to expand partnerships with other platforms.

- Improving financial data collection, governance, and analytics. For instance, data obtained from IoT devices can be further used for product development.

By taking the partnership route, PSPs can organically expand their reach across platforms while retaining the central position in customer’s lives.

Hassle-free commerce experience? Tap on IoT payments!

IoT payments can enable truly contextual commerce experiences: hassle-free, cardless, and boundless, since all things, people, services, and devices can interact with one another.

By leveraging location-based services and predictive analytics, companies can also make the payment experience highly personalized. By anticipating users’ needs, for instance, a fridge can prompt a user to reorder groceries, a fuel pump can dole out just the right type and quantity of fuel, and a wearable device can remind you to pay back that $50 for last night’s dinner with your friend.

It’s logical that payment service providers will want to remain at the heart of this budding new ecosystem of embedded finance.

Let’s build a new customer-centric payment solution for your business! Reach out to the financial software development team at Intellias for details.