Payment fraud is a shared locus of pressure for payment processors, merchants, and us, the regular online shoppers. Can we eradicate payment fraud? Unlikely. Can we learn how to cope with it more effectively? Absolutely.

In fact, better payment fraud detection should be a top priority for FIs. Increased volume of digital sales is ‘new normal’ for most retailers. But that’s awesome news, right?

Sure thing, but…the card not present (CNP) fraud is on the rise, too.

By 2023, retailers will lose $130+ billion in revenue on fraudulent card-not-present transactions if they fail to keep up with digital fraud prevention measures.

Ok, so should I tighten my online payment security measures, is this what you are implying?

Not so fast. Running a suboptimal fraud detection engine — one that has an offensively high rate of false positives — can cause more damage to your company than payment fraud.

Why false positives are a jinx for the financial industry

A standard rules-based security engine installed by an online retailer can decline up to 30% of non-fraudulent orders.

After being declined, 42% of customers will abandon their cart. What’s more, 4 out of 10 shoppers will go on and place an order with another company, rather give another go to the security-tight merchant.

And here’s the biggest kicker:

19% and 32% of shoppers in the $800,000-$999,999 and $1 million-plus income brackets, respectively, moved on to competing companies when their payment is declined

Yikes, that’s a target audience few retailers would want to lose! And even if you are not catering to the uber-rich of this world, those false declines can be cutting a major drain in your revenues. Accenture reports that annual global e-commerce fraud losses range from $25 to $40 billion.

Banks shouldn’t get all cozy either. IBM reports that as much as 90% of notifications about potential suspicious activities do not result in the filling of a suspicious transaction report. In other words, your systems can detect all-things-that-seem-to-be-fraud, but they are not configured to investigate whether the event was actual fraud or not, resulting in a high rate of false positives in banking.

Wait, but we already modernized some of our legacies back-office operations, including fraud monitoring systems. Where’s the problem?

Despite recent advancements and investments in new technology, 51% of banks still reported a high rate of false-positives, resulting from their technology solutions, decreasing efficiencies in fraud detection.

Basic financial security mechanisms such as two-factor authentication, network analysis, and even behavioral biometrics are good measures for card not present fraud prevention. But they do not help you tackle emerging fraud proactively.

Also, ineffective management of incoming fraud information and lack of clear data governance can make even state-of-the-art fraud detection mechanisms inefficient. So where’s the solution then? As the post title implies, it’s machine learning and AI that can make a major difference.

Accuracy detection: Using machine learning to reduce false positives in AML screening

Traditional automated fraud detection systems can get overwhelmed pretty fast.

That’s because most were never meant to cope with the large volume of incoming data from multiple sources in the first place. Next, the data itself can be hosted in a siloed, fragmented, and incomplete manner across different locations, making it harder to investigate and monitor. Lastly, such detection systems rely on outdated rules and thresholds that hardly align with the current payment

landscape — omnichannel commerce, mobile payments, contactless payments, and soon, IoT payments.

Machine learning (ML) relies on algorithms that can learn from an array of available data and create more accurate classifications of fraudulent and genuine payments. What’s more, ML-powered systems can progressively learn over time without being reprogrammed.

These qualities make ML a strong contender for augmenting the fraud investigation process and providing your analysts with the latest insights. Even better, you can set the entire process of reviewing, classifying, and flagging transactions on an intelligent auto-pilot, rather than rely on blanket rules, built upon the same logic for everybody.

The value of real AI tech is that every single person is different. This allows FIs to know how you spend and your behavior — what is personalized and specific to you? That way, they can protect you well — and also serve you well with the kinds of products you want to see.

Picture this: you and your spouse have a joint bank account. As in all happy families, one is a spender, and another one is a saver. You decide to exchange your cards for a week to see what happens.

When the spender goes on their regular shopping spree with a ‘savers’ card, a rules-based fraud detection system will likely mark this as an anomaly and decline some big-item in-store transactions. At the same time, the ‘saver’ prefers shopping online since the discounts and cashback are better. This is an untypical behavior (as per the rules-based system), so their online transactions may get falsely declined too.

In both cases, the result is the same — a trusted FI got the customer in a frustrating position. Since they have plenty of other cards and payment methods available, they’ll likely reach out for an alternative option the next time around.

56% of cardholders decrease online shopping, reduce payment card usage, and close payment card accounts after facing a fraudulent event.

And as we said before — superb customer experience is key to winning and retaining financial customers. Losing loyal customers to false declines is painful to say the least.

Now, unlike traditional fraud detection systems, machine learning algorithms can create rules, rather than follow them. ML solutions can capture and analyze 100+ specific features, unique to an individual transaction. For example, transaction time, location and type; amounts spent with certain vendors, a percentage of online vs offline sales, and so on.

As a result, the algorithm creates an evolving ‘normcore’ profile for every cardholder and triggers alerts only if the spending behavior deviates from the set standards.

But can machine learning fraud detection solutions really deliver more accurate results?

You bet! Here’s proof:

Danske Bank used to have a fraud detection system based on hand-crafted rules. At times, their rate of false positives reached 99.5% transactions, skyrocketing investigation costs, and underlying customer experience. After adopting machine learning for fraud detection, the bank:

- Managed to reduce false positive rate by 50%

- Increased fraud detection rates by 60%.

As a next step, they are currently exploring deep learning models to further improve accuracy.

Intellias also helped one of our clients — a payment services provider for the iGaming industry — incorporate a monitoring application to accept, decline, and investigate incoming transactions, based on real-time intelligence. Get the gist from the complete case study!

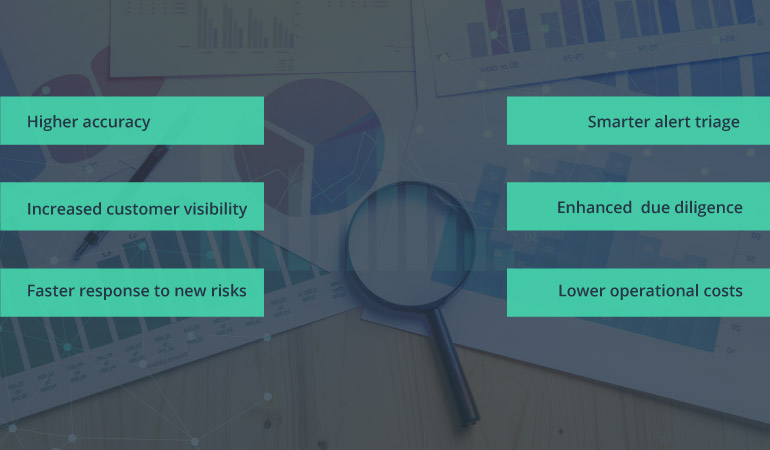

Key advantages of using machine learning for fraud detection

- Higher accuracy and lower level of false declines due to dynamic and personalized rule creation for each customer.

- Increased customer visibility that helps understand their main behaviors and create custom risk scores.

- Swifter response to new risks and the ability to identify and respond to previously unseen fraud types.

- Smarter alert triage that reduces noise and directs your investigation teams towards the most pressing issues.

- Enhanced and faster due diligence for all payments traveling through your network.

- Lower operational costs that result from better triage, improved monitoring, and reduced load on investigation teams.

What type of data do you need to for AML false positive reduction?

Cross-channel customer data is key to improving your fraud analytics and detection systems. Also, by aggregating data from across the portfolio of cardholders and connecting it to the analytics, can help you effectively connect the entire payment ecosystem, rather than individual payment channels or customer segments.

On any given day your bank may flag 10 same-looking transactions of just under $10,000. Among them, just one would be fraudulent. How do you identify which is it?

You seek additional context from the data stashed in your systems such as:

- General customer data collected as part of the KYC process. Additionally, you should take into account customer account age, existing economic relationships with other account holders (family) and businesses (employer), plus direct debit frequency.

- Transactional data — all the regular insights of volumes, frequency, transaction types (CNP, ACH, direct debit, etc), plus data on location.

- Non-transactional customer activities that may denote suspicious activities, when coupled with other factors. For example, an updated email or password, coupled with higher than usual spending can be a sign account takeover.

- Location data also acts as a proxy for possible account fraud. Big-sum cash withdrawals from multiple locations should make some bells right at your end.

- Overall behavioral data will allow you to benchmark how one cardholder compares to lookalike prospects in their segment and more effectively detect deviations in their behavior when compared to information provided during KYC.

- Social and mobile data — both provide extra context about the customer’s usual activities and monetary exchanges with people they know.

How to reduce false positives in machine learning

By supplying your machine learning algorithms for fraud detection with all of that data types, you can create an array of high-performing analytical models for preventing more false-positive declines and detecting more elaborate AML behaviors. Here are a couple of examples of how to reduce false positives in AML from the world-famous banking and consulting organizations.

QuantumBlack, leveraged machine learning to analyze over 10,000 suspected criminal account network and over 18 billion of transactions across multiple banks to create a custom scoring model for “money mule accounts” — account networks created to launder funds, by quickly moving small sums through multiple accounts to obscure the source of funds and complicate tracing. Their algorithm identified 15,000 mule accounts across multiple banks.

As part of upgrading their fraud detection system, a top 20 US bank also incorporated ML for enhanced due diligence (EDD) process. The solution developed together with IBM, automatically started the data collection process after receiving an alert, aggregating data from structured and unstructured sources. Next, it ranked all the data based on its relevance and source, plus performed sentiment analysis of the content to better understand the entity under review. Afterward, the system presented all the findings to the analyst for final review and rulings. As a result, the bank conducted 60% faster reviews and minimized the needed rework by 50%.

So not only can ML help you minimize false positives, but also improve your KYC and compliance processes.

Final tip: You need a strong data governance process to reduce false positives in AML transaction monitoring

Collecting customer and transaction data ≠ being able to use it.

Most banks have (inconsistent) data stashed in multiple places, leading to bloated alerts review times, lack of up-to-date customer visibility and extremely high costs to perform security screenings across large customer bases.

Slapping machine learning atop of that spaghetti setup won’t do you any good. The first key step to adopting any advanced analytics solutions is building a strong base, or more accurately, — a data lake for aggregating, storing, and later operationalizing all your data. Then work towards establishing a unified data collection and management process. And only afterward, look proactively into ML adoption!

Let’s secure your bank together! Contact Intellias team to learn more about intelligent solutions for predicting and preventing fraud without undermining customer experience!