The business banking revolution has only just begun. For long enough, SME banking was in a pitiful state: clunky digital products, exorbitant fees, and prohibitive lending practices. For digital banks that have already developed a strong portfolio of retail products, accumulating an initial business user base was just a matter of time.

As we highlighted in Digital Business Banking Part 1, over half of SMEs around the world have business accounts with challenger banks. However, those user bases are maturing fast. The demands of SMEs now extend beyond core business banking offerings.

SMEs want more functionality from their primary business banking provider

SMEs are full speed ahead into diversification. Instead of banking with a single institution, most business owners opt to create an ecosystem of integrated financial products, consisting of offerings from challenger banks, incumbents, and non-financial services providers (to some extent).

Underpinning this trend is the fact that most SMEs cannot find one provider that offers services for all their business needs. So they take the DIY route and assemble custom portfolios of financial tools.

While 79% of SME adopters express satisfaction with the services provided by traditional banks and insurers, 57% also agree that no single financial product or service fully meets all the needs of their organization.

In this environment, digital banks have the upper hand. Here’s why:

- They already offer a superior UX and more competitive pricing than incumbent banks.

- Technologically, they’re more agile and can easily plug additional partners into their platforms — for instance, through the marketplace banking model.

- Most digital banks already have top KYC infrastructure and data to devise and deploy competitive new offerings.

All of these factors combined mean that your business banking product can occupy a central spot in the ecosystem of financial products for small businesses.

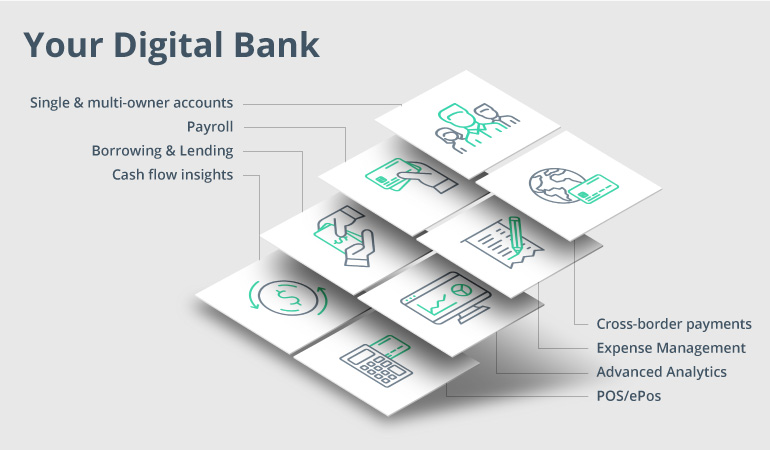

Advanced business banking account features

So what is it that business banking users want on top of existing offerings? Our team has analyzed voice of customer data from current users and identified the eight most frequently requested features.

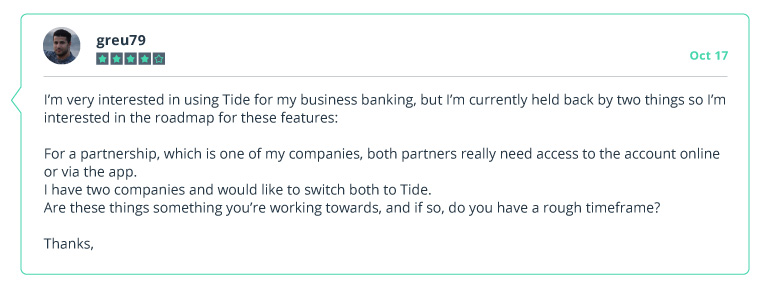

1. Multi-owner (multi-directorship) accounts

Source: Tide Community

Freelancers, sole traders, and single-director companies are not the only ones interested in a better business banking experience. Jointly owned and multi-director LLCs are also avid users of digital banking services. However, their needs have not yet been fully met.

Tide, Revolut, Monzo, and Monese business banking users frequently request multi-owner accounts. But so far, only Starling has released multi-owner business accounts, allowing multiple shareholders to jointly own and manage one account on equal grounds.

Monzo unveiled how their multi-user business accounts will look during their Future of Monzo event in November. The feature will become available to all users by the end of the year.

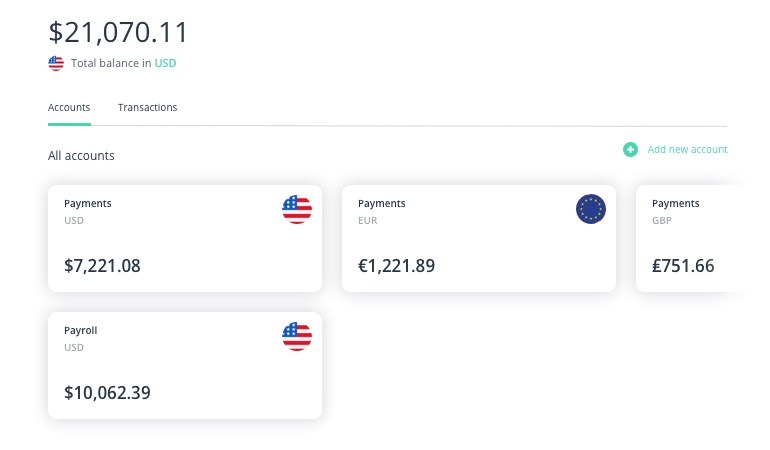

2. Multi-currency business accounts

Source: Revolut

Thanks to the internet and the rise in connectivity, anyone can do business on a global scale. However, small businesses tend to be at a disadvantage here because they often get overcharged for cross-border transfers and foreign currency payments.

A study by Capital Economics revealed that SMEs in the UK who use traditional business accounts for international payments pay an average of £755 in hidden fees per year. Collectively, this amounts to £4.1 billion in financial losses.

Apart from offering low-cost local and international transfers, you can also let companies create accounts in multiple currencies for different market operations. Revolut allows companies to open accounts in 28 currencies and have a unique IBAN for each account. Monese plans to launch a dedicated EU business account later this year.

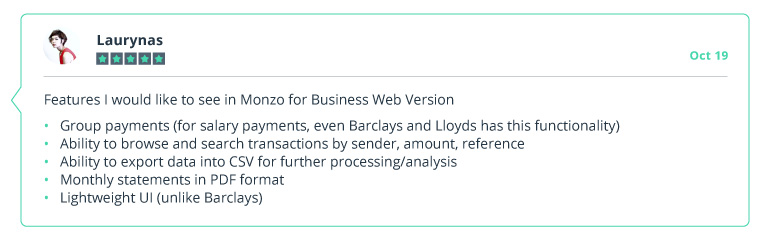

3. Companion banking web application

Source: Monzo Business Account Idea Board

Business banking often requires a bigger screen. Some mobile business banking users complain that doing accounting on a phone can be cumbersome. Others prefer working from the desktop whenever they need to manage payroll or schedule multiple payments.

While mobile banking will remain the prime channel for digital banks, offering a complimentary web application can help you attract more users.

Apart from core mobile banking app functionality, consider adding the following features to a web portal:

- Advanced spending analytics

- Downloadable monthly/yearly account statements in PDF/CSV format

- Payee and payroll management

- Access to live chat support

- Full integration with popular accounting apps such as QuickBooks and Xero

- Account control to grant read access to a third party (accountant)

4. Business-friendly transaction categorization

Expense management, accounting, and tax preparation are major pain points for SMEs. Providing business users with the ability to quickly organize all their money movements is essential to raising user experience and customer experience scores.

There are several ways to approach this design-wise:

- Introduce a set of standard transaction categories (like Revolut and Starling did), similar to those used for personal accounts.

- Allow users to add custom tags to each transaction (like N26 does) to create a personal organizational system.

- Reach out to the community and brainstorm together a new set of business-specific categories. For instance: business income, allowable business expenses (different types), tax payments, interest/loan repayments, etc.

- Consider partnering with 3rd-party services providers (accounting specialists, tax planners, etc.), so that your customers have a choice of recommendations for receiving help.

N26 recently rolled out an AI-driven spending categorization tool for both personal and business accounts. They’re among the first digital banking pioneers to venture into the personal finance management space.

5. POS terminal linked to a business account

Source: Revolut Community

Seamless connectivity with POS solutions is another frequently requested feature. Developing custom hardware, however, can be costly, so it’s worth looking into possible partnerships instead.

The following card readers and POS solutions are popular among SMEs and contractors:

- Square – offers a hardware card reader plus online payment APIs

- PayPal Here – offers three types of readers and quick integration with other PayPal products

- Clover – a modern and streamlined POS terminal offering integrations with popular online business tools

6. RPA-powered account reconciliation and expense management

Robotic process automation (RPA) facilitates the creation and execution of standard processes by automating routine tasks such as inputting, verifying, and reconciling data. Adding this technology to your business banking product will enable users to:

- Automate invoice generation and distribution

- Match and process payments after validation

- Avoid manual invoice submissions (and mistakes that come with that)

- Improve the management of transactions on balance sheets and income statements

- Spend less time on manually categorizing expenses/transactions

- Automate bill generation and reporting

7. Cash flow insights and forecasting with predictive analytics

Maintaining a healthy cash flow is the number one priority for any business. SMEs struggle with this the most, as they’re prone to late invoices and cash shortfalls due to seasonality.

Help your users get a better grip on their current rate of spending and give them a heads-up when they’re running out of funds.

Embedding predictive analytics technology will let you churn individual user data and translate it into proactive recommendations. The best part is that 89% of SMEs are willing to share more data with digital banks in exchange for better financial recommendations and offers.

A basic predictive analytics suite can help users gauge their financial standing by capturing and analyzing the following data:

- Unpaid invoices vs current account balances

- Average invoice payment times

- Tax liabilities

- Fixed expenses and due dates of recurring bills

- Available overdraft

Then it can help them translate this data into actionable insights and additional cash flow optimization tips.

You can learn more about predictive analytics solutions in banking from our white paper.

8. Overdrafts and business borrowing

Sometimes, a small business needs a little bit of help to stay afloat before new capital becomes available. Starling allows businesses to apply for an overdraft (under £10,000 on average) with a 15% effective annual rate (EAR) and no additional fees.

Tide recently rolled out a more advanced business credit scheme that will extend pre-approved credit to eligible SMEs. Tide plans to expand their credit product portfolio even further by leveraging big data analytics and integrations with lending partners.

Tide’s platform structure means we can make rich data available to partner lenders to orchestrate a smooth process for our members to access credit. This has proven to be a successful model through the Beta integration currently running with Iwoca.

Monzo has also mentioned that they plan to upgrade their loan products and are testing new credit scoring functionality.

However, the best examples of business banking borrowing hail from the East. Chinese super app Ant Financial has designed a three-minute loan application process:

- KYC data is automatically aggregated from the customer’s online profile.

- The disbursal of loan, powered by machine learning and predictive analytics, takes another second.

- Zero back-office operations happen in the background.

Alibaba-backed MYbank — another popular local FinTech player who uses a similar lending algorithm — issued over 1.19 trillion yuan in loans to businesses last year. Their non-perform loan ratio was around 1%.

Summing up

Market demand? Check. New value streams for users? Yep. Additional revenue opportunities? Plenty! Digital business banking is a ripe new niche with significant potential. Most challenger banks have already made their move and are prioritizing new features to roll out in 2020.

Yet there are still plenty of business customers left underserviced both in mature markets (UK, US, Europe, Australia) and emerging ones (Asia, South America). Will 2020 be the year you add business banking to your product roadmap?

Intellias is an end-to-end financial software partner to innovative digital banks. Get in touch with us to receive more ideas and technical insights for your next digital business banking product.