The banking and telecommunications industries have always been mighty forces to be reckoned with. Addressing the essential needs for universal communications and accessible financial services, each has had a wide customer base and offered an ever-growing variety of life-improving, money-saving, and money-making products.

With time, however, it became apparent that as the demand for financial services grew, banks were not able to scale their presence accordingly. To a larger degree, the issue affected the markets of South-East Asia, Africa, and a fair number of developing countries with a large fraction of the population living in remote areas and having problems accessing traditional banking services in full.

At the same time, telecommunications companies had been expanding rapidly over the years to reach the farthest corners of the world. Having hit a certain saturation point, they faced two major issues: plummeting revenues from voice calls and a new strong competitor in the form of rapidly spawning OTT services. Telcos found themselves in a very unusual position, where over 80% of their business was suddenly selling video traffic from streaming services like Netflix and YouTube.

All of that, combined, made telecommunications companies — and banks as well — seek new, unconventional sources of revenue and business models that would let them grow and diversify their service portfolios. As surprising as it may seem, financial services and mobile payments as a telecom VAS turned out to be the potential next big thing for both.

FinTech & Telcos Partnership: Integrating Digital Payments in Telecom

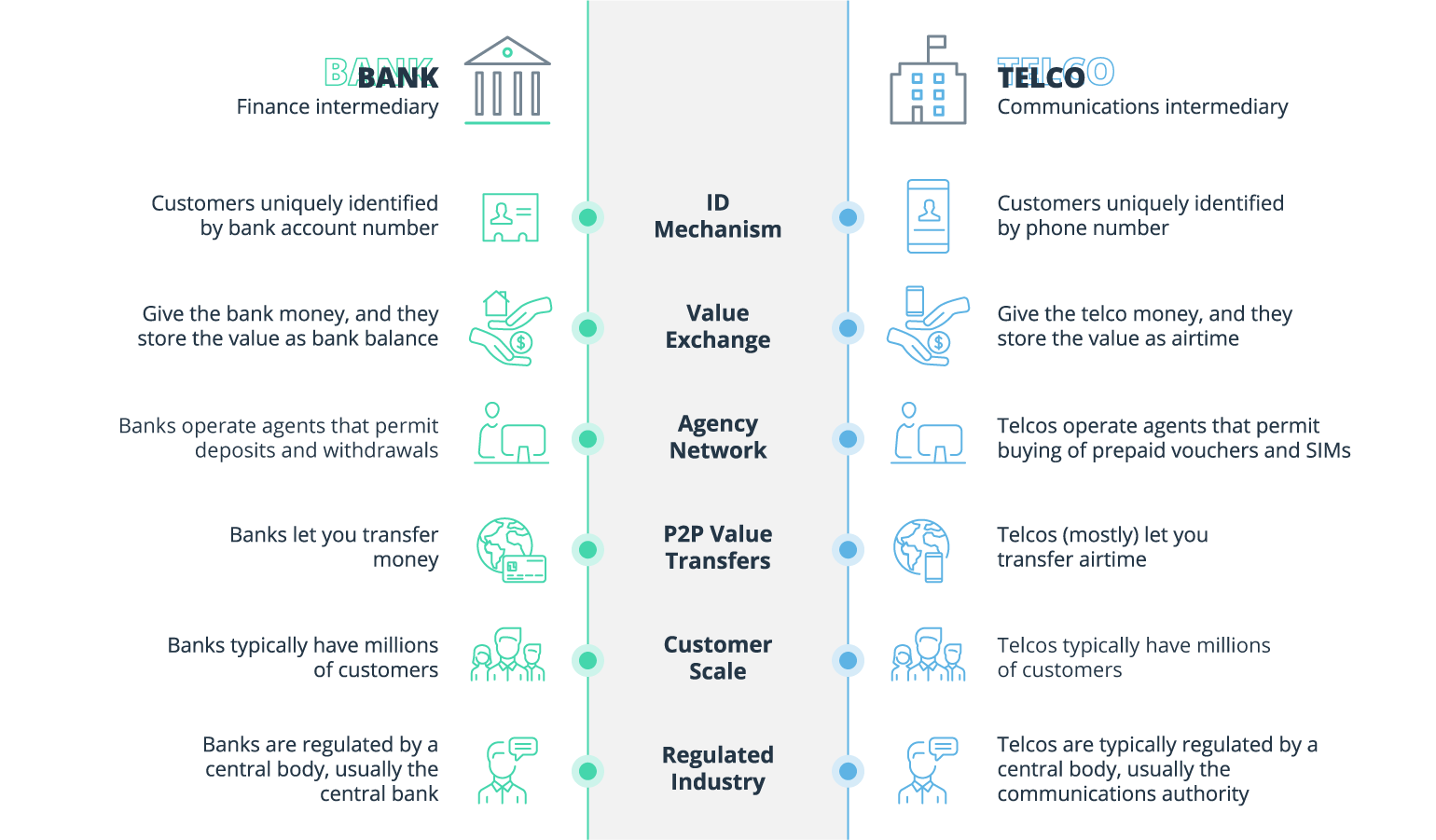

Looking at the two industries, what’s immediately noticeable is the number of similarities on the operational side:

Banks vs Telcos: comparing operational similarities between the two

Source: Medium

Telcos have one huge advantage over banks: universal accessibility, including in rural and remote areas. According to trusted sources, global GSM coverage was as high as 95% in 2020, followed by LTE with an impressive 83%. With so much potential for reaching out to everyone, it was only natural for telcos to leverage this competitive edge for purposes other than just communications.

Throwing banking and FinTech functionality on top of the vast existing telecommunications network opens a multitude of doors on both business and consumer sides. The ability to use a regular feature phone as a telecom mobile wallet for paying utility bills and rent has proven to be truly invaluable for people with limited physical access to banks and those unwilling to deal with their complex processes.

Telecommunications companies can use this model of mobile payments to make money on processing fees, currency conversion, and accurate geo-targeted ads thanks to their inherent ability to capture user location and other relevant details. In addition to digital payments for telcos, some more complex revenue-generation scenarios may involve such financial instruments as deposits of mobile money backed by real-money collaterals in a partner bank, for example.

The fusion of the two industries (or mergers or individual companies, or emergence of hybrid organizations) would bring a number of mutual advantages to the table.

Banks would enjoy:

- telcos’ digital wallet integration with their broad range of products and services

- access to a vast source of valuable big data and analytics

- potential for growing their customer base with higher retention and lower churn.

Telcos would be rewarded with:

- broader utilization of their communications networks

- access to a slew of financial tools and products from the banking industry

- extra revenue from bundled offers and promotional campaigns accessible right from the telcos’ mobile wallet apps.

Operators and banks should be expecting a lot of good things from cross-industry mergers and the transformation of their operational models, but how do consumers benefit from these commercial marriages?

Your phone is your wallet

From a user’s perspective, turning an old-fashioned flip phone into a telecommunication e-wallet for online banking, even in an area with extremely poor data transfer speeds or no data connectivity at all, is nothing short of amazing. And with modern smartphones, mobile banking becomes a breeze and a bliss.

Using a mobile device with telecom payments software offers a multitude of benefits: a user account can be set up online with a few clicks, the physical card is no longer required (or may not exist at all), the use of a multi-layer user authentication system ensures top security, payments are all accounted for and can be processed from a single digital wallet app.

In addition, a digital payment app can also offer other essential features that customers appreciate today, such as an integrated loyalty program, built-in flight and hotel booking tools, P2P transfers, and more.

Telecom mobile wallet implementations can vary significantly depending on the type of phone used and the usage context. For example, Kenya has famously adopted M-Pesa, a mobile banking system based on SMS messaging that has been a huge success in the country.

Other solutions like BibiMoney go even further and offer country-agnostic mobile banking services by means of a “SIM skin” or “thin SIM” technology. The solution provides users with an ultra-thin, film-like SIM card that is applied like a sticker to their existing SIM card, unlocking access to a variety of financial services.

In the rest of the world, mobile banking relies on high-speed data networks that enable customers to download all kinds of apps to their phones and enjoy the comfort of taking care of their finances anytime, anywhere.

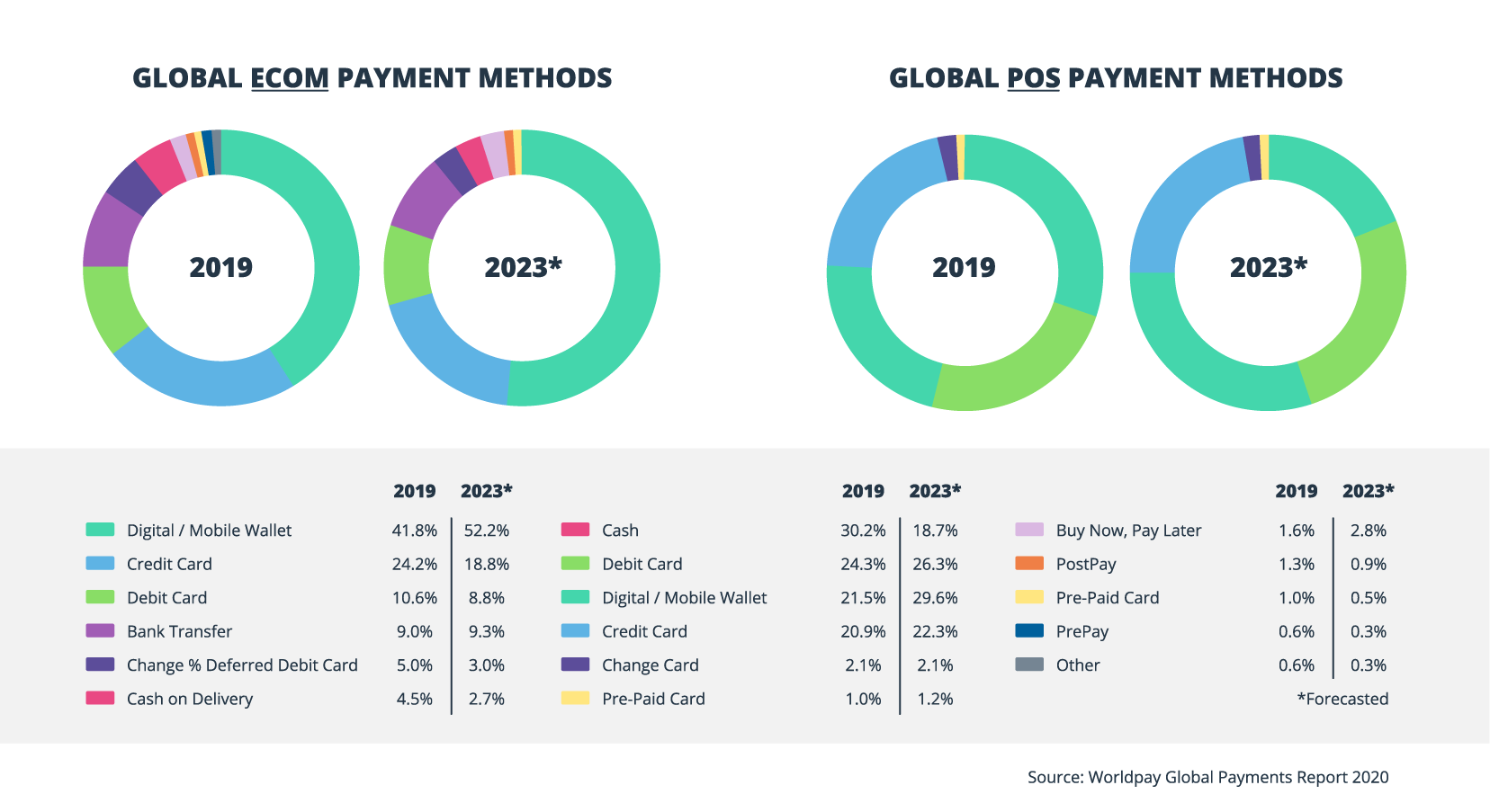

Global eCom and POS payment methods

Forming alliances

Both banks and telcos are well aware of the value of mobile payments and have been offering various solutions to customers over the years.

On the high-end side, Apple launched the Apple Card in 2019 in cooperation with Goldman Sachs and Mastercard. This card natively supports Apple Pay, offers 2% cash back (instantly redeemable) on all general purchases and 3% on Apple purchases. It also comes with fast and easy P2P money transfers and other great features.

T-Mobile responded to Apple’s strong move with T-Mobile Money, a mobile checking account service from T-Mobile and BankMobile that comes with no fees and offers an up to 4% interest rate for deposits up to $3000 made by eligible users.

In 2018, France’s telecom giant Orange launched Orange Bank, a completely new online banking platform that aims to attract at least 2 million customers and become a disruptive force on the market. It looks like they are right on track to achieving their ambitious goal, with 1 million active customers as of summer 2020.

There are numerous other similar mergers and launches around the world, with more and more traditional financial institutions giving birth to completely digital spin-offs or partnering up with leading telcos to keep up with market trends and expectations.

The majority of these new banking/telecom platforms are designed with scalability and extensibility in mind, which translates into powerful and functional APIs being offered to OTT partners and third-party developers. This, in turn, will lead to the formation of diverse software ecosystems with more payment integrations and financial tools.

Conclusions

To answer the question from the title of the article — yes, banks and telcos most definitely should join forces. In fact, they have no other options and the process is well underway. In the pandemic-ridden world, having all of the familiar financial tools at your fingertips comes in handier than ever.

In the years to come, we’ll be seeing more and more hybrid telecommunications companies offering a variety of banking services and rich ecosystems. Whether you are in Nairobi, Seattle, Sydney, Moscow or Hong Kong, there is a good chance that in 5 years’ time you will completely forget what visiting a bank felt like — and it may not be a bad thing, after all.

When it comes to building a mobile payments solution for telecom, you want to entrust the task to people who know the drill and have been there. We qualify as both. Please contact us and share your thoughts on what you need built. We’ll take care of the rest.