Breaking the barriers to access with technology could quadruple asset trading volumes without exposing players to extra risks.

Imagine this:

You begin your morning by checking your investment portfolio. Your stocks are doing fine (given the market conditions). But the value of your Jackson Pollock painting just went up by 20% (after a recent Sotheby’s sale). Your real estate holdings are also doing exceptionally well, as the average market prices for condos recently went up.

You decide to schedule a quick commodities order for corn (since the prices are down) and eye up purchasing a piece of land that recently went up for sale. It might be a good long-term investment, but you want to sit on the idea a bit longer.

This may sound like the typical day of an ultra-high-net-worth (UHNW) individual or an institutional investor.

But not for too long. As asset tokenization enters the mainstream, retail investors could soon be able to afford a diverse portfolio of physical and digital assets, and capital market players could be able to capture more profits.

The concept of asset tokenization

Asset tokenization is the process of creating a digital representation (token) of a physical or digital asset. For ages, we’ve been using tokens to pay for transport or play arcade games. You give your dollar and get a token of equivalent value.

The difference is that asset tokenization can now happen on a larger scale using more advanced technologies, namely the blockchain — a cryptographically protected, decentralized, immutable ledger with complete traceability.

Blockchains power cryptocurrencies — tokens that network participants receive as a reward for keeping the ledger active. These tokens aren’t pegged to a fiat currency or any specific asset class. Their value is fully demand-driven.

Blockchains also power central bank digital currencies (CBDCs) — virtual tokens issued by central banks to represent electronic money. CBDCs are pegged to a country’s fiat currency. Some 81 central banks are exploring this option, since tokenization can reduce operational costs, speed up settlements, and increase liquidity.

Lastly, blockchains can power securities trading by transforming exchanged monetary assets into fungible or non-fungible tokens, representing liquid and illiquid assets of different value. Then they can distribute these tokens, representing complete or fractional ownership, to anyone interested. The possibility of fractional ownership is what’s particularly exciting for capital markets.

Among EMEA financial institutions, between 50-75% have already assembled a digital asset/blockchain team, invested in DLT prototypes, and invested in digital asset servicing companies.

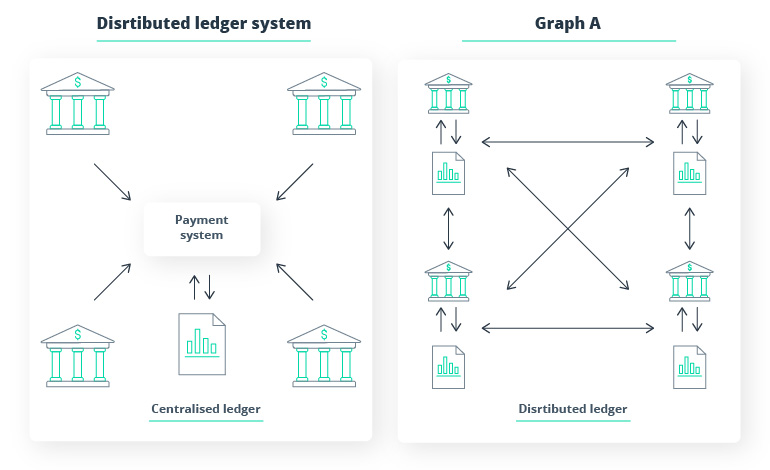

How tokenization of assets works

The idea of pooling investors’ money isn’t new. Mutual funds, exchange traded funds (ETFs), and real estate investment trusts (REITs) have been doing this for decades.

Asset tokenization uses similar mechanics. What differs is the type of shared assets and the technology for establishing asset origination, ownership stakes, trading prices, and settlement processes using distributed ledger technology (DLT).

Source: BIS

Distributed ledger technology is the parent technology of the blockchain. As the name implies, DLT is a set of protocols and supporting infrastructure for validating transactions and updating records using a decentralized computer network.

Blockchains, as a type of DLT, come with features for transaction processing such as:

- Programmable execution conditions (smart contracts)

- Cryptographic hashing for extra security

- Transaction time stamps

- Immutable and traceable ledger records

The above characteristics also enable tokenization of assets. Blockchain developers can create asset tokens (fungible, non-fungible, or security) to represent an asset class that is similar to an initial coin offering (ICO).

Each security token can include specific investor rights such as:

- Equity ownership

- Dividend conditions

- Profit share

- Voting rights

- Buyback rights

These rights are codified using a smart contract — a transactional protocol designed to self-execute under predetermined conditions.

By codifying specific investor compliance rules in blockchain code, you can set up self-enforcing and self-executing smart contracts to automate asset trading. When all contract conditions are fulfilled, security tokens are delivered to investors. Contractual terms and investor obligations are securely recorded on the blockchain and remain visible to network participants or the general public (if using a public blockchain ledger).

On the technology side, the industry has already come up with three standards for asset tokenization:

- ERC-20 standard for issuing fungible tokens (i.e. tokens with an equivalent value). For example, one ERC-20 token can equal one company share.

- ERC-1400 standard for issuing security tokens that can represent full or partial ownership of a tokenized asset. For example, one ERC-1400 token can equal a 1% stake in a real estate property.

- ERC-721 standard for issuing non-fungible tokens (NFTs) with a unique owner identifier. For example, one ERC-721 token can represent one bottle of vintage port.

These standards enable interoperability between different wallet services and asset trading platforms.

But depending on the use case, the same asset can be represented with different token models. For example, you can choose to sell one painting as an NFT token worth $1,000. Or you can offer fractional ownership via security tokens: for example, sell a 5% stake for one token worth $50.

Since security tokens act more like traditional securities, they are better regulated (unlike NFTs). Germany, Singapore, Switzerland, and the United States, among others, already have relevant regulations in place.

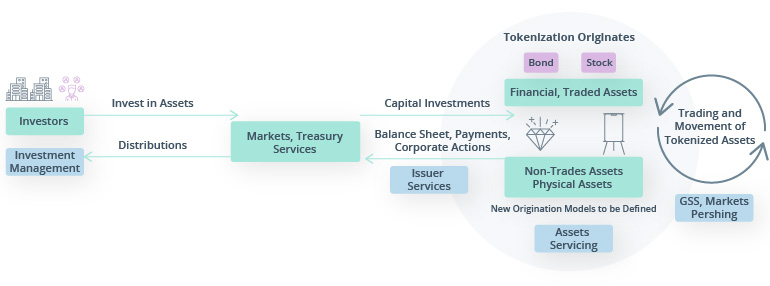

From the operational perspective, asset tokenization is the easy part. The more complex element is designing new infrastructure for the entire securities trading value chain. Traditional institutions usually have a monolithic platform of established processes for securities origination, distribution, trading, clearing, settlement, and safekeeping.

Tokenized assets force incumbents (and their tech competitors) to re-imagine the process of servicing and exchanging assets.

Source: BNY Mellon — Tokenization: Opening Illiquid Assets to Investors

But those who are quick to reconcile their processes with asset tokenization technology capabilities will be the first to profit from the emerging revenue pools.

Benefits of asset tokenization

Like it or not, tokenized assets are going mainstream.

On the retail investor side, security token trading volumes were $4.1 trillion in 2021 and are projected to reach $162.7 trillion by 2030. In Europe, the security token market may reach €918 billion by 2026 as retail investors move into this niche.

The global NFT market currently stands at $11.26 billion, though its value may swell to $231 billion by 2030 in response to token proliferation across other industries — music, fashion, retail, sports, film, etc.

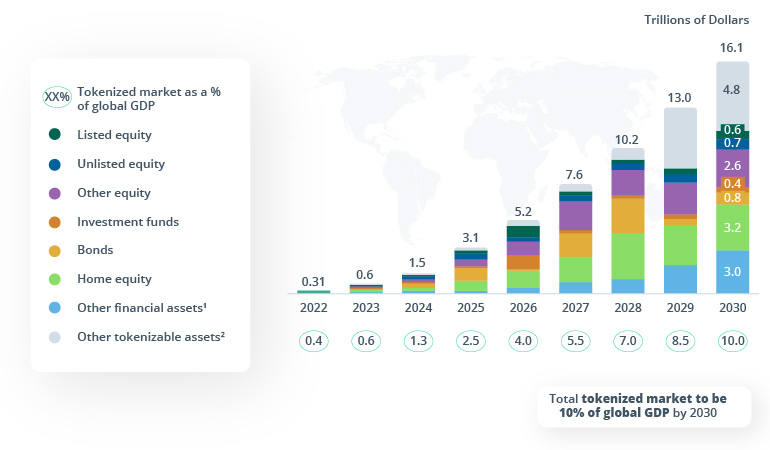

As for the traditional securities market, BCG estimates that tokenized security assets can account for 10% of global GDP by 2030.

Source: BCG — Relevance of on-chain asset tokenization in ‘crypto winter’

Given consumer sentiment and the improving regulatory stance, institutional investors are jumping on the digital asset bandwagon too. A Deloitte survey says that 76% of leading financial institutions already view tokenization of financial instruments as a major growth opportunity for their company.

The above sentiment makes sense when you consider the benefits generated by asset tokenization.

Activation of new customer segments

With crippling inflation and ongoing market calamities, retail investors are looking into alternative investments — and art, antiques, commodities, private equity, and real estate are strong contenders.

Yet only a fraction of retail investors can afford to purchase alternative investments.

35% of 25-to-44-year-old US investors indicate an increased demand for alternatives. However, an average affluent or high-net-worth (HNW) investor holds only 2% in alternatives.

Asset tokenization can change the above dynamics. NFTs can open access to new digital asset classes. Security tokens, in turn, can enable regular and affluent retail investors alike to purchase stakes in more expensive physical assets, increasing trading volumes (and profits).

At the same time, different financial industry players get to benefit from the new consumer segments:

- Wealth management firms can attract more clients with diverse classes of assets and capitalize on higher portfolio management and safekeeping fees.

- Investment banks can facilitate security or NFT token generation in a compliant manner. Additionally, they can issue stablecoins (digital currencies) to ensure higher liquidity for their trading partners.

- Trading platforms and stock exchanges can capitalize on booming demands for alternative investments, NFTs, and crypto assets by engaging more investors.

- Treasury services can profit from custodian fees for keeping physical versions of tokenized assets and record-keeping for on-chain assets.

- Digital banks can collect extra transactional fees by supplying users with easy access to fractionalized assets and preventing revenue erosion with trading platforms.

There’s plenty of room in the future $16 trillion tokenized asset market.

Effective expansion to new markets

(Robo) investing apps have already commoditized access to stocks and bonds.

However, many platforms struggle to grow from there, as they are catering to a limited population of the top 5% (sometimes the top 15%) of investors, primarily in Western markets. The competition gets quite heated, as digital and incumbent companies encroach on each other’s turf.

Big Techs are moving from “disruptor” to “mature competitor” in financial services, and have been taking initial steps in wealth management too. Many of these players broke into the market with a single offering (often payments) and then ventured into lending, savings, wealth management, and beyond. Tech giants are now aggressively growing their presence through investment in FinTechs globally.

Since many WealthTech players have created a digital onboarding system, they are now better positioned to attract clients in different markets. Blockchain technology can further remove common onboarding hurdles such as KYC verifications or payment setup/processing across multiple currencies. Then it can provide investors with access to local and foreign tokenized asset types without additional verifications or payment complexities.

Tokenization can provide industry players with hotkey access to the booming wealth management markets of the Asia-Pacific region. Wealth held by Asian investors already stands at $52.3 trillion (or approximately 20% of global wealth).

By 2026, Asia can outpace Europe and become the second-largest hub of wealth globally, with the highest growth in the HNWI customer population.

At the same time, the number of retail investors with more modest capital is also growing fast. The number of stock market investors in Indonesia has increased by 66% in two years from 2019. In India, the number of new electronic trading accounts opened each month has increased sixfold between 2019 and 2022.

However, a lot of trading in Southeast Asia still happens in penny stocks (which aren’t always the best investment instrument). Tokenized assets can be presented as a longer-term, safer, and more valuable alternative to such clients — and a solid investment diversification opportunity for HNWIs.

Faster trade settlement times

Much of the stock industry still operates by the T+2 (trade date plus two days) stock settlement rule. But this rule creates unnecessary risks, especially when markets are volatile.

Investors (especially retail investors) can fail to pay for their trades within this timeframe. Because of this, brokers must post their own capital to support customer trades for three days at any given time to ensure compliant trade settlement.

In the US, that translates to some $45 billion being settled each day by the National Securities Clearing Corporation (NSCC). If brokers fail to post the required capital, they go bankrupt during the two-day trade settlement window — a factor which can affect other market participants.

In times of market stress—say, a run on meme stocks—problems expand rapidly and can create a much broader market crisis based on instability, absence of investor confidence, or a liquidity crunch.

This puts extreme regulatory pressure on digital-first players with relatively low capitalization but a growing base of retail investors.

Since asset tokenization is powered by smart contracts with predefined conditions, settlement times for different asset classes (not just stocks) can be virtually wiped out. The trading industry can finally enter the age of real-time transaction processing, which, in turn, can translate to bigger daily trading volumes at lower operational costs. Global trade processing costs could be reduced by $17 billion to $24 billion by moving securities to the blockchain.

Multi-directional growth

The majority specialize in primary and secondary markets:

- Primary market companies mostly provide technical infrastructure for DLT/blockchain-based asset tokenization.

- Secondary market companies work on blockchain-based securities exchanges that allow investors to trade tokenized assets.

Corporate players, in particular, are interested in entering the primary market, as doing so would allow them to stand at the vanguard of new tokenized asset issuing. By capturing this niche, financial institutions could then generate two types of revenue:

- B2C revenue by offering a variety of tokenized assets to their customer base

- B2B revenue by collecting fees for asset tokenization from B2B partners and offering held assets to other financial institutions

In other words, fast-moving players can grow vertically and horizontally as digital platforms — and benefit from lower costs for product distribution, customer acquisition, and market expansion.

Meanwhile, there’s still room to create a multitude of new tokenized asset classes such as:

- Real estate

- Commodities

- Pre-IPO stocks

- Public infrastructure projects

- Physical art

- Private debt

- Antiquities

- Tokenized futures contracts

- Wholesale bonds

- Private debt

…Or any other type of illiquid asset the global markets fancy trading.

Time to tokenize

Day by day, asset tokenization is seeing greater support from consumers, legislators, and technical infrastructure suppliers.

New market entrants and corporate offerings already have à la carte options for technology partnerships to start building out a new value ecosystem for on-chain securities trading.

The ball is in your court. Use your advantage thanks to substantial institutional knowledge of financial markets and an existing customer base to deploy a pilot project. Then scale it with the help of industry partners and technology advisors familiar with blockchain technologies.

Intellias provides technology consulting and engineering services to global financial market leaders. Contact us to strategize the future of asset tokenization together.